-

P.J. O’Rourke on the Death of Capitalism

Posted by Eddy Elfenbein on February 11th, 2009 at 10:28 amFrom the Financial Times:

The free market is dead. It was killed by the Bolshevik Revolution, fascist dirigisme, Keynesianism, the Great Depression, the second world war economic controls, the Labour party victory of 1945, Keynesianism again, the Arab oil embargo, Anthony Giddens’s “third way” and the current financial crisis. The free market has died at least 10 times in the past century. And whenever the market expires people want to know what Adam Smith would say. It is a moment of, “Hello, God, how’s my atheism going?”

Adam Smith would be laughing too hard to say anything. Smith spotted the precise cause of our economic calamity not just before it happened but 232 years before – probably a record for going short.

“A dwelling-house, as such, contributes nothing to the revenue of its inhabitant,” Smith said in The Wealth of Nations. “If it is lett [sic] to a tenant for rent, as the house itself can produce nothing, the tenant must always pay the rent out of some other revenue.” Therefore Smith concluded that, although a house can make money for its owner if it is rented, “the revenue of the whole body of the people can never be in the smallest degree increased by it”. [281]*

Smith was familiar with rampant speculation, or “overtrading” as he politely called it. -

The Geithner Plan

Posted by Eddy Elfenbein on February 10th, 2009 at 2:01 pmTreasury Secretary Timothy F. Geithner this morning announced an aggressive and multi-faceted program that could commit $1.5 trillion or more in public and private funds to rescue banks and financial institutions and thaw frozen credit markets.

The gravity of the financial crisis confronting the Obama administration was brought into stark focus as Geitner unveiled a financial stability plan that would more closely scrutinize the risks banks are facing and offer public and private capital to those that need it; create a fund, with a starting value of $500 billion, to buy up toxic real estate loans; and commit up to $1 trillion to reopen lending markets for consumer, student, small business, auto and commercial loans.

Geithner said the administration was also working on a plan to address the nation’s housing crisis by bringing down mortgage payments and reducing interest rates. President Obama, appearing at a town hall meeting in Fort Myers, Fla., said he would personally outline the details of that plan within the next few weeks.

Geithner did not ask Congress for more funds than the roughly $350 billion that remain in the Treasury Department’s original rescue package for the financial system. He said the balance of the money for the stability plan would, for now, come from other government agencies, such as the Federal Reserve, as well as private-sector contributions.

“To get credit flowing again, to restore confidence in our markets, and restore the faith of the American people, we are fundamentally reshaping the government’s program to repair the financial system,” Geithner said. ” . . . We believe that the policy response has to be comprehensive, and forceful. There is more risk and greater cost in gradualism than in aggressive action.” -

The Black Swan Song

Posted by Eddy Elfenbein on February 9th, 2009 at 4:01 pmI’ve already devoted too much space to Nassim Taleb and his Black Swan nonsense. It’s a mystery as to why he’s considered such a visionary. But now people are claiming he’s one of the people who saw the financial crisis coming. I’ve read both of his awful books and he never made such a prediction.

Taleb is a Johnny One-Note. He can talk about how people have trouble with risk. Fine, got it. But when we go to any other topic, he can’t deal. He always goes into his Napoleon Dynamite routine where he’s brilliant and everyone else is a “freakin’ idiot!”

Notice in this clip when he’s asked what to do now and he has no clue. His answer is to fire Bernanke. Yep, that’ll solve things. Strip away the attitude and vindictiveness, and there’s nothing to him. -

SNL: Pelosi and Reid

Posted by Eddy Elfenbein on February 9th, 2009 at 3:41 pm -

Lloyd Blankfein in FT

Posted by Eddy Elfenbein on February 9th, 2009 at 10:31 amHere’s a sample of Lloyd Blankfein in today’s Financial Times:

As policymakers and regulators begin to consider the regulatory actions to be taken to address the failings, I believe it is useful to reflect on some of the lessons from this crisis.

The first is that risk management should not be entirely predicated on historical data. In the past several months, we have heard the phrase “multiple standard deviation events” more than a few times. If events that were calculated to occur once in 20 years in fact occurred much more regularly, it does not take a mathematician to figure out that risk management assumptions did not reflect the distribution of the actual outcomes. Our industry must do more to enhance and improve scenario analysis and stress testing.

Second, too many financial institutions and investors simply outsourced their risk management. Rather than undertake their own analysis, they relied on the rating agencies to do the essential work of risk analysis for them. This was true at the inception and over the period of the investment, during which time they did not heed other indicators of financial deterioration.The most provocative part is here:

The percentage of the discretionary bonus awarded in equity should increase significantly as an employee’s total compensation increases. An individual’s performance should be evaluated over time so as to avoid excessive risk-taking. To ensure this, all equity awards need to be subject to future delivery and/or deferred exercise. Senior executive officers should be required to retain most of the equity they receive at least until they retire, while equity delivery schedules should continue to apply after the individual has left the firm.

-

The Money Song

Posted by Eddy Elfenbein on February 8th, 2009 at 2:57 pm -

Mapping Bernie’s Victims

Posted by Eddy Elfenbein on February 6th, 2009 at 3:27 pmZero Hedge has some great maps showing where Bernie Madoff’s victims are. Why is it always the rich people who have all the money?

