-

How Disney+ Became a Streaming Service Heavyweight

Posted by Eddy Elfenbein on February 10th, 2021 at 3:45 pm -

A Note About Twitter

Posted by Eddy Elfenbein on February 10th, 2021 at 1:07 pmI have a Twitter account and I use it a lot. I’m lucky enough to have gained a decent-sized following.

Thanks to Twitter, I’ve been able to connect with countless people who are smart, kind, funny and passionate about investing.

As much as I enjoy Twitter, I don’t take it that seriously. I say this because there’s a small minority of people, perhaps less than 1%, who take Twitter seriously. Very seriously.

That’s not me. I have to confess that I’m a person who is incapable of being offended. Whatever that gene is, I don’t have it. Due to this shortcoming, I occasionally, and always inadvertently, upset people on Twitter.

I find this frustrating. More often than not, I’m baffled by how some tweet could have offended anyone. It’s usually a joke that misfires. Or someone gets angry about the political slant of the tweet.

In these cases, the intent is entirely lacking on my part. I’m amazed at the political angle that some people can unearth in a seemingly benign tweet. To us un-offendables, it’s like people speaking a foreign language that’s somewhat similar to English but you can’t quite follow the whole thing.

If you think I’m exaggerating, this is from the day of the Capital Gazette shooting.

So they deserved to die, then?

— Shizuka Kobayashi (@ShizukaKobayash) June 28, 2018

I have other examples.

Still, I’m not here to upset people. Nor am I a professional comedian. As I see it, my principal goal is to share market news and observations. I’ll add some corny jokes well. That’s it. If someone gets upset by a Tweet, I’ll usually delete it.

Twitter can be a lot of fun. But if you follow me, always bear in mind that it’s not that serious.

-

10-Year Breakevens Highest Since 2014

Posted by Eddy Elfenbein on February 10th, 2021 at 12:42 pmWith the government spending so much money, I’ve been concerned about a resurgence of inflation. So far, there hasn’t been much evidence of higher prices. Still, I’m not the only one who’s concerned.

I like to follow the “breakeven” rates. This is basically the market’s view of expected inflation. It’s the difference between, in this case, the 10-year Treasury yield and the 10-year Inflation Protected bond. The Federal Reserve often discusses the breakeven rates since the central bank doesn’t want to see expectations get out of control.

During the worst part of the market crash last year, the 10-year breakeven rate fell to 0.5%. That’s very low. Since then, it’s rallied much higher. The breakeven rate has recently gotten as high as 2.22%. That’s the highest in six-and-a-half years (see below).

This morning, the government said that inflation rose by 0.3% in January which matched expectations. The core rate was unchanged.

-

Morning News: February 10, 2021

Posted by Eddy Elfenbein on February 10th, 2021 at 7:00 amThe Power Balance Is Shifting in London’s Commercial Real Estate

In Canada, Americans Are Missed, With Limits

Biden’s Next Economic Challenge: Getting Manufacturing Jobs Back

U.S. Chamber of Commerce Names Its First New Leader in 24 Years

A U.S. Housing Crisis Could Be Looming on the Horizon

Microsoft CEO Says Big Tech Needs Clearer Laws on Online Speech

Elon Musk Wants Clean Power. But Tesla’s Carrying Bitcoin’s Dirty Baggage

King of Supply-Chain Finance Expands, and Controversy Follows

Chase Coleman Leads $23 Billion Payday for 15 Hedge Fund Earners

Toyota Powers Ahead of Rivals With Much Brighter Outlook

Coca-Cola Earnings Top Estimates as Cost Cutting Offsets Pandemic’s Blow to Sales

Aunt Jemima No More; Pancake Brand Renamed Pearl Milling Company

Nick Maggiulli: The Test of Time: Art as an Investment

Ben Carlson: The Investment Strategy That Makes Your Life Easier

Joshua Brown: Explorer & How SPAC Issuers Earn 1,000% Returns

Michael Batnick: So Much Time and So Little To Do & An Inside Joke for the Super-Rich

Be sure to follow me on Twitter.

-

Fiserv Earned $1.30 per Share

Posted by Eddy Elfenbein on February 9th, 2021 at 4:30 pmAfter the closing bell, Fiserv (FISV) reported Q4 earnings of $1.30 per share. This was the company’s 35th year in a row of double-digit earnings growth. For 2020, Fiserv earned $4.42 per share compared with $3.96 per share for 2019, so earnings growth came in at 11.6%. Previously, the company said it expected to see 2020 earnings growth of 11%.

