Author Archive

-

CWS Market Review – April 5, 2019

Eddy Elfenbein, April 5th, 2019 at 7:08 am“Investing isn’t about beating others at their game. It’s about controlling yourself at your own game.” – Benjamin Graham

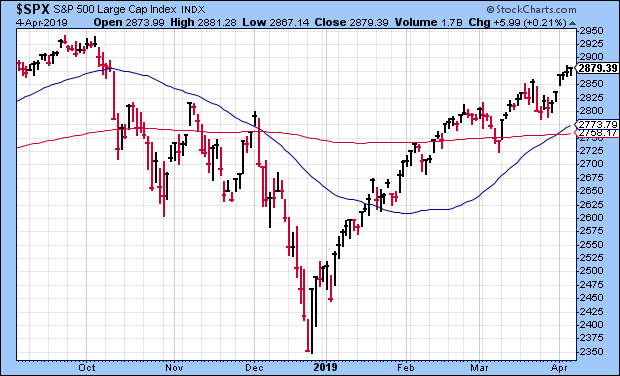

T.S. Eliot famously wrote that “April is the cruelest month.” Actually, as far as stocks go, it’s been pretty good. The market has risen 12 times over the last 13 Aprils. Plus, April 2019 has gotten off to a solid start. This builds upon a very good start to the year. We just wrapped up the best first quarter for stocks in 21 years.

That could be a good omen. Consider that of the last 19 times that each of the first three months of the year were higher, 18 times the rest of the year was green as well. The only exception came in 1987.

During the day on Wednesday, the S&P 500 got as high as 2,885. That’s a six-month high. In fact, we’re not that far from an all-time high. The dividend-adjusted S&P 500 came within 0.5% of making a new all-time high. (Dividends are small, but they do add up!)

The market has now rallied for six days in a row. Despite the rebound in share prices, I have to confess that there’s not a lot going on in the stock market right now. Each week, I strive to bring the latest and greatest on Wall Street, but it’s been quite dead lately.

We’re in that odd lull before earnings season. In just a few days, we’ll have all the news we can bear. But for right now, it’s crickets out there. Don’t fret. In this week’s CWS Market Review, we’ll take a look at some recent economic data. I’ll also run through the new earnings report from RPM International. Plus, I’ll cover some news impacting our Buy List stocks. But first, let’s review some mildly weak economic news.

The U.S. Economy May Be Stagnating

In recent weeks, there’s been more talk about the possibility of an interest-rate cut by the Federal Reserve. Larry Kudlow, the president’s top economic advisor, said the Fed should cut rates immediately by 0.5%.

Until now, I’ve been a doubter, and I still think it’s a long shot. But I’ve become somewhat less doubtful. What’s the reason? Well, some recent economic news has been noticeably tepid. The standout example is the February jobs report. According to the government number crunchers, the U.S. economy created just 20,000 net new jobs in February. That was way below expectations.

I’m writing this to you on Friday morning, so the March jobs report may already be out by the time you’re reading this. That report includes a revision to the numbers from February, and it’s likely the revision is higher.

But that’s not the only data. For example, the weekly jobless-claims report got weaker at the start of this year. The weakness seemed to coincide with the government shutdown, so it caused a major uproar. Sure enough, on Thursday, we learned that initial jobless claims fell to 202,000. That’s the lowest since the 1960s.

On Wednesday, the ADP payroll report said that just 129,000 private sector jobs were created last month. That’s the lowest figure in 18 months. For the first time since December 2016, goods-producing jobs shrank. It’s possible that the labor market is beginning to stagnate as global growth is softening.

That’s probably what’s driving the talk of a rate cut. What’s interesting is that the yield curve isn’t exactly flat. Rather, it has a notch. At the moment, yield on the six-month Treasury exceeds the yield on the three-year by 16 basis points. That’s very unusual, and it only makes sense if bond traders expect a short-lived rate cut in a larger tightening cycle.

