Archive for 2013

-

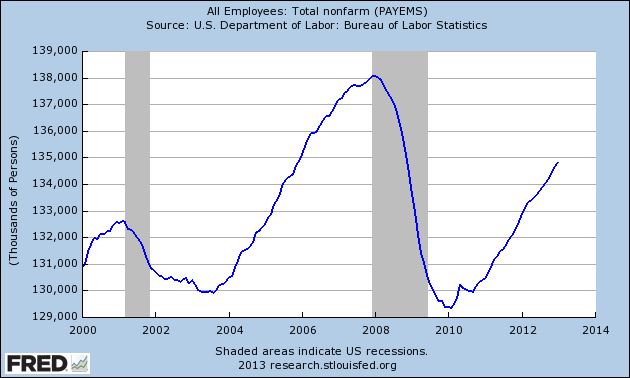

January NFP = +157,000; 7.9% Unemployment

Eddy Elfenbein, February 1st, 2013 at 9:23 amThe big jobs report this morning showed that the U.S. economy created 157,000 jobs last month and the unemployment rate ticked up to 7.9%. Both November and December’s jobs gains were revised higher.

The Labor Department today also issued its annual benchmark update, which aligned employment data spanning from April 2011 to March 2012 with corporate tax records. The revision showed payrolls grew by an additional 424,000 workers, on an unadjusted basis, in that period.

The economy has recovered 5.51 million of the 8.74 million jobs that were lost as a result of the last recession.

Additionally, the Labor Department incorporated new Census Bureau population estimates into the household survey it uses to calculate the jobless rate. The adjustment boosted the estimated size of the labor force by 136,000. It also updated how it adjusts payroll figures for seasonal swings, affecting data back to January 2008.

Private payrolls, which don’t include jobs at government agencies, rose 166,000 in January following a revised jump of 202,000 the previous month. Economists forecast they would grow 168,000 for a second month.

-

CWS Market Review – February 1, 2013

Eddy Elfenbein, February 1st, 2013 at 7:20 am“There are two times in a man’s life when he shouldn’t speculate:

when he can afford to and when he can’t.” – Mark TwainRemember the panic about the Fiscal Cliff? And the Debt Ceiling? And the Sequester? And about a dozen other things the financial media told us—insisted—that we simply had to worry about?

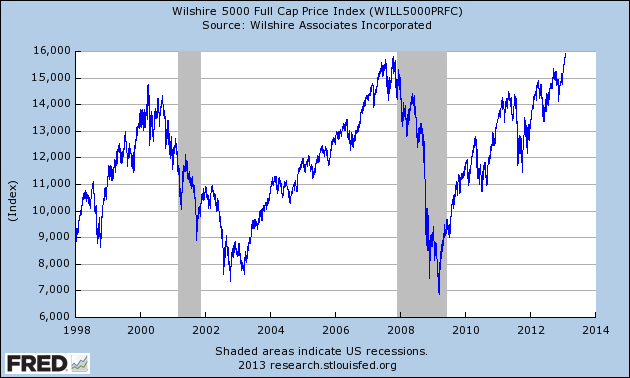

Well, here we are a few weeks later. The Dow Jones Industrial Average just closed out its best January in 19 years. The Wilshire 5000, the broadest measure of the U.S. stock market, is just below its all-time high.

Fortunately, we stuck by our strategy and ignored the noise-making scaremongers on TV. What’s perhaps more impressive is how low the market’s volatility has been. Consider this: On Wednesday, the S&P 500 had a rather minor loss of just 0.39%, and that was its worst loss of the year! Between January 9th and January 25th, the S&P 500 rallied 12 times in 13 sessions, and the only downer was a miniscule 0.09% drop.

But I have to be frank. The rally is beginning to look a little tired. For example, the S&P 500 tried to break 1,510 a few times this week and wasn’t able to bust through. That’s not a good sign. I think it’s very possible the bears may take back control of Wall Street in February. Nothing too serious, mind you, but just enough to scare the bulls away.

This was a mixed week for our Buy List stocks. The earnings reports were quite good, but some of our stocks, like Ford Motor ($F) and Harris ($HRS), didn’t respond well. That’s frustrating, but as you know, we’re in this game for the long haul.