For 2021, Fiserv expects revenue growth of 8% to 12%. For earnings, Fiserv sees earnings of $5.30 to $5.50 per share. That’s growth of 20% to 24%. Wall Street had been expecting $5.39 per share. I think it’s very likely we’ll see year #36 in a row.

For 2020, operating cash flow rose by 48% to $4.15 billion. Free cash flow increased 7% to $1.05 billion in the quarter and 11% to $3.65 billion for the full year.

More good news. The board approved a new 60-million-share buyback authorization. During Q4, Fiserv bought back 1.8 million shares for $200 million. For the whole year, Fiserv bought back 16.1 million shares for $1.64 billion.

-

Morning News: February 9, 2021

Posted by Eddy Elfenbein on February 9th, 2021 at 7:05 amU.S. Maritime Regulator Urges Freight ‘Silos’ to Unite in Crisis

The Clash of Liberal Wonks That Could Shape the Economy, Explained

The Gig Economy Dipped Again in the Fall. But How Bad Was It?

Crisis Spurs Congress Toward Big Measures to Lift Families From Poverty

Bitcoin Powers Towards $50K as Tesla Takes It Mainstream

Reddit’s Valuation Doubles to $6 Billion After New $250 Million Funding

Lost In the ‘Gamestonks’ Mania – What is GameStop Actually Worth?

JP Morgan’s Board Rejects Switch to Stakeholder-Focused Entity

Apple Is the $2.3 Trillion Fortress That Tim Cook Built

Elon Musk’s Love-In With China May Be Over As Regulators Go After Tesla

Amazon to Buy Half of the Energy Produced by Huge Offshore Wind Farm in the Netherlands

Ben Carlson: The Catch-22 of Selling Your House Right Now

Howard Lindzon: From Tiny Bubbles To Frothy McBubbles

Joshua Brown: Shorts and Longs Are NOT Enemies!, Repeat After Me: That Sounds Stupid, I’m Buying Some Just In Case, Reddit App Installs Explode, Up 127% Year Over Year & The Plumbing

Be sure to follow me on Twitter.

-

Low Qual Is Leading the Charge

Posted by Eddy Elfenbein on February 8th, 2021 at 11:53 amThe stock market was up every day last week, and it’s up again today. If the market holds, this will be another all-time high close.

Friday’s jobs report showed that the U.S. economy created 49,000 net new jobs last month. The unemployment rate fell to 6.3%. Very roughly speaking, I’d say we’re about 10 million jobs away from something resembling full employment.

On our Buy List, Trex (TREX), Abbott Labs (ABT) and Disney (DIS) are all at new highs, and Ansys (ANSS) is very close. There are no Buy List earnings reports today. Our next one will come tomorrow when Fiserv (FISV) reports after the close.

One of the factors that is used to dissect the market is “quality.” Analysts like to see if high-quality stocks are leading the charge, or if they’re being left behind. That’s assumed to be a good indicator of what investors are thinking.

At the outbreak of the coronavirus, investors flocked to high-quality names. That makes sense. But since May, high quality has lagged. Actually, it’s lagged pretty badly.

Here’s a chart of Fidelity’s Quality ETF divided by the S&P 500.

-

Morning News: February 8, 2021

Posted by Eddy Elfenbein on February 8th, 2021 at 7:05 amWhat Recovery? Clothes Retailers Cut Orders While Factories Fight to Survive

Biden Appointments Signal a Trade Approach That Hews to the Left

Treasury Long Bond Reaches 2% Milestone as Global Yields Awaken

Without A Big Aid Bill Like Biden’s, Jobs Will Be Slow to Rebound, Yellen Warns

Tightening Oil Supplies Inject New Momentum Into Price Rally

Dogecoin Smokes Its All-Time High After Snoop Dogg Becomes Snoop DOGE

Wall Street’s Most Reviled Investors Worry About Their Fate & Short-Sellers Fear for the Future

Renaissance Clients Pull Out After Firm’s Rotten Run of Results

SoftBank’s Son Hails ‘Golden Eggs’ as Vision Fund Rallies

Apple Supplier Dialog Semiconductor Snapped Up by Japanese Tech Giant for $6 Billion

Dating App Bumble Boosts IPO Fundraising Target to $1.8 Billion

Big Publishing Pushes Out Trump’s Last Fan

Ben Carlson: Some Friendly Reminders About Day Trading & Will Robinhood Become the Facebook of Finance?

Michael Batnick: Animal Spirits: Commission-Free Insurance

Howard Lindzon: Sunday Sentiment….Access To Markets Not Democratization

Be sure to follow me on Twitter.

