-

Bove Meets Hegel, Nietzsche, Rousseau and Leibniz.

Posted by Eddy Elfenbein on April 12th, 2010 at 12:46 pmCrain’s New York features the only article you’ll read today where banking analyst Dick Bove cites Hegel, Nietzsche, Rousseau and Leibniz.

Renowned banking analyst Dick Bove is calling on Bank of America to break itself up. In a Friday report, he dutifully backed up this idea with the sorts of numbers Wall Street types often use to show the bank’s different components are worth more separate than together.

Much more interestingly, he also cited BofA’s failure in living up to the teachings of 19th century German philosopher Georg Wilhelm Friedrich Hegel.

Mr. Hegel is best known for his work on dialectics, which says that an event, for instance the Protestant Reformation, triggers an forceful opposing event (the Counter-Reformation), and eventually the phenomena combine, or synthesize, to produce an improved state of being. (In fact, Catholic and Protestant Europe did learn to live together, more or less agreeably). By the way, this school of thought was an important foundation for Karl Marx.

Mr. Bove, a Rochdale Securities analyst who clearly has read up on Idealist philosophers, says that BofA fails to meet the Hegelian test.

“In a Hegelian cycle, events keep returning to the same place. However, that position is always higher and somewhat better than in the prior cycle due to the accumulated wisdom gained from prior cycles,” he wrote. “However, [BofA] shows no evidence of having learned anything from the past cycles….It gets back to the same position but at a lower point in the cycle.”

Although he didn’t cite Nietzsche’s concept of the eternal recurrence, Mr. Bove may well have had that in mind when pointed out that last year BofA’s stock was trading for the same price it fetched in 1982 and its dividend payout appears to be the same.

In a best of all possible worlds—a phrase coined by 18th century philosopher Gottfried Leibniz—Mr. Bove argues that BofA’s different businesses would be spun off as independent entities. These newly independent companies, surely stocked with the sort of Ubermenschen in management that Friedrich Nietzsche would appreciate, would lead shareholders to greater heights than BofA could. Mr. Bove pegged BofA’s break-up value at $53 a share.

An analyst for some 40 years, Mr. Bove is known for his forthright views that distinguish him from many other analysts, though sometimes his work resembles Jean-Jacques Rousseau’s Reveries of a Solitary Walker.

A BofA spokesman had no comment.Clearly, the spokesman is a Stoic.

-

Calling the Recession Over

Posted by Eddy Elfenbein on April 12th, 2010 at 11:00 amThe NYT has a good article on the issue of NBER officially declaring the recession over. I hear lots of people talking about the possibility of a double-dip. Even if that happens, I would have to view that as a separate cycle.

There is no formula for defining a recession, even though it is often casually described as two consecutive quarters of economic contraction. The committee relies on interpretation to determine the beginning or end of one.

The last time it made such a cautious statement was in December 1990, when it said that a recession had most likely begun between June and September but that it could not make a determination until the contraction was sufficiently long and deep; the committee announced four months later that the recession had started in July 1990.

It seems nearly certain that the present recession will end up lasting longer than the 16-month recessions of 1973-75 and 1981-82. They had been the longest downturns since the 43-month period from 1929 to 1933 that was the first phase of the Great Depression.

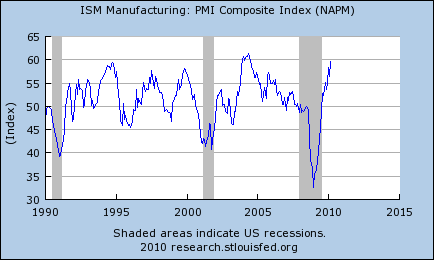

The committee, created in 1978, has assigned the start and end dates of economic contractions for every business cycle since 1854. It has long emphasized that it looks only backward, and does not make forecasts or predictions.I recently looked at the data and found that the ISM is the among the best predictors of what the committee will do. Once the ISM Composite Index crosses 44, the odds that we’re still in a recession drop dramatically. We’ve now been above that every month since June 2009.

Note that the last shaded area isn’t official. NBER has said the recession began in December 2007, but we haven’t heard on its ending just yet. -

2011 S&P 500 Earnings Estimate

Posted by Eddy Elfenbein on April 12th, 2010 at 10:41 amHoward Silverblatt, the top numbers guy at Standard & Poor’s, has pegged 2011 consensus earnings estimates for the S&P 500 at $93.55. Some have the consensus even higher. If that’s correct, then this market is still on the inexpensive side.