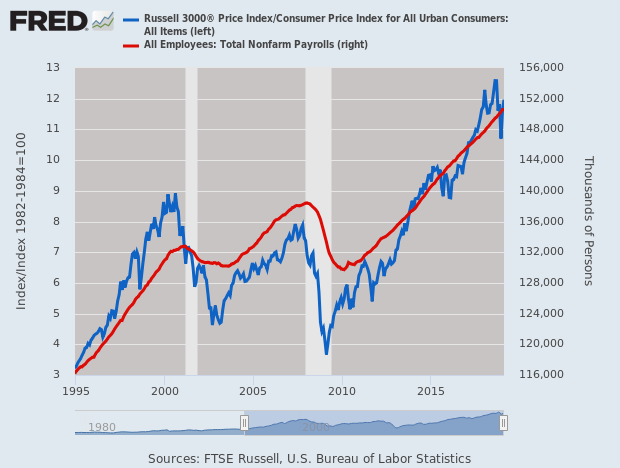

Here’s a chart of nonfarm payrolls (red) with the Russell 3000 adjusted for inflation (blue).

Last week, the government lowered its estimate on Q4 GDP growth. The initial report said the U.S. economy grew by 2.6% in the last three months of 2018. The updated report lowered that figure to 2.2%. That basically puts Q4 right in line with the trend of the current expansion. The economic recovery is notable for its length and its meandering speed. Compared with previous recoveries, the current one hasn’t been particularly strong.

On Monday, the ISM Manufacturing Index was reported to be 55.3 for March. That’s up from 54.2 in February, but that report was the lowest in six months. A recession usually aligns with an ISM reading somewhere in the mid-40s. On Wednesday, the Non-Manufacturing Index fell to 56.1 for March. That’s down from 59.7 for February. That was below expectations, and the lowest point since August 2017.

As I mentioned before, there hasn’t been much happening on Wall Street this week, but that will soon change. Next Friday, earnings season will kick off when JPMorgan and Wells Fargo report earnings. As we stand at the beginning of earnings season, the wave of lower guidance seems to have passed. Since September, Wall Street analysts had chopped this year’s earnings estimate for the S&P 500 by 5% to $167.80. Apple and the Energy sector were key drivers in the lower estimates. Analysts now expect to see top-line growth of 4.4% and an earnings decline of 9.8%.

The week after next, the first of our Buy List stocks will report. Between mid-April and early May, 20 of our 25 Buy List stocks will report earnings. I don’t have the complete list yet, but Eagle Bancorp (EGBN) will report on April 17; then Danaher (DHR) and Check Point (CHKP) will report on the 18th. There will probably be others. Overall, I expect more good results from our stocks. On Thursday, we got the latest off-cycle earnings report from a Buy List stock, and it was quite good.

RPM International Is a Buy up to $65 per Share

In last week’s issue, I confessed that RPM International (RPM) has been a disappointment this year. The January earnings report was a dud, and the company had some (to my ears) tired excuses. Still, I’m not ready to pull the plug. The company owns a broad selection of well-known brands like Rust-Oleum.

The good news is that Thursday’s earnings report alleviated some of my concerns. For the third quarter of RPM’s fiscal year, the company earned 14 cents per share. That exceeds the company’s own range of 10 to 12 cents per share. I’ll note that Q3 is typically RPM’s slowest of the year. Quarterly sales rose 3.4% to $1.14 billion. For the year, sales are up 5.3%.

Frank Sullivan, RPM’s president and CEO, said, “Organic growth was 4.3% and acquisitions contributed 2.1%, while foreign exchange was a significant headwind that reduced sales by 3.0%. Price increases helped to offset higher raw-material costs, which have risen for seven straight quarters, as well as higher costs for freight, labor and energy. International markets remained challenged and resulted in reduced operating earnings from most geographies around the world.” The currency issue is a big problem for RPM.

