-

AFLAC Increases Its Dividend

Posted by Eddy Elfenbein on February 14th, 2006 at 8:15 pmThe market had a great turnaround today. The Dow broke 11,000. The S&P 500 broke 1,275 and closed up 1.00%.

Expeditors (EXPD) had a strange day. First, the stock opened 46 cents higher on its earnings news. It then fell to a loss of $1.57 a share. But the market changed its mind and decided that the earnings were good, and the stock then rallied to a gain of $2.22, an all-time high. Before the end of trading, that gain was halved and Expeditors finished with a still-impressive gain of $1.09. The stock is up nearly 14% for the year. I love this stock, but I’m afraid it’s getting a bit rich.

Donaldson (DCI) also plugged higher to a new all-time high, and SEI Investments (SEIC) is within striking distance of a new high.

After the bell, AFLAC (AFL) announced that it’s raising its dividend for the 24th straight year. That’s another reason to love this stock. The new quarterly dividend is 13 cents a share, an 18% increase over the old 11-cent dividend. The company will also buy back 30 million shares of stock.

Hewlett-Packard (HPQ) reports tomorrow. I hope this company can manage its business as well as it manages Wall Street. Investors are in love with this stock. Wall Street’s earnings consensus, so we’re told, is for 44 cents a share. Please. HPQ should easily report, I’ll say, 46 cents a share. The crowd wants permission to love the stock some more, however, I wouldn’t be surprised to see the stock pull back in the next few days.

I’m always skeptical of turnarounds. Not that companies don’t turn around. They do. But in HPQ’s case, it’s still HPQ. Once they stop improving their margins (hey, you lay off 15,000 people, your margins will improve, too), how fast can the company grow? Ten percent tops. I expect to see that sales rose about 5%, and that’s probably what they’ll do next quarter. This is not a great business to be in. There are only so many profiles you can read about CEO Mark Hurd. -

S&P Says Home Depot Is Worth $52

Posted by Eddy Elfenbein on February 14th, 2006 at 2:09 pmFrom Business Week:

Even though the shares have lost ground thus far in 2006, we think it’s possible to build a strong case for Home Depot. First, we think that a low unemployment rate and robust wage growth should continue to propel the U.S. economy (and, more importantly, consumer spending) at a modest clip. Second, while we’re slightly concerned with the recent rapid increases in housing prices, we believe demand will remain strong enough to avert a major problem.

Finally, we think the valuation is very compelling, with the shares trading below the broader market, despite sporting a higher growth rate and stronger balance sheet. The stock carries S&P’s highest investment ranking of 5 STARS (strong buy).

Home Depot is the world’s largest home-improvement retailer and the second-largest retailer in the U.S., in terms of sales. As of October 31, 2005, it operated 1,972 stores, including 1,913 Home Depot stores (of which 126 were in Canada and 49 in Mexico), 34 EXPO Design Centers, five Home Depot Supply stores, 11 Home Depot Landscape Supply stores, two Home Depot Floor stores, and seven Contractors’ Warehouse stores.

NUTS AND BOLTS. Home Depot stores sell a wide assortment of building materials, as well as home improvement and lawn and garden products. The company also provides installation services. Typical stores average 106,000 square feet plus 22,000 square feet of garden center and storage space, and stock 40,000 to 50,000 items, including brand name and proprietary items.

The flagship Home Depot stores serve three primary customer groups: Do-It-Yourself (DIY) customers, typically homeowners who complete their own projects and installations; Do-It-For-Me (DIFM) customers, homeowners who purchase materials and hire third parties to complete the project and/or installation; and Professional customers, consisting of professional remodelers, general contractors, repairmen, and tradesmen.

By product group, plumbing, electrical, and kitchen (29% of fiscal 2005 revenues) represents Home Depot’s largest source of revenue. Hardware and seasonal (27%), building materials, lumber, and millwork (24%) and paint, flooring, and wall coverings (20%) make up the remainder.

R.I.P. CONSUMER? We believe several factors bode well for the company in 2006, including a resilient consumer, the company’s shift in focus away from the cyclical domestic housing market, a dramatic 2005 hurricane season, and an economy on solid footing.