One major caveat is that we shouldn’t a great deal of faith in an earnings projection so far away. In March of 2009, Goldman said that the S&P 500 would earn just $40 for the entire year. Instead, it was $57. -

Upcoming Earnings Dates

Posted by Eddy Elfenbein on April 12th, 2010 at 10:28 amHere are some upcoming earnings dates and EPS estimates for stocks on the Buy List:

Intel INTC 13-Apr $0.38 Eli Lilly LLY 19-Apr $1.10 Gilead GILD 20-Apr $0.95 Johnson & Johnson JNJ 20-Apr $1.28 Stryker SYK 20-Apr $0.78 Baxter BAX 22-Apr $0.93 Reynolds American RAI 22-Apr $1.06 Aflac AFL 27-Apr $1.32 Becton Dickinson BDX 29-Apr $1.23 Fiserv FISV 29-Apr $0.97 -

Merger Monday

Posted by Eddy Elfenbein on April 12th, 2010 at 10:05 amOne of the signs of a good market is the willingness of mergers and acquisitions. This often means that there’s plenty of money out there and stocks are still cheap. Today’s merger news is the probably the catalyst that has pushed the Dow over 11,000 this morning.

For example, the California Pizza Kitchen (CPKI) said that its board has authorized a “strategic review.” That’s a fancy way of saying “the bidding starts…NOW.” Personally, I don’t quite understand many of these theme restaurants but they seem pretty popular so what do I know?

The other news is that Cerberus Capital Management LP is buyingDynCorp International (DCP) for $1.5 billion. The deal represents a 49% premium for DynCorp’s stock. Not bad.

The biggest news is the marriage proposal between Mirant (MIR) and RRI (RRI). The new company will have the hideously ugly name GenOn Energy. I’m going to factor in a 10% price discount based on the name alone. Still, I expect to see more mergers in this space. -

Bernanke Warns

Posted by Eddy Elfenbein on April 8th, 2010 at 8:10 am

Bernanke warns of U.S. debt

Ben Bernanke Warns of Deficit

Bernanke warns US economy still faces ailing housing and employment

Bernanke warns on homes, jobs

Bernanke warns Congress – Hands off the Fed!

Bernanke warns of need for monetary tightening

Bernanke Warns Against Narrowing Fed Focus

Bernanke Warns Deficits Threaten Financial Stability

Bernanke warns about creating new bubbles

Bernanke warns growth is fragile

Bernanke Warns of “Formidable Headwinds”

Freak Power Outage Puts Alan Greenspan in the Dark

Here’s more and more and more and more. -

Tax Day Is Coming

Posted by Eddy Elfenbein on April 7th, 2010 at 11:16 pmBut nearly half the country pays no Federal income tax:

The result is a tax system that exempts almost half the country from paying for programs that benefit everyone, including national defense, public safety, infrastructure and education. It is a system in which the top 10 percent of earners — households making an average of $366,400 in 2006 — paid about 73 percent of the income taxes collected by the federal government.

The bottom 40 percent, on average, make a profit from the federal income tax, meaning they get more money in tax credits than they would otherwise owe in taxes. For those people, the government sends them a payment.

“We have 50 percent of people who are getting something for nothing,” said Curtis Dubay, senior tax policy analyst at the Heritage Foundation. -

Bed Bath & Beyond Earns 86 Cents a Share

Posted by Eddy Elfenbein on April 7th, 2010 at 7:41 pmHoley Moley! Bed Bath & Beyond (BBBY) creamed even my high expectations. For their Q4, they earned 86 cents per share. In January, BBBY gave a range of 67 cents to 71 cents a share. Kinda low, no?

For the entire year (this was FY 2010 that just ended in February), BBBY earned $2.30 a share. For FY 2011, the company said it expects earnings growth of 10% to 15%. In other words, forward earnings of $2.53 to $2.64 a share. That’s much better than I was expecting. For Q1, BBBY sees earnings ranging between 44 and 48 cents per share. I have no idea what to expect now.

I had said that I was concerned that BBBY was becoming fully priced. Not anymore. This is still an excellent buy. (The earnings table is updated below.)

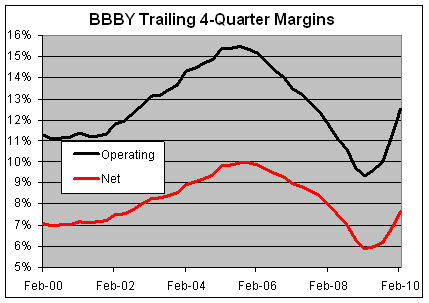

As with the broader economy, BBBY’s resurgence is a margin story. They’ve held the line on costs and no longer have to undercut anyone (RIP: Linens N Things). Here’s a look at BBBY’s trailing four-quarter operating and net margin.

That upspike is key. Retailing is a margins game. When you increase your margins, you’re King of the World, or at least the King of the Mall. Think of it this way: A margin increase of 6% to 8% turns a 10% sales increase into a 47% increase in profits. When the opposite happens, well, that’s not good.

Where BBBY is different than the broader economy is that their sales are growing. Nominal GDP growth has been pretty flat but BBBY increased its sales by 16.7% over last year.

