-

Lockhart: Time to Start Thinking About Raising Rates

Posted by Eddy Elfenbein on June 3rd, 2010 at 9:54 amI’ve been saying that the Federal Reserve will probably raise interest rates before most people expect. Since last March, we’ve been in a Golden Period for stocks investors with very low interest rates and steeply low equity prices. Of course, equity prices are now no longer as low as they used to be. This may soon come to an end and today we got confirmation from Dennis Lockhart, the president of the Atlanta Fed.

The U.S. economy is almost strong enough to allow the Federal Reserve to begin thinking about raising interest rates, Atlanta Fed President Dennis Lockhart said on Thursday.

While he noted unemployment would likely remain elevated for some time, Lockhart said the U.S. central bank should not wait too long before beginning to tighten the reins.

“The time is approaching when it will be appropriate to consider recalibrating interest rate policy. I do not believe that time has yet arrived,” Lockhart told .

“As the economy continues to improve and financial markets find firmer ground, extraordinarily low policy rates will not be needed to promote recovery and will become inconsistent with maintaining price stability.”

In response to the most severe financial crisis in generations, the Fed not only slashed interest rates effectively to zero but also undertook a host of emergency measures such as buying up Treasury and mortgage bonds.

Lockhart’s comments mark a significant change in tone for the regional Fed president, who has been among the most dovish on the central bank’s policy in recent months. They suggest firmer growth in the United States is catching the attention of Fed policymakers, despite the renewed risks to the outlook from the turmoil surrounding European debt markets.The timing of a rate increase is still an issue. I think it could happen by the end of the summer. I also think the Fed may raise the Fed Funds rate by 50 or 75 basis points.

-

Bullet Bob Feller

Posted by Eddy Elfenbein on June 2nd, 2010 at 2:56 pm

At my town’s Memorial Day parade, I caught a glimpse of 91-year-old baseball great Bob Feller, the pride of Van Meter, Iowa. He was born eight days before Armistice Day.

Feller rocked the baseball world during the summer of 1936 when he debuted for the Cleveland Indians at the tender age of 17. He won his first start as he struck out 15 St. Louis Browns. Three weeks later, he struck out 17 Philadelphia Athletics (while walking nine).

Over his career, Feller pitched three no-hitters including the only one thrown on Opening Day. He also tied the record for throwing 12 one-hitters.

The day after Pearl Harbor, Feller joined the U.S. Navy. He was the first major leaguer to volunteer for combat service. Feller served on the USS Alabama.

After the war, he returned to baseball and struck out 348 batters in 1946. He probably would have broken a lot of records had it not been for the war. Feller also helped the Tribe win the 1948 World Series (they haven’t won one since). -

The Decline and Fall of Fannie Mae

Posted by Eddy Elfenbein on June 2nd, 2010 at 12:16 pmYesterday, shares of Fannie Mae (FNM) closed at 93 cents. That’s a gigantic fall from the stock’s high of $87.

Still, it’s important to remember how successful Fannie Mae had been in the years before its undoing. In 1981, you could have picked up a share of FNM for just 53 cents (adjusted for splits). So after nearly 30 years, you’d have a 75% profit not including dividends.

Maybe that’s a small consolation but it’s something to think about. -

Joe Bank Earns 85 Cents a Share

Posted by Eddy Elfenbein on June 2nd, 2010 at 9:47 amI was wrong about JoS. A. Bank Clothiers (JOSB). I was expecting the company to beat earnings by four cents per share. Instead, they beat by 14 cents per share. I’ll try to do better next time:

Clothing maker JoS. A. Bank Clothiers Inc. said Wednesday its fiscal first-quarter net income rose 38 percent as revenue improved.

Net income for the quarter ended May 2 rose to $15.8 million, or 85 cents per share, from $11.5 million, or 62 cents per share, last year.

Revenue rose 10 percent to $178.1 million from $161.9 million from last year.

Analysts polled by Thomson Reuters, on average, predicted a profit of 71 cents per share on revenue of $175.3 million.

Revenue in stores open at least one year, a key measure of a retailer’s financial health, rose 10.4 percent.

JoS. A. Bank operates 479 stores in 42 states and the District of Columbia. -

Stocks and Hemlines

Posted by Eddy Elfenbein on June 1st, 2010 at 5:29 pm

The New York Times reports that lower hemlines are in. Devotees of the Hemline Theory believe that hemlines tend to be follow the opposite of equity prices. -

At Least It’s a Profit

Posted by Eddy Elfenbein on June 1st, 2010 at 5:07 pmThe Buy List is positive for the year…by 14 basis points!!

But we’re still over 400 points ahead of the market. -

HP to Cut 9,000 Jobs

Posted by Eddy Elfenbein on June 1st, 2010 at 2:17 pmHere’s a post which I’d call “thinking out loud” since I can’t decide where I stand. Hewlett-Packard (HPQ) announced today that it’s cutting 9,000 jobs.