Some economists and investment professionals have been quick to point to the national savings rate, which has now been negative over the past seven months, as a key indicator of the impending retrenchment of the U.S. consumer. While this lack of savings is justifiably a cause for concern and could become quite problematic over the long term, we think the near-term ramifications of this statistic may not be that significant at all. Because the savings rate excludes capital gains on investments, we suspect the recent wealth that was built up as a result of the stock market in the late 1990s and real estate boom over the last five years will continue to drive spending over the coming years.

In addition, the job market remains very healthy, in our view, so we think it’s unlikely consumers will feel the need to drastically tighten their purse strings any time soon. Furthermore, while increased interest rates make refinancing a less likely option for consumers in 2006, we expect home-equity loans will continue to buoy spending. S&P predicts that consumer spending will increase 3.2% in 2006.

HOUSING VALUES. While the current status of the housing market has been well documented — and a topic of discussion at many cocktail parties — we foresee only a modest decline in new home activity in 2006. S&P economists predict an 8.8% decline in housing starts for 2006, following a 6.2% increase in 2005. We also predict that declines in real estate values may occur in certain geographic “pockets,” but that, overall, little attrition will occur. We believe it may take several years for houses to “grow” into their current values, but we don’t foresee a dramatic decline in overall prices.

Also, government spending on the reconstruction of New Orleans will be the most expensive such effort in U.S. history, with estimates ranging from $100 billion to $200 billion. We believe Home Depot will benefit substantially from this increased spending.

For Home Depot, the biggest development over the past year, in our view, has been the aggressive push by the company to expand its Home Depot Supply business in the $410 billion professional market. In July, 2005, the company acquired National Waterworks, the leading distributor of water and wastewater transmission equipment in the U.S. Then, on January 10, 2006, it agreed to purchase Hughes Supply (HUG ; $46) for $3.47 billion (including the assumption of debt), which would be its largest acquisition ever.

MOVING ABROAD. While these acquisitions may appear puzzling to many investors, as they go well beyond Home Depot’s core retail business, we believe these investments will ultimately prove to be net positives for the company. For one, both are expected to be slightly accretive to earnings. In addition, we believe they will reduce the cyclicality of Home Depot’s business, which is strongly correlated with housing turnover. We’re confident that Home Depot can properly integrate both companies.

We think international expansion is another major focus for Home Depot, and will likely be one of the future growth drivers for the company, as the domestic market approaches saturation levels. It has followed an acquisition-based strategy when first entering a new market, followed by organic growth. We expect continued organic growth to occur in Canada and Mexico, where Home Depot is the market leader, and expect the company to make an acquisition bid for a Chinese company sometime in the first half of this year.

In fact, according to an unconfirmed report in the Financial Times on Feb. 13, Home Depot is in talks to buy up to a 49% stake in Chinese retail chain Orient Home, for more than $200 million. We expect the company to work diligently on securing a foothold in China’s $50 billion retail home improvement market.

U.S. PULLBACK. At its annual investor and analyst meeting on Jan. 19, Home Depot announced that it would open between 400 to 500 new stores over the next five years (with total square footage growth of 40 million to 55 million). This is a significant deceleration from the rapid pace at which Home Depot had previously been opening stores, and indicates to us that the company believes the U.S. market is nearing saturation. We view positively this difficult decision by HD to slow new store growth, and believe it will relieve some of the pressure on same-store sales results from stores in overlapping markets.

Furthermore, we think this decision should free up the cash that Home Depot will require to grow in the Professional and international markets. While we expect Home Depot to finance the majority of its expansion plans from the significant cash flow it derives from operations, we do think it’s likely that the company will assume a greater debt load in order to accomplish all of its objectives.

We’re projecting EPS of 56 cents in the coming January quarter (results to be released on Feb. 21). Overall, we expect the company to earn $2.67 in fiscal 2006 on sales growth of approximately 11% and a 0.6% improvement in operating margins. Fueled by acquisitions, we expect fiscal 2007 sales to increase about 15%, driving EPS to $3.05.

EPS FORECAST. In our view, the quality of Home Depot’s earnings, as indicated by our proprietary Standard & Poor’s Core Earnings per share model, is high. In the absence of pension-related adjustments (the company doesn’t have a defined benefit pension plan), the main impact to earnings quality comes from the expensing of stock options.