-

Just Get it Over With

Posted by Eddy Elfenbein on February 6th, 2009 at 9:59 amAnother brilliant graph from Jessica at Indexed:

-

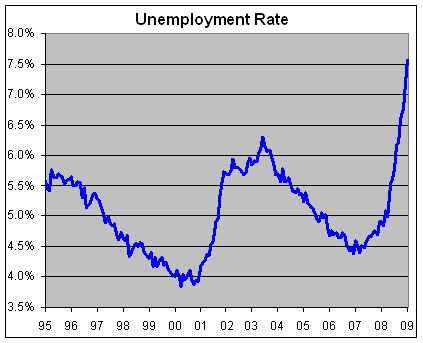

Today’s Job Report

Posted by Eddy Elfenbein on February 6th, 2009 at 8:29 amHoly crap! Unemployment jumped to 7.6% last month, the worst since September 1992. Nonfarm payrolls plunged by 598,000. The economy has lost jobs for 13 straight months. Since the recession began, the economy has lost 3.6 million jobs–half of that came in the last three months of 2008.

Here’s a look at the unemployment rate since 1995:

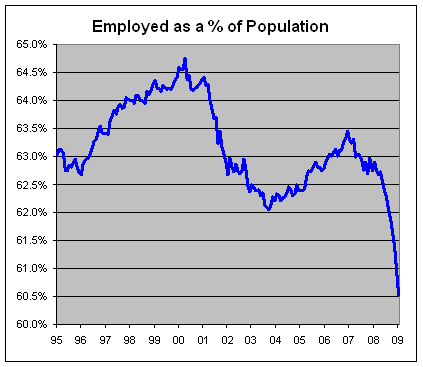

Here’s another measure of employment, the number of employed as a percent of the total population.

The traditional unemployment rate only counts folks “in the labor force” so if you’re not looking for a job, you’re not counted. Of course, people stop looking for jobs when there are no jobs so I really don’t get that one.

How’s this for a scary number. If the employed/population rate was at the level it was in April 2000, there would be nearly 10 million more jobs today. Wow.

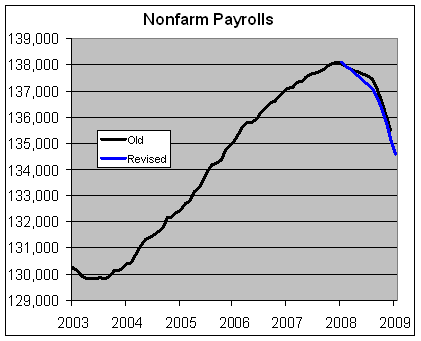

I’m not a big fan of the nonfarm payroll report because it’s constantly getting revised. Today, the government revised all the monthly numbers for 2008. Can you guess if they were revised better or worse?

Actually, the numbers for January and February were a tiny bit better, most everything else is a lot worse. -

The Action Americans Need

Posted by Eddy Elfenbein on February 5th, 2009 at 2:33 pmThe president makes his case in today’s WaPo:

This plan is more than a prescription for short-term spending — it’s a strategy for America’s long-term growth and opportunity in areas such as renewable energy, health care and education. And it’s a strategy that will be implemented with unprecedented transparency and accountability, so Americans know where their tax dollars are going and how they are being spent.

In recent days, there have been misguided criticisms of this plan that echo the failed theories that helped lead us into this crisis — the notion that tax cuts alone will solve all our problems; that we can meet our enormous tests with half-steps and piecemeal measures; that we can ignore fundamental challenges such as energy independence and the high cost of health care and still expect our economy and our country to thrive. (Has anybody said this?)

I reject these theories, and so did the American people when they went to the polls in November and voted resoundingly for change. They know that we have tried it those ways for too long. And because we have, our health-care costs still rise faster than inflation. Our dependence on foreign oil still threatens our economy and our security. Our children still study in schools that put them at a disadvantage. We’ve seen the tragic consequences when our bridges crumble and our levees fail.

Every day, our economy gets sicker — and the time for a remedy that puts Americans back to work, jump-starts our economy and invests in lasting growth is now.

Now is the time to protect health insurance for the more than 8 million Americans at risk of losing their coverage and to computerize the health-care records of every American within five years, saving billions of dollars and countless lives in the process.

Now is the time to save billions by making 2 million homes and 75 percent of federal buildings more energy-efficient, and to double our capacity to generate alternative sources of energy within three years.

Now is the time to give our children every advantage they need to compete by upgrading 10,000 schools with state-of-the-art classrooms, libraries and labs; by training our teachers in math and science; and by bringing the dream of a college education within reach for millions of Americans.

And now is the time to create the jobs that remake America for the 21st century by rebuilding aging roads, bridges and levees; designing a smart electrical grid; and connecting every corner of the country to the information superhighway.

These are the actions Americans expect us to take without delay. They’re patient enough to know that our economic recovery will be measured in years, not months. But they have no patience for the same old partisan gridlock that stands in the way of action while our economy continues to slide.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His