We also had a negative GDP report for Q4, and that spooked a lot of folks. As odd as it may sound, the negative report really wasn’t that bad. When you look past the plunging military spending, the economy is better than it looks, and we’re poised for decent growth in 2013. The other big news this past week was the Fed meeting. We learned that Bernanke & Co. are firmly committed to keeping the money spigots going for a while longer. Some folks misread the December minutes, believing that the Fed was going to pull back soon. Sorry, not a chance.

Now let’s take a look at some of our recent Buy List earnings reports.

Ford Is a Buy up to $15 per Share

In last week’s CWS Market Review, I told you to expect a big earnings beat from Ford Motor ($F). Technically, I was correct. The company earned 31 cents per share, which was 24% higher than the 25 cents per share that Wall Street was expecting.

Despite the earnings beat, Ford warned that its losses in Europe this year would be worse than it had anticipated. Traders overreacted (of course, or they wouldn’t be traders) and brought the stock back below $13 per share. Let me be clear that Ford’s business is doing very well, especially in North America. Their pre-tax earnings in North America soared 110% from Q4 of 2011.

The New York Times described Q4 as a “microcosm of Ford’s recent overall performance.” In other words, strong America, weak Europe. But Ford’s strength in North America didn’t come about quickly. It was part of a painful restructuring process that’s only now paying dividends (literally, as Ford doubled its payout three weeks ago). Ford is employing that same turnaround strategy in Europe today, and the good news is that they’re far ahead of General Motors.

Don’t worry about the pullback in Ford. If you don’t already own it, the stock is a very good deal, especially if you can get it below $13. Thanks to the higher dividend, Ford currently yields 3.1%. I rate Ford a solid buy up to $15 per share.

Lower Guidance from Moog and Harris

On Tuesday, Harris ($HRS), the communications equipment company, reported earnings of $1.25 per share for the December quarter, which is the company’s fiscal Q2. This was five cents ahead of Wall Street’s consensus. Quarterly revenue dropped from $1.31 billion to $1.29 billion.

While Harris’s results were good, the news that has me concerned is that the company lowered its full-year guidance. I find that I often tell investors not to worry about this, or don’t worry about that. But lower guidance is indeed something to worry about. (By the way, I’m very glad we ditched JoS. A Bank from this year’s Buy List. The stock got pounded for a 15% loss on Monday after it gave an ugly earnings warning.)

Previously, Harris saw full-year earnings ranging between $5.10 and $5.30 per share. The company lowered that range by 10 cents per share at both ends. Harris now sees earnings ranging between $5.00 and $5.20 per share. So really, the guidance isn’t that much lower. We have to put this in context of a stock that closed the day on Thursday at $46.20, which is about nine times earnings.

Harris now sees 2013 revenue dropping by 2% to 4%. The previous range was flat to negative 2%. The company blamed the lower guidance on “slower government spending resulting from growing budget uncertainty.” It’s still early in the year, so I’m not giving up on Harris, but I want to see some improvement later this year. Harris remains a good buy up to $53.

Moog ($MOG-A) also joined the lower-guidance club, and like Harris, the news is disappointing but hardly dire. Last Friday, Moog lowered its full-year guidance from a range of $3.50 to $3.70 per share to $3.50 to $3.60 per share.

John Scannell, Moog’s CEO, noted that the company is off to a slow start this year, “The weakness in the major economies around the world is affecting our industrial business. On the other hand, the aircraft market is strong. We have moderated our forecast for the year slightly, but we are still projecting growth in both sales and earnings in 2013, despite the headwinds in our industrial markets.” Interestingly, Scannell’s comment reflects the same news about lower defense spending that we saw in the GDP report.

Moog’s quarterly revenues were up 3% to $621 million. Net earnings dropped 6% to $34 million. On a per-share basis, Moog made 75 cents last quarter. Since no one follows them, I can’t say if that beat or missed expectations. The stock still looks good for the long-term. Moog is a good buy up to $46 per share.

Profit Machine at Nicholas Financial Continues to Hum

On Wednesday, Nicholas Financial ($NICK), our favorite used-car loan company, reported quarterly earnings of 37 cents per share. But the results were distorted by taxes on their ginormous dividend late last year. Not including that, Nicholas earned 43.6 cents per share. Frankly, that’s a bit lower than I was expecting (around 45 cents per share), but not by much. I’m not a fan of NICK’s escalating operating costs, and I hope that doesn’t become a problem.