After deducting stock-option expense, we arrive at S&P Core EPS of $1.78 for fiscal 2004 and $2.19 for fiscal 2005, representing a divergence of 5.3% and 3.1%, respectively, from GAAP-based EPS for the two fiscal years. This differential compares favorably with that of other constituent companies of the S&P 500.

We see Home Depot’s earnings quality improving further, as the company has already begun expensing options. Therefore, our estimates of option expense in fiscal 2006 and 2007 are for un-expensed options granted in previous years. Our S&P Core EPS estimate for fiscal 2006 is $2.63, indicating a 1.6% impact to our operating EPS estimate of $2.67. For fiscal 2007, we have incorporated the unexpensed stock options into our operating EPS projection of $3.05.

BALANCED BALANCE SHEET. Recent selling pressure has Home Depot shares approximately 3.5% lower since the start of 2006. We believe that a strong January-quarter and robust guidance will help fuel investor enthusiasm in the shares once again.

The shares are currently trading at 14.7 times our fiscal 2006 EPS estimate and 12.9 times our fiscal 2007 EPS estimate, below the S&P 500 and well below the stock’s historical average of 22 times. Home Depot shares have historically traded at nearly a 15% premium to the broader market due, we think, to the company’s above-average sales and earnings growth, along with its strong balance sheet. Currently, the shares trade at a 15% discount to the S&P 500.

We believe the company has one of the stronger balance sheets in our specialty-retail coverage universe, with over $1 billion in cash and manageable debt levels. In addition, its asset base is formidable, with the company owning 86% of its stores, a huge point of differentiation in the world of retail, in our opinion. Lastly, the company’s commitment of returning cash to shareholders is exemplary, we think. Home Depot has returned nearly $13 billion over the past five years in the form of dividends or share repurchases, or approximately 58% of the company’s cumulative earnings.

LEVEL BOARD. Our discounted cash-flow (DCF) valuation suggests an intrinsic value of $52 for Home Depot, about 33% above the recent price, and approximately 17 times our fiscal 2007 EPS estimate.

In general, we view Home Depot’s corporate governance positively. Several of the practices that we view positively are: the expensing of stock-option grants, the lack of a poison pill, and the fact that the nominating and compensation committees are entirely comprised of independent outside directors. Furthermore, 10 of the company’s 12 board members are independent outsiders, which we believe promotes a greater amount of objectivity and reduces conflicts of interest. However, we do view executive compensation as excessive, given the stagnant stock price over the past five years.

MICRO AND MACRO RISKS. There are several risks to our recommendation and target price, in our opinion. First and foremost, a modest decline in real estate values would likely adversely affect Home Depot. With U.S. savings rates near (or below) zero and a rather flat stock market, we believe consumers will be much less apt to spend on home-improvement projects should their net worth decline. Rising interest rates could be a catalyst to the bursting of a housing bubble, as many recent mortgages have been financed as interest-only or adjustable rate mortgages (ARMs). These rising rates would have the effect of driving up mortgage payments, thus reducing discretionary income.

Non-macro-related risks include currency movements and poor execution while entering new growth markets such as China. In addition, acquisition risks exist if Home Depot overpays for an acquisition or fails to integrate it properly and cost-effectively. -

Expensing Stock Options

Posted by Eddy Elfenbein on February 14th, 2006 at 12:44 pmYou may to check out Barron’s Online this week. The site is free-for-all for a limited time. Andrew Bary has a good article on the impact of expensing stock options, especially in the tech sector:

Tech outfits tend to be generous dispersers of stock options. At Intel and Cisco, the value of these are expected to equal about 13% of profits this year, versus 3% at Pfizer (PFE) and less than 1% at General Electric (GE).

Cisco reported “pro-forma” profits, excluding option expense, of 26 cents a share for its quarter ended Jan. 28, and of 22 cents, with option expense. Some investors and analysts, hoping for earnings that would justify a high stock price, still focus on Cisco’s pro-forma results.

