-

Market Looks to Rally on Yuan News

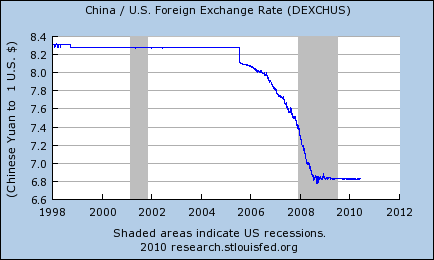

Posted by Eddy Elfenbein on June 21st, 2010 at 9:14 amGood news this morning. The market will most likely get a lift today thanks to China agreeing to let the yuan rise against the dollar. I know currency news is as dull as dirt, but this time it matters. The Chinese currency is now at its highest level in two years and it had its biggest one-day gain in five years.

Let me explain: China keeps a very tight leash on the yuan. Even though this was the biggest move since 2005, the rally was a lousy 0.42%. The Chicoms keep the yuan artificially low and that doesn’t sit well with the rest of the world, including me. One dollar will get you 6.7976 yuan. My take is that this was a just a nice gesture from China ahead of the next G-20 meeting.

The good news for us is that Asian markets like the news a lot. Not surprisingly, the major airline stocks inside China some very good gains. The downside is that oil rose. This makes sense since investors think it will spur greater demand from China.

Reuters lists some of the winners and losers from today’s move. The winners include automakers, consumers and tech, foreign heavy machinery makers, luxury firms and Chinese financials. The losers are foreign financials and commodity firms.

-

No Follow Through

Posted by Eddy Elfenbein on June 16th, 2010 at 9:11 amThe frustrating thing about this market is that there’s zero follow through. Every time we try to rally, we seem to give it all back the next day. For 13 of the last 17 sessions, the market has closed in the opposite direction from the day before.

From April 29 through June 1, the S&P 500 rose just eight times. The following day, every single time, the market closed lower. Since then, only two of the last five rallies have been followed by rallies and both were very modest (about 0.4%).

The S&P 500 hasn’t had a three-day win streak in two months. It looks like we’re going have a lower open. Again.

The only bright spot is over the last nine down days, seven have been followed by rallies. -

Today’s Close

Posted by Eddy Elfenbein on June 15th, 2010 at 5:58 pmWe did it! The S&P 500 barely closed above the 200-DMA. The index is also up for the year — +0.012%!! With dividends, it’s up +0.93%.

-

Fighting the 200 DMA

Posted by Eddy Elfenbein on June 15th, 2010 at 1:58 pmI’ve said before that I’m not a big fan of technical analysis. I make one small exception for looking at the market’s 200 day moving average.

This is the simply the average of the closes for the previous 200 days. The 200 DMA does have a decent track record — when the market is above the 200 DMA, it tends to rally, below it, not so much.

I think this is a good example of a dumb rule that works well (or well enough) for very smart reasons. The key is that the market tends to be a very trend friendly data series. Once things are set in motion, they tend to continue. At least, until they stop.

I think the stock market is pretty cheap right now (but I caution you that my broad market calls aren’t so good), but it looks like investors aren’t ready for a rally. The S&P 500 has tried a couple of times to break out above its 200 DMA but each attempt has sputtered out.

We just peaked above it again today. Let’s see if this is our turning point.

-

“We Can Have the Financial Solvency To Take Hits If We Need To”

Posted by Eddy Elfenbein on June 15th, 2010 at 12:33 pmIn the interest of full disclose, I’ll tell you that I recently bought some shares of AFLAC (AFL) at a price of $42.77. I’ve said that I think it’s very underpriced so that shouldn’t be a big surprise.

The stock is down on, I believe, overblown worries about its exposure to Europe. AFLAC’s CEO Dan Amos recently spoke with the crew at Motley Fool.Aflac’s bottom line is highly correlated with the returns it gets from investing the proceeds from its insurance business. Market volatility makes deciding where to invest a challenge.

As a general rule, Amos said, the company tries not to invest more than $250 million in any one company or country — taking currency fluctuations into account. He said Aflac’s largest investment is in Japanese government bonds. The company invests roughly $20 million per day in Japan within its overall portfolio. (One out of every four households in Japan has an Aflac policy and 80% of Aflac’s earnings and invested income stems from Japan.)

However, Japan doesn’t really have a market for long-dated maturities. “You can find them, but 20-year dated maturities are almost impossible to find,” said Amos. “So to match assets against liabilities, we ultimately had to go other places.”

As such, Amos said, the company does have exposure to Europe via companies and country bonds, including the PIIGS countries: Portugal, Italy, Ireland, Greece, and Spain. Aflac owns shares in the top three banks in England, including Barclays (NYSE: BCS); the top three banks in Germany, including Deutsche Bank (NYSE: DB); and banks in other countries such as Spain. (You can view a list of Aflac’s European exposure here.)

“So, we’ve spread our risk,” said Amos. “[But] it puts us in the light a lot of times because if someone says, ‘Do you own Greece?’ Yes, we own Greece. It’s part of the European common market. We thought that would be safe. So that’s what we’ve done.”

But Amos said his main focus is whether a business’s or country’s bonds will continue to pay. “There can’t be what I call a ‘run on the bank’ in our business,” he said. “There are no cash values. So as long as those bonds are going to pay, then ultimately we’re in a very good position. And we can have the financial solvency to take hits if we need to because we made over $2 billion in profits this year.”Let me also add that Nicholas Financial (NICK) is currently going for $7.88 a share which is more than 5% below its book value.