Our larger thesis for NICK still holds: that the company can rather easily churn out 45 cents per share every quarter. As long as rates are low and the economy is improving, NICK will do well. The math is pretty straightforward. Any company that’s pulling in, say, $1.80 per share per year should be going for at least $15, and possibly closer to $17. I think investors see NICK as a shaky subprime play. It’s not. In fact, NICK has gotten more conservative over the past few years. Like Ford, NICK pulled back below $13. Again, don’t be alarmed. NICK is a solid buy up to $15.

One more late earnings report. After the close on Thursday, CR Bard ($BCR), the medical technology firm, reported earnings of $1.70 per share, which beat consensus by three cents per share. Bard made $6.57 per share for all of 2012, which is up from $6.40 per share in 2011. I like that kind of growth. The downside is that Bard warned that 2013 will be rough, but they see extra-strong growth coming in 2014 and beyond. For now, I’m lowering my Buy Price on Bard to $102.

More Buy List Earnings Next Week

We’re now heading into the back end of earnings season, and the results have been good so far. The latest numbers show that of 237 companies in the S&P 500 that have reported, 74% have beaten earnings expectations, and 66% have beaten sales expectations.

Next week, we have four more Buy List earnings reports due: AFLAC ($AFL), Cognizant Technology Solutions ($CTSH), Fiserv ($FISV) and WEX Inc. ($WXS). I’m curious to hear what AFLAC has to say. Three months ago, they told us that Q4 earnings will range between $1.46 and $1.51 per share. That means full-year 2012 earnings between $6.58 and $6.63 per share. The problem is that AFLAC’s bottom line has probably been squeezed by the low yen. The question how is, how much? AFLAC has said to expect 2013 earnings to rise by 4% to 7%, but that’s on a currency-neutral basis. I like AFL up to $57.

Cognizant publicly said they expect earnings of 91 cents per share, and their forecast is usually very close. For this year, I think they can make $4 per share. I’m looking to see what kind of guidance they provide for 2013. CTSH remains a good buy up to $83.

Two weeks ago, Fiserv guided lower for Q4 but higher for all of 2013. I think this stock has some room to run. Fiserv is a good buy up to $88. Before I go, I wanted to highlight Microsoft ($MSFT). The shares are an especially good buy if you can get them below $28.

That’s all for now. Stay tuned for more earnings reports next week. We’ll also get important reports on factory orders and productivity. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. Our old friend Russell Wasendorf, Sr. was just sentenced to 50 years in prison for massive fraud. Here’s our post from this summer on ol’ Russ, and tips for how you can spot financial fraud.

-

Morning News: February 1, 2013

Eddy Elfenbein, February 1st, 2013 at 6:55 amU.K. Manufacturing Grows in Sign of Industry Stabilization

EU Regulators Want to Examine Dutch SNS Reaal Rescue

China Approves HSBC Sale Of Remaining $7.5 Billion Ping An Stake

Consumer Spending in U.S. Rose in December as Incomes Surged

Doubt Is Cast on Firms Hired to Help Banks

Justice Department sues to block Anheuser-Busch InBev merger with Grupo Modelo

Deutsche Bank Avoiding Capital Increase as Jain Sees Pain

Sharp Shares Rise After Report of Operating Profit

Zoetis Prices $2.2 Billion IPO Above Expectations

Newell Rubbermaid Goes After $127 Billion Health Market

Mattel Misses Analysts’ Estimates For Holiday Quarter

Ex-Peregrine Chief Sentenced to 50 Years in Prison

Wal-Mart’s Union Complaint Shelved by U.S. Labor Board

Jeff Carter: Tax Code Carve Out-Free Money For Smart Investors

Cullen Roche: Fear & Greed Index Showing Signs of Extreme Greed

Be sure to follow me on Twitter.

-

Reprise: Tips on Spotting Financial Fraud

Eddy Elfenbein, January 31st, 2013 at 4:57 pmHere’s an update to a post from last summer. Our old friend Russell Wasendof, Sr. was sentenced today to 50 years in prison for massive fraud. The following is our original post from August 17th:

For those of you who never got around to taking ancient Greek in college, the word of the day is hubris.