Nonetheless, says David Bianco, the chief equity strategist at UBS. “There are not too many investors out there who think stock options aren’t an expense.” Option grants have been falling in recent years — Cisco, however, issued more in its latest fiscal year than in the prior one — and Bianco wonders how much further they’ll slip now that expensing is mandatory. He estimates that options will cut profits for the S&P 500 by about $2 this year, off an earnings base of around $80. That’s a hit of roughly 2.5%. The hit in tech will be an estimated 15%. -

Random Market Stat of the Day

Posted by Eddy Elfenbein on February 14th, 2006 at 11:36 amIt’s hard to overstate the impact of long-term interest rates on equity prices. As long as long-term yields head lower, the stock market does well. But when rates rise, it’s like running into the wind.

Since 1962, there have been over 2,300 weeks of trading. The yield on the 10-year Treasury bond has fallen for 1,060 of those weeks. During those weeks, the S&P 500 is up a combined 6,187%, which is about 22.5% on an annualized basis.

The 10-year yield was unchanged over 129 weeks. During that time, the S&P 500 was up just 4%, or 1.6% annualized.

And for the 1,112 weeks of rising yields, the S&P 500 was down 72.3%, or 5.8% a year. When you separate out the data like this, you can really see the impact that bond yields have on the market.

Perhaps the most important fundamental aspect of this market is that long-term interest rates have been remarkably flat for so long. For the last two-and-a-half years, long-term yields have traded in a band between 3.68% and 4.87%. Over 75% of the time, the yield has been between 4.0% and 4.5%.

In other words, stocks aren’t getting any help from bonds. -

Expeditors Earnings

Posted by Eddy Elfenbein on February 14th, 2006 at 9:50 amThis morning, Expeditors (EXPD) reported fourth-quarter earnings of 72 cents a share. However, that included a tax benefit of 19 cents a share. Discounting that, Expeditors earned 51 cents a share, two cents more than Wall Street’s estimates. Net sales increased 23%.

“This quarter has to be viewed as a fitting end to what was an outstanding year,” said Peter J. Rose, Chairman and Chief Executive Officer. “Our operating income was 27.6% of net revenue during the fourth quarter of 2004, but this expanded to an amazing 31.3% in 2005 as we were able to handle a significant increase in freight without having to add a commensurate amount of expense. This positive leverage was a result of our ongoing process and productivity initiatives. By every measure, our people did a superb job executing in what was really a very difficult environment: simply put, there was just a bunch of freight out there,” continued Rose.

“Air freight volumes were strong during the fourth quarter and ocean freight, which was a little subdued in November 2005 compared with October, came through very strong in December,” Rose said. “We think that a 39% operating income increase off of our already sizeable base is extremely indicative of just how well we executed during the busiest time of the year. We just finished recording our second straight one billion dollar quarter and this put us over the top to enjoy our first year with over one billion dollars in net revenue. More than empty talk, these are real measures of progress,” Rose concluded. -

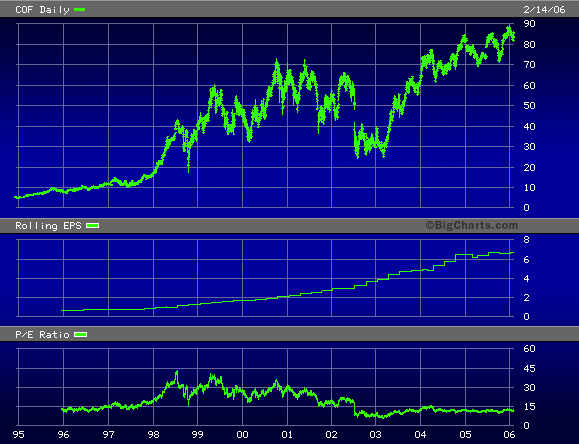

Obscenely Profitable Stock

Posted by Eddy Elfenbein on February 14th, 2006 at 1:00 amIn my continuing series, “here’s an obscenely profitable stock that I don’t own,” I bring you Capital One Financial (COF).

They’re one of the major credit card companies (David Spade, “what’s in your wallet?”). The company is massively profitable.

Capital One uses a combination of heavy mass marketing and pinpoint datamining. They know exactly who to lend to and how much. Despite their aggressive marketing, the loan portfolio has actually been fairly conservative.

I often hear people complain about junk mail from credit card companies. The companies do it for a highly sophisticated and complex reason. It works.