The good news is that RPM provided a pretty optimistic forecast. The company sees Q4 earnings ranging between $1.12 and $1.16 per share. At one point on Thursday, shares of RPM gapped up nearly 8%. RPM eventually finished the day at $60.63 per share for a gain of 2%.

This is an encouraging report. The major concern is still the currency issue, but RPM doesn’t have much control over that. Remember that this is a solid outfit. RPM has increased its dividend every year for the last 45 years. This week, I’m raising my Buy Below on RPM International to $65 per share.

Buy List Updates

Earlier this week, shares of Raytheon (RTN) were downgraded by UBS. I usually ignore these news items, and I’m not going to bother refuting them. Still, the downgrade was enough to ping the shares for a 4% loss on Wednesday. The analyst lowered Raytheon from buy to neutral. (I’m not neutral on any stock!) He also lowered his price target from $220 to $200 per share, which is still a pretty juicy target. Anyway, I’m not concerned by the downgrade and am expecting good earnings later this month. Raytheon is a buy up to $190 per share.

This Thursday, April 11, is a big one for Disney (DIS). At 5 p.m. ET, Disney will have its Investor Day webcast. With the big Fox deal done, this is the day when Bob Iger is expected to map out Disney’s plans to take on Netflix. Goldman Sachs recently said, “it is the dawn of a new era at Disney.” That’s true.

Going into the meeting, there seems to be a lot of negative sentiment. Some folks think it will be bad news, and that may be what’s weighing on the share price. Personally, I have a more faith in Disney. Plus, with expectations so low, it may be easy to impress investors. Disney remains a buy up to $118 per share.

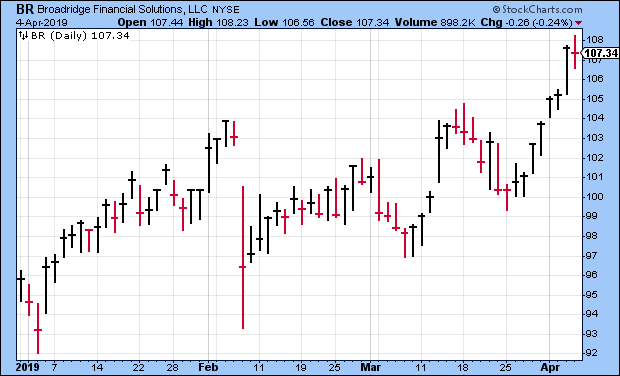

I’ve neglected discussing Broadridge Financial Solutions (BR), and that should change. In February, the shares got smacked down after a lousy earnings report. BR made 56 cents per share, 15 cents below expectations. Despite the big drop, Broadridge has gradually recovered, and the stock just hit a new YTD high.

The rally shouldn’t be too surprising. Broadridge has maintained a favorable outlook. The company said it sees earnings growth of 9% to 13% for this fiscal year, which is already half over. Since they made $4.19 per share last year, the guidance works out to $4.57 to $4.73 per share this year. For the current quarter, Broadridge sees revenue between $1.195 billion and $1.245 billion and earnings of $1.40 to $1.56 per share. Look for some improved results in May. This week, I’m raising my Buy Below on Broadridge Financial Solutions to $113 per share.

That’s all for now. There are a few key economic reports next week. On Monday, the factory-orders report comes out. On Wednesday, we’ll get the CPI report for March. Also on Wednesday, the Fed will release the minutes from its last meeting. The jobless-claims report comes out on Thursday. On Friday, the Q1 earnings season begins as JPMorgan and Wells Fargo are due to report earnings. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. I’ll be on Bloomberg TV’s market-wrap segment this Monday, April 8 at 3:50 pm ET.