Here’s the earnings call transcript from Seeking Alpha. Unfortunately, they never take any questions. -

Looking Ahead to Bed Bath & Beyond’s Earnings

Posted by Eddy Elfenbein on April 7th, 2010 at 12:28 pmBed Bath & Beyond (BBBY) is due to report its earnings today, probably after the close. This will be an interesting report because the last earnings report was WAY above expectations. The Street was expecting 43 cents a share and BBBY earned 58 cents a share. The stock has been in a happy mood ever since (new 52-week high on Monday, thank you very much).

With the last earnings report, BBBY said that this earnings report should range between 67 cents and 71 cents per share. That was above the Street’s estimate of 63 cents. Wall Street seems to think the company is low-balling and I agree. The Street’s consensus is for 73 cents a share. This is for the company’s fourth-quarter (December, January and February) making BBBY one of the last companies to report their results for the holiday season.

I’m expecting another beat, say 75 cents a share, but I’m not sure if the stock will respond so well this time. What I’d like to see is strong guidance going forward. I’d also like to see a full-year earnings forecast. The stock is getting pricey but a forecast of $2.50 a share for FY 2011 would help out a lot.

Here are the earnings results going back a few years:Quarter Sales Gross Profit Operating Profit Net Profit EPS $356,633 $146,214 $28,015 $17,883 $0.06 $451,715 $185,570 $53,580 $33,247 $0.12 $480,145 $196,784 $50,607 $31,707 $0.11 $569,012 $238,233 $77,138 $48,392 $0.17 $459,163 $187,293 $36,339 $23,364 $0.08 $589,381 $241,284 $70,009 $43,578 $0.15 $602,004 $246,080 $64,592 $40,665 $0.14 $746,107 $311,802 $101,898 $64,315 $0.22 $575,833 $234,959 $45,602 $30,007 $0.10 $713,636 $291,342 $84,672 $53,954 $0.18 $759,438 $311,030 $83,749 $52,964 $0.18 $879,055 $370,235 $132,077 $82,674 $0.28 $776,798 $318,362 $72,701 $46,299 $0.15 $903,044 $370,335 $119,687 $75,459 $0.25 $936,030 $386,224 $119,228 $75,112 $0.25 $1,049,292 $443,626 $168,441 $105,309 $0.35 $893,868 $367,180 $90,450 $57,508 $0.19 $1,111,445 $459,145 $155,867 $97,208 $0.32 $1,174,740 $486,987 $161,459 $100,506 $0.33 $1,297,928 $563,352 $231,567 $144,248 $0.47 $1,100,917 $456,774 $128,707 $82,049 $0.27 $1,273,960 $530,829 $189,108 $120,008 $0.39 $1,305,155 $548,152 $190,978 $121,927 $0.40 $1,467,646 $650,546 $283,621 $180,980 $0.59 $1,244,421 $520,781 $150,884 $98,903 $0.33 $1,431,182 $601,784 $217,877 $141,402 $0.47 $1,448,680 $615,363 $205,493 $134,620 $0.45 $1,685,279 $747,820 $304,917 $197,922 $0.67 $1,395,963 $590,098 $148,750 $100,431 $0.35 $1,607,239 $678,249 $219,622 $145,535 $0.51 $1,619,240 $704,073 $211,134 $142,436 $0.50 $1,994,987 $862,982 $309,895 $205,842 $0.72 $1,553,293 $646,109 $154,391 $104,647 $0.38 $1,767,716 $732,158 $211,037 $147,008 $0.55 $1,794,747 $747,866 $203,152 $138,232 $0.52 $1,933,186 $799,098 $259,442 $172,921 $0.66 $1,648,491 $656,000 $118,819 $76,777 $0.30 $1,853,892 $739,321 $187,421 $119,268 $0.46 $1,782,683 $692,857 $136,374 $87,700 $0.34 $1,923,274 $785,058 $231,282 $141,378 $0.55 $1,694,340 $666,818 $142,304 $87,172 $0.34 $1,914,909 $773,393 $222,031 $135,531 $0.52 $1,975,465 $812,412 $245,611 $151,288 $0.58 $2,244,079 $955,496 $370,741 $226,042 $0.86 -

Is This the News?

Posted by Eddy Elfenbein on April 7th, 2010 at 11:26 amHere’s NICK’s press release released a few minutes ago:

CLEARWATER, Fla., April 7, 2010 (GLOBE NEWSWIRE) — Nicholas Financial, Inc. (Nasdaq:NICK – News) today announced the opening of two (2) new branch offices located in Nashville, Tennessee and Grand Rapids, Michigan. The new offices expand Nicholas Financial’s branch network to fifty-two (52) locations. The company expects to open its 5th branch in the greater Atlanta, Georgia metro area during the current quarter, bringing the total number of Nicholas Financial branch offices to 53 in 12 states. The Company will continue to evaluate potential branch locations in both new and existing markets and intends to add 3 to 5 new branches during its 2011 fiscal year which began April 1, 2010.

Yeah…big deal. We already knew NICK is opening offices. It’s odd how a stock can be a screaming buy and yet no one will pay attention. Then suddenly, everyone has to own it.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His