Capital One grew so quickly that the market assumed something had to be wrong. Four years ago, banking regulators demanded tighter controls and the stock cracked. But the company stood by its loan portfolio, and the results speak for themselves.

Here’s their earnings-per-share for the past few years: $0.77, $0.93, $1.32, $1.72, $2.24, $2.91, $3.93, $4.92, $6.21 and $6.73. Constant growth.

The company forecast earnings this year of $7.40 to $7.80 a share, which translates to growth of 10% to 16%. It also means that at today’s price, Capital One is going for 11.0 to 11.6 times this year’s earnings. That’s very cheap, and if that isn’t enough, you also get a teeny dividend.

One of my worries, however, is that the company recently completed a major merger with Hibernia bank. I always get nervous about growth-through-acquisition strategies.

-

The Market Now Expects At Least One More Rate Hike

Posted by Eddy Elfenbein on February 13th, 2006 at 4:08 pmHere’s a major change in sentiment: One month ago, the futures market indicated that there was a 56% chance that the Fed would raise rates on its March 28 meeting, and a 0% chance of a rate hike in May. Today, the futures indicate a 94% chance of a rate hike in March, and a 62% chance of another rate hike in May.

-

This Week’s Earnings

Posted by Eddy Elfenbein on February 13th, 2006 at 2:47 pmExpeditors International (EXPD) will release its fourth-quarter earnings tomorrow morning. The current consensus estimate is for 51 cents a share. Last year, Expeditors earned 39 cents a share. This is a great stock, although it’s getting a bit rich for me.

Dell (DELL) will release its fourth-quarter earnings on Thursday.

For the record, Dell originally said that its third-quarter earnings would come in at 39 to 41 cents a share, on sales of $14.1 to $14.5 billion. However, the results were 39 cents a share on sales of $13.9 billion. That was the “miss” that freaked everyone out.

For this quarter, Dell expects earnings of 40 to 42 cents a share on sales of $14.6 to $15 billion. Wall Street’s original forecast was for 42 cents on $15 billion.

If Dell earns 43 cents a share, I will never listen to another Wall Street analyst for the rest of my life. -

Is the Oil Crises Over?

Posted by Eddy Elfenbein on February 13th, 2006 at 1:52 pmYes, according to Matthew Lynn at Bloomberg:

Forget that order for a funny- looking electric car. Take the solar panels off the roof. Don’t worry about hoarding tinned food for the long economic slump that is about to engulf the world.

Why? Because the oil crisis we were all concerned about less than a year ago is quietly going away.

The laws of supply and demand are starting to restore market calm. They suggest that although oil isn’t about to get really cheap, talk of $100 a barrel can now be put to rest.

That will give an extra leg to economic growth and stop central bankers from fretting about inflation.

“The fundamentals are starting to quietly reassert themselves,” Simon Hayley, senior international economist at Capital Economics Ltd. in London, said in a telephone interview.Oil is down to $61.15 a barrel today.

-

Venture Capitalist Turns Romance Novelist

Posted by Eddy Elfenbein on February 13th, 2006 at 1:33 pmTom Perkins, one of the legendary venture capitalists of Silicon Valley, has a new book out. But it’s not what you think.

The new book, Sex and the Single Zillionaire, is actually a romance novel and it sounds like the kind of thing Danielle Steel would write. Of course, that’s hardly a coincidence considering that Ms. Steel is not only his editor, but his ex-wife.

Yah Zhao at the Harvard Crimson outlines the plot:The protagonist, Steven Hudson, is a powerful N.Y. investment banker. Like Perkins, Steven receives a letter asking him to be the star in a reality television show called “Trophy Bride” where young, female 20-somethings compete to marry a “zillionaire.” After repeated assertions about the absurdity of the offer, Steven ends up agreeing to do the show—partially because he is lonely after his wife’s passing and partially because he falls in love with the producer of the show, Jessie Jones.

After 280 pages of trials and tribulations—including Steven being conned by a girl pretending to be on the U.S. Olympic ski team, being pursued by a nymphomaniac, and pacifying his extremely conservative colleagues who were outraged by his “sex frolic”—the obligatory happy ending is duly set down.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His