-

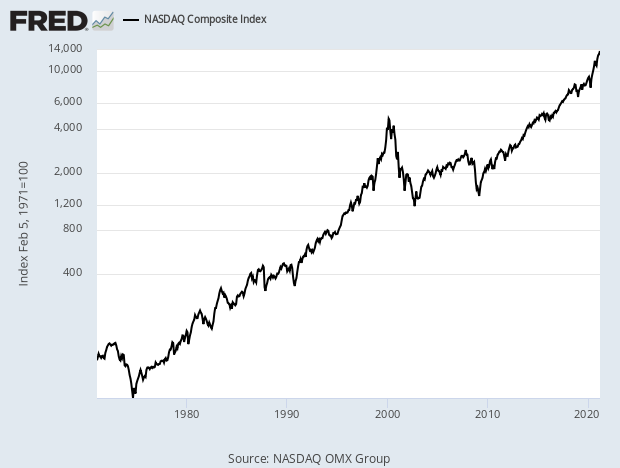

Happy 50th Birthday to the Nasdaq Composite

Posted by Eddy Elfenbein on February 5th, 2021 at 10:22 amToday is the 50th birthday for the Nasdaq Composite index.

The index started at 100 based on the closing prices of February 5, 1971. That was also a Friday. The first day of trading was Monday, February 8. The index closed that day at 100.84.

However, the start wasn’t that great. By October 3, 1974, the Nasdaq had fallen down to 54.87.

The index crashed 77.93% during a two-and-a-half year stretch from March 2000 to October 2003.

The Nasdaq closed Thursday at 13,777.74. Not including dividends, that’s an annualized gain of 10.35% per year.

-

CWS Market Review – February 5, 2021

Posted by Eddy Elfenbein on February 5th, 2021 at 7:08 am”Investment is most successful when it is most businesslike. – Ben Graham”

So far this earning season, we’re a perfect 12 for 12. All 12 of our Buy List stocks that have reported earnings so far have beaten Wall Street’s consensus. I probably shouldn’t jinx it, since we still have ten more reports to go.

It looks like Wall Street has survived the meme-stock rebellion. At least for now. Shares of GameStop crashed 83.5% this week, and there’s still one more trading day left. GameStop’s plunge this week works out to an average loss of 1% for every eight minutes and 41 seconds of market time. That’s pretty painful.

Meanwhile, the S&P 500 closed at another all-time high on Thursday. Since October 30, the S&P 500 has rallied 18.4%. Notice how we bounced off the 50-day moving average (blue line).

(Side note: Six months ago, the now-famous “Roaring Kitty” cc’d several Wall Street big shots in an attempt to draw attention to his bullish videos on GameStop. Amongst those big shots was your humble editor. At the time, GameStop was going for about $4 per share. I didn’t learn about the tweet until this week.)

In this week’s CWS Market Review, I’ll cover all of our Buy List reports. We also had two dividend hikes this week, plus Sherwin-Williams announced a 3-for-1 stock split. I’ll also preview four more earnings reports coming our way next week, including Disney. There’s a lot to get to, so let’s jump right in.

Six Buy List Earnings Reports

Here’s our updated Earnings Calendar:

Stock Ticker Date Estimate Result Silgan SLGN 26-Jan $0.53 $0.60 Abbott Labs ABT 27-Jan $1.35 $1.45 Stryker SYK 27-Jan $2.55 $2.81 Danaher DHR 28-Jan $1.87 $2.08 Sherwin-Williams SHW 28-Jan $4.85 $5.09 Church & Dwight CHD 29-Jan $0.52 $0.53 Thermo Fisher TMO 1-Feb $6.56 $7.09 Broadridge Financial Sol BR 2-Feb $0.70 $0.73 AFLAC AFL 3-Feb $1.05 $1.07 Check Point Software CHKP 3-Feb $2.11 $2.17 Hershey HSY 4-Feb $1.43 $1.49 Intercontinental Exchange ICE 4-Feb $1.08 $1.13 Fiserv FISV 9-Feb $1.29 Cerner CERN 10-Feb $0.78 Disney DIS 11-Feb -$0.42 Moody’s MCO 12-Feb $1.96 Zoetis ZTS 16-Feb $0.86 Stepan SCL 18-Feb $1.08 Trex TREX 22-Feb $0.36 Ansys ANSS 24-Feb $2.54 Middleby MIDD TBA $1.40 Miller Industries MLR TBA n/a Last Friday, Church & Dwight (CHD) reported Q4 earnings of 53 cents per share. That beat the company’s own range of 50 to 52 cents per share. You really can’t go wrong with condoms and baking soda.