Webster’s dictionary, 8th ed.: “Excessive pride or self-confidence, often entailing a loss of contact with reality and an overestimation of one’s own capabilities, especially on the part of those in positions of power.”

That pretty much sums up the psychology behind the ongoing debacle that is Peregrine Financial, whose founder and CEO, Russell Wasendorf, Sr., was indicted in Cedar Rapids, Iowa, on Monday on 31 counts of lying to U.S. financial regulators.

By his own admission, Wasendorf bilked investors out of nearly $100 million over the course of nearly two decades (just days before his arrest, the National Futures Association reported a deficit of more than $200 million in funds that Peregrine Financial had claimed to be on deposit at U.S. Bank). To hide the theft, he cooked up fake bank statements using Photoshop, Microsoft Excel, and high-quality printers. These he then handed over to Peregrine’s CFO, who appears to have adopted an “OK, you’re the boss” attitude after Wasendorf used what he called “blunt authority” to cow him into submission. Wasendorf seems to have taken special pride in his forger’s art, bragging of how adept he eventually became at falsifying not just hard copies, but online statements as well, none of which the financial regulators appear to have questioned.

Then, this summer, Peregrine hit the wall. Wasendorf couldn’t keep all the balls bouncing. On July 9, he tried to kill himself by inhaling fumes from a hose hooked up to his car’s tailpipe. Needless to say, the firm had been run into the ground. Wasendorf’s son was devastated at finding the company he was supposed to inherit was now a mound of useless paper—and that his father was a crook. Peregrine’s workers were out of a job. And of course, thousands of investors were left holding the bag.

Excessive self-confidence? Check. Grotesque overestimation of one’s abilities? Check. Loss of contact with reality? Check. (Sooner or later someone had to notice that there was no actual money in those U.S. Bank accounts.)

But the hubris didn’t stop there. It was also abundantly on display in Wasendorf’s suicide note, in which, far from showing any remorse, he actually seemed to thumb his nose at financial regulators. Evidently even his would-be last moments were ego-driven:

Where executives [like Wasendorf] have committed crimes, “it is not remorse that motivates” them to kill themselves, said Dr. Alan Berman, executive director of the American Association of Suicidology, a suicide education and prevention group. “Rather it’s a refusal to accept a changed public persona.”

As he prepared to take his life, Wasendorf confessed to massive fraud in a document whose tone often sounded more boastful than ashamed. He explained in detail how he had used “careful concealment and blunt authority” to steal hundreds of millions of dollars over two decades from clients of his brokerage firm. His scheme to falsify bank statements and balance sheets started 20 years ago, he wrote, because “my ego was too big to admit failure.”

In the cases of executive criminals, Berman said that “the suicide dies having preserved in his mind that the world’s view of him will remain that of before his death. Death is preferred to losing face, suffering media coverage of the felonious behavior, prison and other consequences.”

Incredible, an ego that massive. But seeing as how egotistical delusions are the enemies of realistic risk assessment pretty much 100% of the time, investors would do well to take a cold shower before forking over money to any proposal that appears too good to be true. Specifically, they should learn to recognize Ponzi schemes, of both the Waserdorf and the Bernie Madoff variety. These schemes have several tell-tale traits:

- They promise minimum or steady returns;

- They claim their opportunities are exclusive, available only to a select few;

- Their means of making money is too complicated or secret to explain;

- They make it difficult to withdraw your money, saying that funds have been frozen;

- They issue statements that lack detail, or that frequently show discrepancies that cannot be explained;

- They are frequently run by a single individual whose charm and charisma allow him maximum leverage over investors’ fears—and greed.

Con artists like Wasendorf prey upon the egotistical hopes and equally egotistical anxieties that come out in just about all of us whenever money is involved. Knowledge and financial realism are their enemies. That’s why, whenever you’re about to embark on a new financial venture, it pays to check your ego at the door.

-

The Lagging Defense Sector

Eddy Elfenbein, January 31st, 2013 at 1:52 pmLower military spending put a big dent into yesterday’s GDP report. For investors, the defense sector has been a laggard. It was a market performer during 2008 and the first half of 2009. But for the last two-and-a-half years, the S&P 500 has left it in the dust.

-

Jobless Claims Rise to 368,000

Eddy Elfenbein, January 31st, 2013 at 9:59 amThis morning, the Labor Department reported that weekly jobless claims rose by 38,000 last week to 368,000. That’s the biggest increase since November. Wall Street had been expecting an increase of 20,000, but the claims recent reports have been very positive.