-

Morning News: April 5, 2019

Eddy Elfenbein, April 5th, 2019 at 7:02 amIndia’s Central Bank Cuts Key Lending Rate to 6.0%

‘Epic’ China Trade Deal Near Completion, Trump Says, but Haggling Continues

China Hails ‘New Consensus’ on Trade as Trump Talks Up Unfinished Deal

Manufacturing Surge, a Boon for Trump, May Be Fading

U.S. Job Growth Seen Accelerating From 17-Month Trough

What Will Cause the Next Debt Crisis?

Why Soft Power Is in Style in Qatar

Gun Control Group’s Report Card on U.S. Banks’ Firearms Ties Has Several Fs

Jeff Bezos Keeps Amazon Voting Power in Divorce Settlement

Ghosn’s Fate May Hang on Complex Financial Web in Middle East

Jeff Carter: Dual Sides of Student Debt

Ben Carlson: 7 Benefits of Writing

Joshua Brown: Josh and Michael on Taxes, a16z, Netflix for Financial Planning, New S&P 500 Highs

Be sure to follow me on Twitter.

-

Morning News: April 4, 2019

Eddy Elfenbein, April 4th, 2019 at 7:05 amFrom Molecules to Electrons; Can Big Oil Become Big Power?

Trump to Meet China’s Liu in a Sign Trade Talks Are Reaching Final Stages

A.I. and Privacy Concerns Get White House to Embrace Global Cooperation

America’s Biggest Economic Challenge May Be Demographic Decline

Stung by Big Fines, Big Banks Beef Up Money-Laundering Controls

Elite U.S. School MIT Cuts Ties With Chinese Tech Firms Huawei, ZTE

PG&E Reveals New C.E.O. & Revamped Board of Directors

Constellation to Sell Several Wine Brands to Gallo in $1.7 Billion Deal

Tesla’s Elon Musk to Square Off With SEC in Court at Contempt Hearing

This Startup Wanted to Change the Way Drugs Are Sold. Then Things Got Messy

Lyft Is Luring Investors, Just Not the Kind It Wants

Ex-Nissan Chief Ghosn Calls Latest Arrest ‘Outrageous’, Asks French Government to Help

Jeff Miller: You Risk How Much Per Trade?

Joshua Brown: A Man and His Signals

Howard Lindzon: Doing The Impossible

Be sure to follow me on Twitter.

-

Morning News: April 3, 2019

Eddy Elfenbein, April 3rd, 2019 at 7:09 amWorld Stocks Rally to Six-Month Highs on U.S.-China Trade Optimism

Japan Stumbles as China’s Growth Engine Slows

The Decade of Deleveraging Didn’t Quite Turn Out That Way

Amid Bitcoin Uncertainty, ‘the Smart Money Knows That Crypto Is Not Ready’

Fed Risks Stoking Financial Bubble in Drive to Lift Inflation

Drug Sites Upend Doctor-Patient Relations: ‘It’s Restaurant-Menu Medicine’

Japan Display to Supply OLED Screens for Apple Watch

Roche Says $4.3 Billion Spark Offer Still On Track for June Completion

Wells Fargo CEO Stumble Puts Bank in Familiar State of Disarray

Deutsche Bank’s U.S. Unit Kept Danske’s Shady Billions Flowing

Novartis’s Alcon spinoff ousts Baer from Swiss benchmark SMI

Walgreens CEO Loses $1.2 Billion in One Day

Ben Carlson: So I Tried Cutting the Cord…

Michael Batnick: Animal Spirits: Netflix for Financial Planning

Be sure to follow me on Twitter.

-

Morning News: April 2, 2019

Eddy Elfenbein, April 2nd, 2019 at 7:11 amAll the Reasons to Fret About the Global Economy, in Charts

Trade Slowed in Fourth-Quarter, WTO Says; Auto Tariffs, Brexit Are 2019 Risks

Bitcoin’s Sudden Surge Propels It Above $5,000

Amid Bitcoin Uncertainty, ‘the Smart Money Knows That Crypto Is Not Ready’

For Many British Businesses, Brexit Has Already Happened

A Key to the Arctic’s Oil Riches Lies Hidden in Ohio

Exxon Weighs Sale of Nigerian Oil and Gas Fields for Up to $3 Billion

Shell to Quit U.S. Refining Lobby Over Climate Disagreement

YouTube Executives Ignored Warnings, Letting Toxic Videos Run Rampant

U.S. Moves to Limit Wage Claims Against Chains Like McDonald’s

General Electric Earnings Still Won’t Matter, but Cash Flow Will

Cullen Roche: Odd Lots Podcast – Talking MMT

Joshua Brown: What if You Only Invested in Your 20 Best Ideas?

