-

TIPs Yields

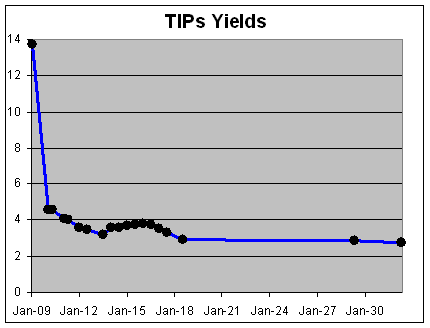

Posted by Eddy Elfenbein on November 19th, 2008 at 9:56 pmHere’s a look at the current TIPs yields-to-maturity listed by maturity date.

-

A 40-Year Look

Posted by Eddy Elfenbein on November 19th, 2008 at 4:09 pmThe S&P 500 closed at a 68-month low today. Given that the CPI report came out today, here’s an interesting stat. Adjusted for inflation, the S&P 500 has advanced just 23.9% in 40 years. Annualized, that’s 0.54%.

This means that almost the entire gain came from dividends. I should add that this is a bit of playing with numbers since 40 years ago was a cyclical high, and I hope we’re near a cyclical low.

Inflation over the last 40 years has increased by 513.5%. The S&P 500 closed today at 806.58. On November 19, 1968, the S&P 500 closed at 106.14. So the index has grown by 660%. -

Heading Towards Deflations

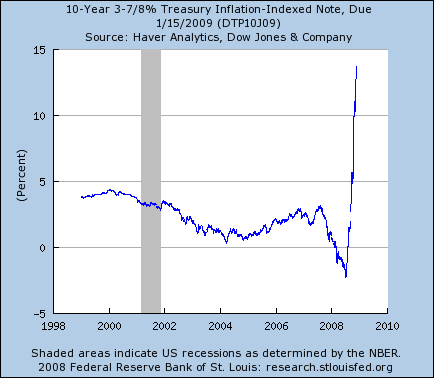

Posted by Eddy Elfenbein on November 19th, 2008 at 2:38 pmThe TIPs say deflation is coming and may stay around for a bit:

Yet, if you believe the yields on US Treasury inflation protected bonds, or Tips, we shall have a 2.2 per cent fall in prices in 2009, a 2.5 per cent decline in 2010 and only flat prices in 2011. If that turns out to be true, the real interest rate burden on even the highest-rated borrowers will be extremely hard to bear.

As a practical matter, long before we had significant “negative prints” of consumer prices, the Federal Reserve would just flat out buy Treasury bonds and monetise away with “quantitative easing”. Gold dealers would replace hedge fund managers at the art auctions, model agency parties and Congressional hearings.But there’s more to the story. John Dizard says that the market is simply becoming less efficient:

What’s really going on is another effect of the disappearance of dealer and arbitrageur capital. The dealers can’t afford to make efficient markets, given their decapitalisation, downsizing, and outright disappearance. That means anomalies sit there for weeks and months, where they would have disappeared in minutes or seconds.

Here’s another look at yield you can get for the TIP maturing in two months.

It’s currently yielding 13.73%. -

Inflation and Stocks

Posted by Eddy Elfenbein on November 19th, 2008 at 1:48 pmWith today’s report showing how steeply prices fell last month, I wanted to revisit the issue of inflation’s impact on stock prices. Let me add the important caveat that correlation doesn’t necessarily mean causation. The short answer is that inflation is bad for stocks. In fact, the only thing worse is deflation. What the market likes is inflation that’s nice, steady, predictable and low.

Going back to 1926, there have been 72 months of deflation coming in below -5%. The inflation-adjusted total return for that period is an annualized loss of -9.6%.

Here’s how it breaks out.

Inflation Rate…………Real Stock Returns (annualized)

Below -5%…………………………-9.6%

Between 0% and -5%………….20.9%

No Inflation………………………..17.1%

Between 0% and 2%…………..10.0%

Between 2% and 5%…………..14.1%

Between 5% and 7.5%………..-0.2%

Between 7.5% and 10%………-2.8%

Over 10%………………………….-11.1

Basically, when inflation is over 5% or under -5%, the market averages a real 5.5% loss. When inflation is between -5% and 5%, it average a 15% gain. -

Gene Simmons Rings the Opening Bell

Posted by Eddy Elfenbein on November 19th, 2008 at 12:48 pm -

CPI Posts Biggest Drop in 61 Years

Posted by Eddy Elfenbein on November 19th, 2008 at 11:42 amThe headline rate dropped by 1% last month which was the most since monthly record began, although the numbers in the database go back to 1913. Consumer prices dropped for an extended period beginning in the 1920s and going into the 1930s. Wall Street was expecting a fall of 0.8%.

We knew a big drop was coming thanks to the fall in oil prices, however, the biggest surprise was the core prices also fell for the first time since 1982. Wall Street was expecting a 1% rise and it got a 0.1% loss. -

More on Corporate Bond Spreads and Their Impact on Equities

Posted by Eddy Elfenbein on November 18th, 2008 at 3:23 pmMichael Stokes stokes picks up on my post from last week, and finds that “high spreads have been bullish for the stock market, except when spreads reach extreme heights (like they have at this very moment).”

-

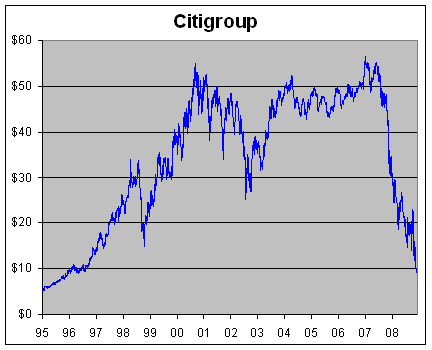

If There Was Something We Could Have Done….

Posted by Eddy Elfenbein on November 18th, 2008 at 2:09 pmCitigroup hits 13-year low:

-

Ken French on Why Commodities are a Bad Investment Idea

Posted by Eddy Elfenbein on November 18th, 2008 at 1:50 pm -

Looking at Harvard’s Endowment

Posted by Eddy Elfenbein on November 18th, 2008 at 1:39 pmDaniel Gross looks at the (mis)management of Harvard’s endowment portfolio. Or as he says, “looks like it was chosen by someone who watched a few episodes of CNBC’s Squawk Box and heard that the hot new investments were emerging markets, commodities, and private equity.”

Gross writes:The biggest position disclosed—all amounts and dollar values are as of Sept. 30—was $463 million in the iShares MSCI Emerging Market fund. As the six-month chart shows, that fund’s off nearly 60 percent from this summer and down by about one-third from the end of September. Third-largest was a $233 million position in Weyerhauser, the wood-products giant that has fallen about 40 percent since the end of September. The top 10 included $232 million in the iShares MSCI Brazil Index Fund, off about 40 percent since the end of September; about $51 million in the iPATH MSCI India Index, off about one-third since the end of September; and $158 million in the iShares FTSE/Xinhua China Index, off about 30 percent since the end of September. For good measure, top 10 holdings also included index funds that were plays on South Africa’s commodity-based economy and on the perennially emerging market of Mexico. Would it surprise you to learn that both of those investments, after fairing poorly in the third quarter, have fallen further in the fourth quarter?

I think Gross is being a bit unfair here. Harvard only has to disclose its position in publicly traded companies, and that’s “only” $2.9 billion, or less than 8% of its portfolio. For any long-term investor, which Harvard certainly is, you can safely reserve 8% of your portfolio for play money.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His