HP will take a $1 billion charge for paying severance and modernizing its data centers to provide more automated services to customers, it said today in a regulatory filing. The Palo Alto, California-based company plans to replace about 6,000 of the eliminated positions with workers in different countries.

“These sets of actions will enable HP to grow better than the market,” Ann Livermore, executive vice president for enterprise business, said today on a conference call. “This is a substantial opportunity for us and something that we think is a good opportunity for our clients as well.”

The job cuts come after HP raised its 2010 forecast last month for the third time since November as results beat analysts’ estimates on a revival in business spending. Chief Executive Officer Mark Hurd has expanded into more profitable services as the recession crimped corporate budgets for equipment. He bought Electronic Data Systems Corp. for $13.2 billion in 2008, vaulting HP to No. 2 in services behind IBM.I’m a big fan of Mark Hurd. He’s done a great job in turning HPQ around after the disastrous tenure of Carly Fiorina (who will probably win California’s GOP Senate primary one week from today). Turnarounds rarely work but this one has. HPQ earnings have grown steadily over the past few years and the stock has outperformed a dismal market.

My worry is that the company might be taking on more than it can afford. I’m not thrilled with the EDS buy and I hate (HATE) the Palm buy. Still, leadership counts and I’m leaning towards trusting that Hurd knows what he’s doing. And as today’s news shows, the company hasn’t grown complacent. -

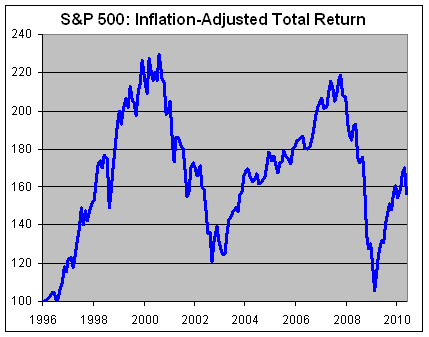

Depressing Stat of the Day

Posted by Eddy Elfenbein on June 1st, 2010 at 1:25 pmHere’s the inflation-adjusted total of the S&P 500. Even after an impressive rally, we’re still where we were more than 12 years ago.

-

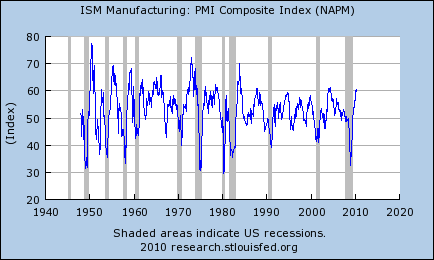

ISM = 59.7

Posted by Eddy Elfenbein on June 1st, 2010 at 11:53 amThe Institute for Supply Management’s manufacturing gauge came out today and it was 59.7. Any reading above 50 indicates an improving economy. This was slightly down from the previous report of 60.4.

As I’ve written before, the ISM is one of the best reports for telling us if the economy is in a recession or not. Historically, the tipping point has been around 44-45. Reading below that have come during recessions, and above we’re in recovery. I continue to believe the Federal Reserve will raise interest rates before most people expect. -

Debtor Nation

Posted by Eddy Elfenbein on June 1st, 2010 at 11:37 amThe NYT profiles a young woman who just graduated from NYU. She’s $97,000 in debt.

This is a scandal. It’s not merely lousy finance, but it’s also wrong to pile up debt on young people who may not realize the burden they’re placing on their future selves. Here’s what I wrote last year:Much like the housing bubble, the Higher Ed bubble is being driven by cheap, government supported credit. The problem is compounded by the fact that hugely important financial decisions are placed on the backs of 19-year-olds, many of whom simply don’t have the life experience to weigh the implications of a gigantic, 20-year debt load. Heck, at least the irresponsible mortgage borrowers during the crazy days were adults (even though many acted like infants).

One report shows that students from lower-income families need to pay 40% of their family income to enroll in a public four-year college. That’s a lot of coin to have some Marxist feminist theorist tell you about atavistic nature of late-stage capitalism. Please, you can watch the Oscars to learn that. Don’t think community colleges are a bargain, either. The average tuition is up to 49% of the poorest families’ median income from 40% in 1999-2000.

The pro-college crowd likes to repeat the claim that college grads earn $1 million more, on average, over their working lifetime. Sure, this is true, but college grads start out in a big hole. On average, they don’t even catch up to high school grads until age 33.

The debt load piled on students is scandalous. One in five students who graduated in the 1992–93 school with over $15,000 in debt defaulted on his or her loan within 10 years of graduation. We’re setting young people up for failure and ruin credit records. Thanks to the recession defaults are up 43% over the last two years. Many students go to grad school and pile on even more debt. The average law grad owes $100,000. Plus, many schools often use grad students as greatly underpaid professors in order to cut costs. Think of Lehman Brothers. Now imagine if they had a football team.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His