For 2020, C&D made $2.83 per share. That’s an increase of 14.6% over 2019. The company had been expecting growth of 13%. Full-year net sales grew 12.3% to $4.9 billion. Cash from operating activities increased 14.6% to $990.3 million.

The best news is that Church & Dwight increased its quarterly dividend by 5.2% to 25.25 cents per share. This makes the annual payout $1.01 per share. This is the 25th consecutive year in which Church & Dwight has increased its dividend. I love seeing long streaks like this.

For 2021, C&D expects earnings of $3.00 to $3.06 per share. That’s growth of 6% to 8%. Wall Street had been expecting $3.05 per share.

For Q1, the company sees sales growth of 3% and organic sales growth of 2%. For EPS, Church & Dwight expects 80 cents per share. The Street had been expecting 86 cents per share.

That’s not great, and the shares pulled back after the earnings report, but I’m not too concerned. For now, I’m dropping our Buy Below on Church & Dwight to $90 per share.

On Monday, Thermo Fisher Scientific (TMO) reported Q4 earnings of $7.09 per share. This was a very good quarter for TMO. Wall Street had been expecting $6.56 per share. Q4 revenue grew by 54% to $10.55 billion. Full-year revenue increased 26% to $32.22 billion, and full-year EPS increased 58% to $19.55.

On the earnings call, Thermo said it expects 2021 earnings of $21.62 per share and revenue of $35.1 billion. I like that forecast. Wall Street had been expecting $20.74 per share on revenue of $33.7 billion. I’m lifting our Buy Below price on Thermo to $500 per share.

On Tuesday, Broadridge Financial Solutions (BR) reported fiscal Q2 earnings of 73 cents per share. That topped Wall Street’s estimates of 70 cents per share.

CEO Tim Gokey said that Broadridge now expects sales and earnings growth to be at the “higher end” of their full-year guidance. The current guidance is for revenue growth of 3% to 6% and earnings growth of 6% to 10%.

“Broadridge delivered 7% recurring-revenue growth and 38% adjusted-EPS growth in the second quarter.

“We are executing well on our targeted-growth plans across governance, capital markets, and wealth and investment management. As we enter our seasonally more significant second half of the year, we will continue to invest to support our long-term growth strategies,” Mr. Gokey added.

“Our fiscal-2021 outlook puts us squarely on track to achieve the three-year growth objectives we presented at our investor day two months ago, including 7-9% recurring revenue and 8-12% adjusted-EPS growth,” Mr. Gokey concluded.

Let’s do a little math. Last fiscal year (ending in June), Broadridge made $5.03 per share. So that higher end of guidance roughly translates to earnings this fiscal year of $5.43 to $5.53 per share. For the first six months of this year, the company has made $1.70 per share.

This isn’t an outstanding report like BR’s last one, but it’s a good one. Broadridge remains a buy up to $150 per share.

There’s always a dud each earning season, and this time, it looks to be Check Point Software’s (CHKP) turn. On Wednesday, the cyber-security company reported earnings of $2.17 per share. That beat Wall Street’s consensus by six cents per share.

For the same quarter one year before, Check Point made $2.02 per share. Sales rose 4% to $564 million. Wall Street had been expecting revenue of $555.4 million. During the quarter, Check Point bought back 2.7 million shares for $323 million.

So what upset traders? The answer is Check Point’s guidance. For Q1, Check Point sees earnings ranging between $1.45 and $1.55 per share. Consensus was $1.51 per share. For the whole year, Check Point expects $6.45 to $6.85 per share. Consensus was $6.92 per share.

Shares of CHKP plunged 10.5% on Wednesday. The stock is still higher than it was two months ago, but that kind of move hurts. Personally, I think traders overdid it. At the current price, Check Point is going for about 18 times this year’s estimate. Let’s also remember that Check Point might exceed its own guidance. After all, the company has topped expectations for the last 16 quarters in a row. (It could be longer, but that’s all the data I have.)

Look for a rebound here. Check Point remains a buy up to $133 per share.

In last week’s issue, I said I expected an earnings beat from AFLAC (AFL), and we got one, although it was close. For Q4, the duck stock reported operating earnings of $1.07 per share. That beat Wall Street’s forecast of $1.05 per share. The yen/dollar exchange rate pinged earnings by two cents per share.