-

The Higher Ed Bubble

Posted by Eddy Elfenbein on June 15th, 2010 at 11:12 amI’ve written before that the benefits of a college degree are greatly exaggerated. The Los Angeles Times has an article titled “Is a college degree still worth it?”

Here’s a sample:After spending tens of thousands of dollars on higher education, often taking on huge debts along the way, many face a job market that doesn’t seem to need them. Not only is the American economy producing few new jobs of any kind, but the ones that are being added are overwhelmingly on the lower end of the skill and pay scale.

In fact, government surveys indicate that the vast majority of job gains this year have gone to workers with only a high school education or less, casting some doubt on one of the nation’s most deeply held convictions: that a college education is the ticket to the American Dream. -

Flowers Foods

Posted by Eddy Elfenbein on June 14th, 2010 at 2:10 pmFlowers Foods (FLO) is another example of a fairly boring stock that’s done incredibly well for investors. Despite having a market value in excess of $2 billion, Flowers is almost completely ignored by Wall Street. The stock is practically invisible on stock message boards.

So what do they do? Here’s what the company has to say:Headquartered in Thomasville, Ga., Flowers Foods is one of the nation’s leading producers and marketers of packaged bakery foods for retail and foodservice customers. Among the company’s top brands are Nature’s Own, Whitewheat, Cobblestone Mill, Blue Bird, and Mrs. Freshley’s. Flowers operates 40 bakeries that are among the most efficient in the baking industry.

Now let’s look at some results. Thirty years ago, you could have picked up one share of FLO for about 17 cents (that’s adjusted for ten, yes ten, 3-for-2 splits). Today the stock is going for about $25 so that’s a gain of over 14,000% or more than 18% a year. That doesn’t include a dividend which usually yields between 2% and 4%.

Speaking of which, the company just raised its quarterly dividend by 14%, raising it from 17.5 cents a share to 20 cents a share. Going by the new dividend, the stock now yields about 3.2%.

In February, Flowers said that it expects 2010 EPS to increase by 10% to 15% over 2009’s total which came in at $1.38. That translates to a target of $1.52 to $1.59. They reaffirmed this guidance last month as well.

I don’t think Flowers is a take-it-to-the-bank buy right here, but I’d love to see it drop to around $20 a share. This is definitely one to watch.

Year…………………………Sales………………………..EPS

2000…………………….$1,562.88……………………-$0.42

2001…………………….$1,299.49…………………….$0.09

2002…………………….$1,328.61…………………….$0.42

2003…………………….$1,453.00…………………….$0.51

2004…………………….$1,551.31…………………….$0.54

2005…………………….$1,715.87…………………….$0.66

2006…………………….$1,888.65…………………….$0.81

2007…………………….$2,036.67…………………….$1.02

2008…………………….$2,414.89…………………….$1.28

2009…………………….$2,600.85…………………….$1.41 -

Managing Currency Risk

Posted by Eddy Elfenbein on June 14th, 2010 at 11:50 amI noticed this brief article at Dow Jones. It notes that Coca-Cola uses hedges to protect itself from the weaker euro.

Coke’s hedges protect it against the euro for all of 2010, he said. Coke’s hedges aren’t new. The company has long used hedges to protect itself against volatile currencies. Coke already has some currency hedges in place for next year. Multinational companies stand to get hurt from the weaker euro as they convert their earnings in local currencies into dollars. Hedges can help limit the effects of currency fluctuations.

This isn’t a new strategy but it’s interesting to note how you can use investments to lower your currency risk.

A weaker dollar tends to help large-cap stocks since that sector is loaded with multinationals that generate more of their sales outside the U.S. Conversely, a strong dollar tends to help small-cap stocks which tend to be more tied to cyclical industries. -

The Buy List’s Ugly Spring

Posted by Eddy Elfenbein on June 14th, 2010 at 10:47 amI like to tout my Buy List when it does well, so I feel obligated to acknowledge when we don’t do well—and we haven’t been so hot lately. We’re still barely positive for the year and ahead of the market, but our lead has shrunk since April 16. Since then, the S&P 500 has dropped by -8.43% while our Buy List is off by -11.38% (not including dividends).

Make no mistake, I haven’t altered my strategy and I’m still committed to our stocks. I’m merely pointing out that the market hasn’t done well and are stocks are feeling the brunt of the pain. Some of this is probably because higher-quality stocks fared well during more turbulent times. Through Friday, our Buy List is up 0.18% compared with a loss of 2.11% for the S&P 500. That’s still a lead of 229 basis points but the lead was at 615 basis points on April 16.

Here’s how each stock has done since April 16:Symbol Gain/Loss SYY 4.17% JOSB -1.05% BBBY -1.96% RAI -3.32% NICK -6.43% LLY -7.85% WXS -9.30% JNJ -10.09% BDX -10.36% FISV -10.38% SEIC -10.68% SYK -11.62% EV -12.95% INTC -13.71% MOG-A -13.92% MDT -15.08% LUK -21.19% AFL -21.37% GILD -24.44% BAX -29.93% -

Where Are the Men?

Posted by Eddy Elfenbein on June 14th, 2010 at 9:40 amThe Atlantic writes on The End of Men:

Since 2000, manufacturing has lost almost 6 million jobs, more than a third of its total workforce, and has taken in few young workers. The housing bubble masked this new reality for a while, creating work in construction and related industries. Many of the men I spoke with had worked as electricians or builders; one had been a successful real-estate agent. Now those jobs are gone too. Henderson spent his days shuttling between unemployment offices and job interviews, wondering what his daughter might be doing at any given moment. In 1950, roughly one in 20 men of prime working age, like Henderson, was not working; today that ratio is about one in five, the highest ever recorded.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His