Howard Lindzon: Momentum Monday – America is Hungry

Be sure to follow me on Twitter.

-

Econ Update

Eddy Elfenbein, April 1st, 2019 at 1:44 pmWe got a few economic reports this morning. The ISM report rose to 55.3 from 54.2 in February. That’s a pretty good number.

The retail sales report showed a drop of 0.2% in February. The number for January was revised higher to 0.7% from 0.2%. Wall Street had been expecting an increase of 0.3%.

The best news was that construction spending rose 1% in February. This data series is now at a nine-month high.

-

What If the Bull Market Ended 14 Months Ago?

Eddy Elfenbein, April 1st, 2019 at 10:03 amConventionally, we measure bull markets from their lows to their highs, and that’s probably as it should be. But what if we broke the rules by a little?

If you allow me a little latitude, I propose that we can say that the bull market ended on January 26, 2018 when the S&P 500 closed at 2,872.87.

Well, yes, technically that is correct. By August, the S&P 500 broke that peak, but here’s my point—it didn’t break it by much. On a closing basis, the S&P 500 topped out at 2,930.75 on September 20, 2018. That’s a gain of 2.01% in the eight months from the January top.

Two percent in eight months ain’t that great. Let’s bear in mind that from the March 2009 low to the January 2018 peak, the stock market averaged a gain of more than 17.6% per year.

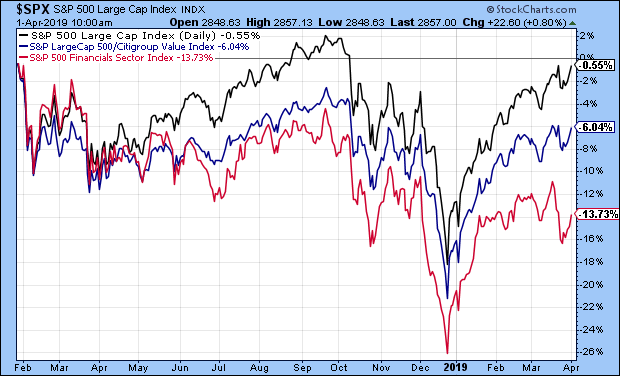

Many sectors and individual stocks never made new highs, and they’re still well below their January 2018 peak. For example, the S&P 500 Value Index never made a new high. It’s currently 6% below its peak from 14 months ago. The S&P 500 High Beta Index also never made a new high. The Consumer Staples sector is way down from its peak. The S&P 500 Industrials also never made a new high. Fourteen months later, the overall S&P 500 is still below that early 2018 top.

This chart shows the S&P 500 in black along with the S&P 500 Value Index in blue and the S&P 500 Financials in red.

So what did make a new high? Tech, and lots of it. The Nasdaq Composite and the Nasdaq 100 have done very well.

Except for a nasty spill in December, the market hasn’t experienced gigantic losses over the last 14 months. Perhaps this is a stealth bear market. Instead of tumbling for a big loss, it’s simply not doing much of anything for an extended time.