We’re coming off five-year lows, so today’s report should be seen in some broader context. Another possibility is that claims are truly around 360,000 and the earlier reports were just noise. It’s hard to say but we’ll get the big jobs report tomorrow when the government reports the non-farm payrolls and unemployment rate for January.

We also learned that personal income rose by 2.6% last month. That’s a bit distorted because a lot of rich folks pulled in a little extra cash in order to avoid higher taxes this year.

The market is currently up about one point to 1,503. Yay, no volatility.

-

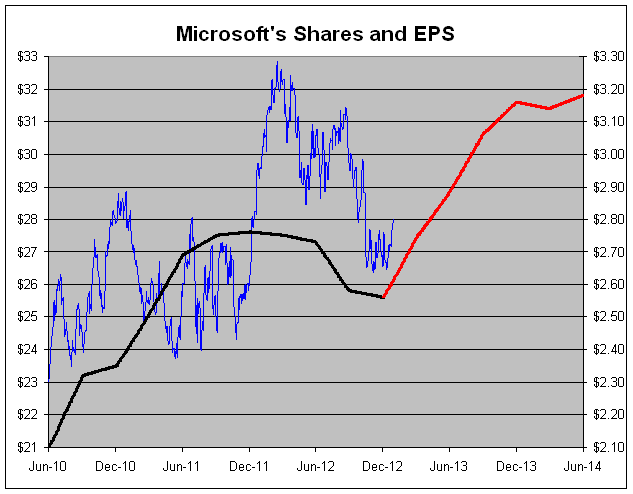

How Much is Microsoft Worth?

Eddy Elfenbein, January 31st, 2013 at 8:03 amLast week, Microsoft ($MSFT) finally delivered a decent earnings number. The company earned 76 cents per share which was a penny ahead of expectations. The quarter before that, MSFT missed by three cents per share, and Wall street was not pleased.

Microsoft’s fiscal year ends in June, and the company is on track to earn about $2.85 per share, give or take. But the stock is only up to $27.85 going by yesterday’s close, and that’s after a small rebound. MSFT certainly has its problems, but I would think the world’s largest software outfit could command a P/E Ratio greater than 10.

Here’s a look at Microsoft’s stock and earnings over the past few years. The stock is the blue line and it follows the left scale. The earnings are in black and they follow the right scale. I scaled the two lines at a ratio of 10-to-1 so whenever the lines cross, the stock’s earnings multiple is exactly 10. The red line is Wall Street’s earnings projections.

The stock gapped up between November 2011 and March 2012 and investors expected an earnings rebound. It didn’t come. If — and this is a strong if — Wall Street’s earnings forecast is correct, MSFT’s stock should rebound this year. And that’s going by very modest valuations.

To get a good idea of what a fair value is for Microsoft, let’s look at my “world’s simplest stock valuation measure.” The equation is:

Growth Rate/2 + 8 = PE Ratio

For Microsoft, the expected five-year earnings growth rate is 8.38%. The calendar year 2013 earnings estimate is $3.16 per share. That gives us a fair value of $38.52 which means the stock is 28% undervalued.

Please bear in mind that my little equation isn’t a precise measure of true value. It’s a ballpark guideline of what might be a good value. What it really tells us is that investors don’t like Microsoft and they’re steering clear of it, but the recent earnings report had many hopeful signs. For example, the company is seeing renewed strength among its business clients.

Microsoft isn’t in good shape but it’s not nearly as dire as the share price suggests. If the company continues to deliver earnings like last quarter, I think the shares could break $37 before the end of the year.

-

Morning News: January 31, 2013

Eddy Elfenbein, January 31st, 2013 at 7:20 amReal Estate Losses Weigh On Santander

Philippine Fourth-Quarter GDP Growth Holds Above 6% on Spending

Deutsche Bank Posts $3 Billion Loss on Job Cuts, Capital

Economy’s Slight Shrinkage Late Last Year Surprises Experts

Federal Rule Limits Aid to Families Who Can’t Afford Employers’ Health Coverage

Biggest Defense Spending Dive Since Vietnam Shows Risk of Cuts

Facebook’s Mobile Ad Push Takes Toll On Profit

Honda Sees Quarterly Profits Rise But Cuts Annual Forecast

Shell Profit Up on Refining Margins

AstraZeneca Forecasts Lower Profit Amid Generic Pressure

Diageo Maintains Profit Growth With Move Away From Europe

BlackBerry, Rebuilt, Lives to Fight Another Day

Credit Writedowns: Going For Broke

Epicurean Dealmaker: Where Angels Fear to Tread

Be sure to follow me on Twitter.