For the year, AFLAC made $4.96 per share. That’s up from $4.44 in 2019. For the full-year, forex added four cents per share to the bottom line. During the quarter, AFLAC bought back 11.8 million shares of AFL for $500 million.

As always, the details are solid with AFLAC. At the end of the quarter, total shareholder equity was $48.46 per share. The annualized ROE on shareholders’ equity in Q4 was 11.5% and 15.3% for the full year.

My take: AFLAC had a very tough year in 2020. Given what they had to deal with, the company performed admirably. The recent 18% dividend hike reflects that. AFLAC remains a buy up to $50 per share.

On Thursday, Hershey (HSY) said it made $1.49 per share, which beat estimates by six cents per share.

Sales grew 5.7% to $2.19 billion, beating the FactSet consensus of $2.11 billion, as volume and prices increased. North America sales rose 8.9% to $1.97 billion, beating the FactSet consensus of $1.90 billion, while international and other revenue dropped 17.3% to $211.3 million to miss expectations of $219.7 million.

For 2021, Hershey expects EPS growth of 6% to 8%. Last year, the confectioner made $6.29 per share, so this year’s range is about $6.67 to $6.80 per share. That’s quite good. Wall Street had been expecting $6.58 per share. Hershey is a buy up to $160 per share.

Finally, Intercontinental Exchange (ICE) earned $1.13 per share, which beat estimates of $1.08 per share.

This is ICE’s 15th year in a row of record revenues. For the year, ICE earned $4.51 per share. ICE’s adjusted operating margin was 59%. This is why I love near-monopolies.

ICE is also raising its quarterly dividend by 10% to 33 cents per share. The first quarter dividend is payable on March 31 to stockholders of record as of March 17. Intercontinental Exchange is a buy up to $123 per share.

Four Buy List Earnings Reports Next Week

We have four more Buy List earnings reports scheduled for next week. Let’s start with Fiserv (FISV), which is due to report on Tuesday. I’m looking forward to this report because it should confirm Fiserv’s 35th year in a row of double-digit earnings growth. That’s a remarkable streak.

Fiserv expects to see its earnings rise by 11% over 2019. Fiserv earned $4 per share in 2019, so an 11% earnings increase translates to full-year earnings of $4.44 per share.

For the first nine months of this year, the company made $3.12 per share. That works out to Q4 earnings of $1.32 per share.

On Tuesday, it’s Cerner’s (CERN) turn. This company is usually quite accurate with its forecasts, so that takes some of the excitement out of earnings time. That’s fine by me. For Q4, Cerner expects revenue between $1.365 billion and $1.415 billion and earnings between 76 and 80 cents per share. That implies full-year earnings of $2.82 to $2.86 per share. Cerner is delivering as expected.

Disney (DIS) is due to report its fiscal Q1 on Thursday. This should be an interesting one. For the third quarter in a row, the Mouse House is expecting to report a loss, but for the quarter ending in June, Disney actually made a small profit. Disney has been hurt by the lockdowns, but it’s held up much better than Wall Street had expected.

Six months ago, Disney creamed estimates by 72 cents per share. Then, three months ago, Disney beat by 50 cents per share. This time around, the Street is looking for a loss of 42 cents per share. That forecast has crept higher in the past few weeks.

In October, I told you to expect a big earnings beat from Moody’s (MCO), but even I didn’t think it was going to be that much. For Q3, the ratings agency earned $2.69 per share which creamed estimates by 59 cents per share. Moody’s Analytics, which is a key business for them, saw a revenue increase of 7% to $531 million.

At the time, Moody’s raised its full-year guidance range from $8.80 to $9.20 per share to $9.95 to $10.15 per share. For the first three quarters, Moody’s has made $8.24 per share. That implies Q4 earnings of $1.71 to $1.91 per share.

Sherwin-Williams to Split 3-for-1

On Wednesday, Sherwin-Williams (SHW) said it will split its stock three for one. This means shareholders will get two more shares for each share they own. However, the share price will fall by two thirds.

The split will happen on April 1. Last week, the paint stock reported very good earnings. For Q1, Sherwin expects that “sales will increase high single digits.” For 2021, the company sees earnings ranging between $26.40 to $27.20 per share.

When the split happens, our $720 Buy Below price will adjust to $240 per share.

That’s all for now. The January jobs report is due out later today. The consensus is that the U.S. economy created 50,000 net new jobs in January and that the unemployment rate is 6.7%. Next week’s news will probably be dominated by earnings. We’ll also get the consumer inflation report on Wednesday. I doubt we will see much inflation, but there seems to be an emerging consensus that inflation will be gaining steam over the next few years. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His