-

Morning News: April 1, 2019

Eddy Elfenbein, April 1st, 2019 at 7:03 amGerman Factory Slump Leaves Euro Area as Global Economic Laggard

U.S.-China Trade War Timeline: What’s Happened in 2019 So Far

China Purchases Could Undercut Trump’s Larger Trade Goal

Denmark’s DSV to Buy Logistics Company Panalpina in $4.6 Billion Deal

Mark Zuckerberg’s Call to Regulate Facebook, Explained

Peter Thiel and Li Ka-shing Have a Banking App for America’s Generation Z

Burger King Tests Plant-Based Meat With an Impossible Whopper

Aramco Eclipses Top Earner Apple Ahead of Debut $10 Billion-Plus Bond Sale

Lyft’s IPO Pop Is Evidence Of Failure, Not Success

Could Elon Musk’s Rap Song Actually Be Good News About Tesla’s Quarterly Deliveries?

South Korea’s Burned Out Millennials Choose YouTube Over Samsung

How Sovereign Citizens Helped Swindle $1 Billion From the Government They Disavow

Howard Lindzon: What’s In a Name

Ben Carlson: Real Estate vs. The Stock Market

Michael Batnick: These Are the Goods

Be sure to follow me on Twitter.

-

CWS Market Review – March 29, 2019

Eddy Elfenbein, March 29th, 2019 at 7:08 am“The conventional view serves to protect us from the painful job of thinking.”

– John Kenneth GalbraithAfter ten years, the yield curve has finally gone flat. Ironically, this was caused by good economic news. A flat curve is a natural response to a growing economy, but the flat curve has some important implications for the economy, the stock market and our portfolios.

In this week’s CWS Market Review, we’ll take a deep dive into all things yield curve. I’ll also discuss the good earnings report from FactSet. The stock gapped up to a new 52-week high. I’ll also preview next week’s earnings report from RPM International, and I have a bunch of new Buy Below prices. But first, let’s look at what the yield curve has to say.

What Does the Flat Yield Curve Mean?

Wall Street has been in a tizzy over the yield curve. As we know, Wall Street loves to stress about something. Or anything. Wall Street’s favorite mode is being “concerned.” If need be, this can be upgraded to “distressed.” Most of the time, I tell you that this week’s “concern of the year” is over-rated and not to worry about it.

This is different. An inverted yield curve truly is a big deal. The hitch is that it’s not immediate. Let me take a step back. By yield curve, I mean the difference between short-term and long-term interest rates. Normally, the yield curve is upward sloping, meaning you get paid more the longer you lend your money. That makes sense, but every so often, the yield curve goes flat, or even gets inverted. That’s when short-term rates rise above long-term rates.

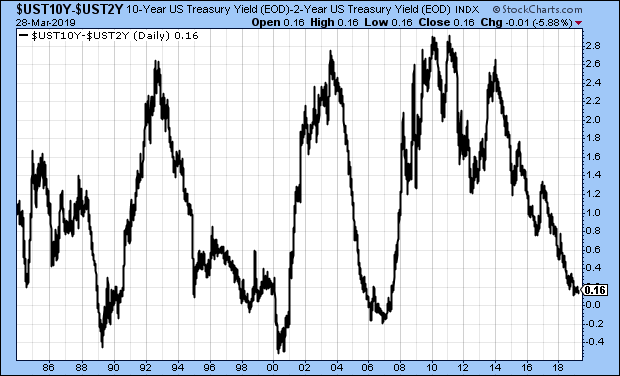

An inverted yield curve is one of the few good predictors of a bad economy. For a field with lots of stats, we still have little idea of how well the economy is doing at the moment. Economists have a terrible track record of predicting recessions, but the yield curve could have won a few Nobel Prizes based on its track record. The spread between the 2- and 10-year Treasuries has been an omen of bad times consistently for the last 35 years.

Check out this tidbit from MarketWatch:

Researchers at the San Francisco Fed say the 3-month/10-year curve is the most reliable indicator, while Cleveland Fed researchers note that inversions of that measure have preceded the past seven recessions with only two false positives — an inversion in late 1966 and a very flat curve in late 1998.

That’s way better than most economists.