-

Nicholas Financial Earned 37 Cents Per Share

Eddy Elfenbein, January 30th, 2013 at 4:48 pmNicholas Financial ($NICK) earned 37 cents per share for the December quarter which is their Q3. Don’t worry, they had a six-cent charge related to the special dividend. Except for that, these results were largely what I expected.

Nicholas Financial, Inc., announced that for the three months ended December 31, 2012 net earnings decreased 15% to $4,566,000 as compared to $5,363,000 for the three months ended December 31, 2011. Per share diluted net earnings decreased 18% to $0.37 as compared to $0.45 for the three months ended December 31, 2011. Revenue increased 4% to $17,889,000 for the three months ended December 31, 2012 as compared to $17,140,000 for the three months ended December 31, 2011.

For the nine months ended December 31, 2012, net earnings decreased 7% to $15,101,000 as compared to $16,186,000 for the nine months ended December 31, 2011. Per share diluted net earnings decreased 9% to $1.24 as compared to $1.35 for the nine months ended December 31, 2011. Revenue increased 4% to $52,940,000 for the nine months ended December 31, 2012 as compared to $50,985,000 for the nine months ended December 31, 2011.

“During the three months ended December 31, 2012, our results were affected by an increase in the net charge-off rate and an after-tax charge of $747,000 or $0.06 per share, which is related to a 5% withholding tax associated with the one-time special cash dividend of $2.00 per share paid in December 2012. The withholding is required under the Canada-United States Income Tax Convention. While competition remains fierce, we are committed to maintaining our conservative underwriting principles. We will continue to develop additional markets and expect to continue our branch network expansion”, stated Peter L. Vosotas, Chairman and CEO.

A few few things to note. Operating costs rose by 6.3% over Q4 2011 which is steeper than I expected. The provision for credit losses jumped to $819,000 last quarter. That’s the most in two years. We knew the ultra-low numbers weren’t going to last forever, but this provision is still well below what NICK had been setting aside a few years ago.

Outside that and the special dividend taxes, the numbers here are almost the same as the previous few quarters. The portfolio’s gross yield is the highest in four years. Even with the dividend tax, the pre-tax yield is over 10%. During the financial crises and recession, NICK wasn’t able to hit 10% pre-tax for more than three straight years. Without the dividend tax, NICK would have earned 43.6 cents per share last quarter.

-

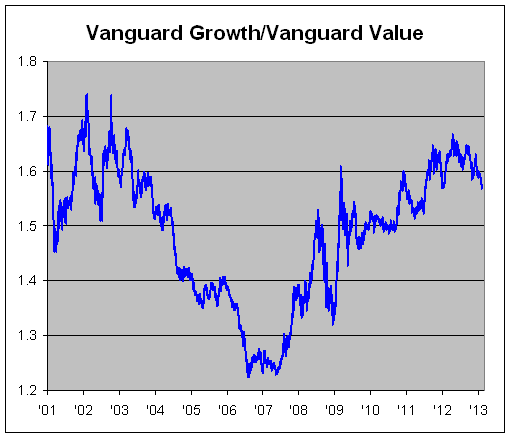

Has Value Turned a Corner?

Eddy Elfenbein, January 30th, 2013 at 3:01 pmHere’s a look at the Vanguard Growth Fund (VIGRX) divided by the Vanguard Value Fund (VIVAX). I use these two mutual funds as proxies to see where we are in the growth-value cycle. When the line is rising, growth is leading and when it’s falling, value is leading.

The market was in a growth cycle from August 8, 2006 until April 13, 2012. Value has done well over the last nine months but I think it’s too early to say whether or not this is a multi-year trend. There have been more prominent breakdowns along the way so this could be just another.

Value generally does better when short-term rates are rising. Since rates are at 0%, and have been for a while, growth and value haven’t diverged that much. Once the Fed finally moves, this will probably change very quickly.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His