To show you how much things have changed, in 2011, the 2/10 Spread reached 291 basis points. It’s now down to 16. The spread between the 10-year and three-month yield is currently negative by four basis points.

While the yield curve is important, I’ll caution you that it’s not an instant tripwire. Let’s look at some recent history. The 2/10 Spread inverted in May 1998. It then went back before becoming very inverted in 2000, but the recession didn’t officially begin until 2001. Even in the last recession, the 2/10 Spread inverted in late 2005. The recession didn’t start for two more years.

It’s a mistake to dismiss the yield curve as a technical indicator like the 200-day moving average. The yield curve has real world ramifications. A few years ago, I ran the numbers and found that the stock market does much better when the spread between the 90-day and 10-year Treasury yield is 121 basis points or more. If you’re a bank, an inverted curve means it’s not profitable to borrow short and lend long. (And yet, starting a bank in 2010 was probably one of the most profitable things you could do.)

In the 12 months following a negative 2/10 Spread, the economy has been in recession about 50% of the time. There is, however, the chance that the yield curve may have lost its predictive powers with the advent of the Fed’s new policies. These things can change. When we had a gold standard, inverted curves were the norm.

I don’t have any plans to alter our investing strategy. Our stocks are stronger than what a yield curve can do. With a flat curve, I would expect to see better valuations among defensive stocks. As I’ll explain later, stocks like Hershey (HSY) and Church & Dwight (CHD) have recently hit new highs. Think of it this way: an inverted yield curve is like rougher seas. If your ship is sturdy, then it doesn’t matter.

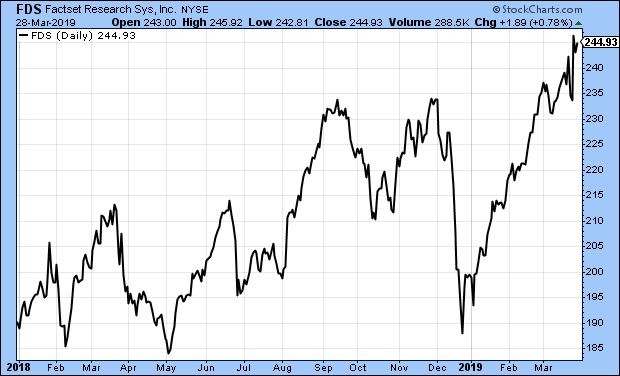

FactSet Is a Buy up to $258 per Share

On Tuesday, FactSet (FDS) reported earnings for its fiscal second quarter and the results were pretty good. This is for the quarter that covered December, January and February.

For Q2, FactSet earned $2.42 per share compared with $2.12 per share last year. Wall Street had been expecting $2.33 per share. Quarterly revenue rose 5.9% to $354.9 million, and organic revenue rose 5.7%. Annual Subscription Value, or ASV, rose to $1.44 billion. I was pleased to see that FactSet increased its adjusted operating margin to 33.2% from 31.4% a year ago.

“As we close the first half of the year, we are pleased to have built upon our long track record of continuous and steady growth. Our team capitalized on growing demand for our core solutions with focused execution as we continued to serve as a trusted partner to our clients,” said Phil Snow, FactSet CEO. “Looking ahead to the second half of the year, we will continue to execute against our proven strategy of providing smarter, connected data and technology solutions that make for an open and flexible user experience.”

As of the end of the quarter, FactSet has a client count of 5,405. That’s an increase of 108. The user count increased by 6,854 to 122,063. Annual client retention was greater than 95% of ASV.

FactSet also updated its financial guidance. The company expects revenue to range between $1.41 billion and $1.45 billion. They see adjusted operating margin between 31.5% and 33.5%. Lastly, they see full-year earnings between $9.50 and $9.65 per share. That’s an increase of five cents to the low end. This was a solid report for FDS.

After the report, shares of FDS opened higher, then lost it all, then rallied back very impressively. This week, FDS hit a new 52-week high. I’m lifting my Buy Below on FactSet to $258 per share.

Preview of RPM International’s Earnings

We have one earnings report next week. RPM International (RPM) is due to report its fiscal Q3 earnings on Thursday morning, April 4. This will be our final off-cycle report until Q1 earnings season begins in mid-April.

I’ll be honest – RPM has been a disappointment this year. The last earnings report was pretty ugly. For its fiscal Q2, RPM reported earnings of 52 cents per share. Sales rose 3.6% to $1.36 billion. Wall Street had been expecting 68 cents per share.

The CEO had some excuses: “Like many manufacturers, our bottom line was impacted by a continued rise in costs for raw materials, freight, labor and energy, as well as adverse foreign-exchange translation.” We already knew the company was facing these issues, but I didn’t realize the problem was so acute. For Q3, RPM expects earnings between 10 and 12 cents per share.

I’m not done yet with RPM. There’s still a lot of time to turn things around, but I want to see some evidence soon. All companies hit rough patches, but not all manage through them the same.

Buy List Updates

Continental Building Products (CBPX) rallied after its last earnings report. Since then, it’s given back the entire gain, and then some. I still like Continental and this is a good price. This week, I’m dropping my Buy Below down to $26 per share.

Eagle Bancorp (EGBN) is another good stock that’s been weak lately. In five trading days, EGBN fell 13%. I’m not worried about Eagle. The stock is going for about ten times this year’s earnings. I’m lowering my Buy Below to $55 per share.

Remember when Church & Dwight (CHD) fell sharply after missing earnings by one penny? The stock lost more than 7% in one day. As it turns out, a stock that’s raised its dividend for 23 years in a row is worth sticking with. Since then, CHD made back everything it lost and just hit a 52-week high on Thursday. I’m raising my Buy Below on CHD to $75 per share.

There are a few other Buy Below changes I want to make. Fiserv (FISV) continues to look very good. I’m expecting another good earnings report. This week, I’m lifting our Buy Below on Fiserv to $92 per share. Hershey (HSY) is another stock that just hit a 52-week high. I’m raising our Buy Below on Hershey to $120 per share. JM Smucker (SJM) is doing very well this year. The jam stock is up 24% for us so far in 2019. I’m increasing the Buy Below on SJM to $122.

That’s all for now. The first quarter ends with the close of trading today. This looks to be one of the best quarters for the stock market in years. The second quarter starts up next week. On Monday, we’ll get the ISM and retail sales reports. Tuesday is durable goods. Then on Wednesday, we’ll see the ADP payroll report. That leads up to the March jobs report on Friday. The last report was quite low. I’ll be curious to see if it gets revised higher. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: March 29, 2019

Eddy Elfenbein, March 29th, 2019 at 7:02 amLira Wobbles as U.S. Ties With Turkey Fray

China, U.S. Pore Over Details of Agreement Text to End Trade War

A Tax On A Tax: U.S. Customs Demands Bigger Bonds as Trade Tariffs Rise

The ETF Tax Dodge Is Wall Street’s “Dirty Little Secret”

Un-Spinning the Trump, Obama GDP Numbers

Lyft’s Trading Debut to Be Watched by IPO-Hungry Tech Companies

Who’ll Get Rich When Lyft, Uber and Other ‘Unicorns’ Go Public

Goldman’s China-Backed Fund Bucks Trade Tensions to Buy U.S. Firm

Huawei Shrugs Off U.S. Clampdown With a $100 Billion Year

Wells Fargo C.E.O. Timothy Sloan Abruptly Steps Down

JPMorgan’s Role in Nigerian Oil Deal Has Come Back to Haunt It

Joshua Brown: An Economist Walks Into a Brothel & Non-Partisan

Cullen Roche: Three Things I Think I Think – Yield Curves and Stuff

Ben Carlson: Personal Finance For Normal People

Michael Batnick: The Perfect Track Record & Eye Roll

Be sure to follow me on Twitter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His