“We don’t have any basis, or any evidence, for calling this a hot labor market.”

– Jerome Powell

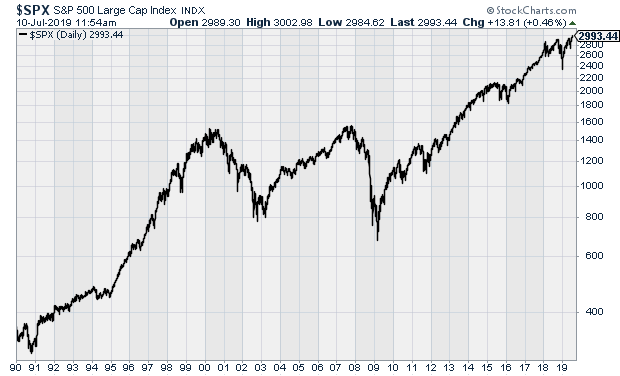

Future historians will note that on Wednesday, July 10 at 9:50 a.m. ET, the S&P 500, for the first time ever, broke through 3,000.

Sure, it fell back again, but it really did happen. Then on Thursday, the Dow broke above 27,000.

What was the cause of this latest rally? That came in the form of Fed Chairman Jay Powell. The Fed head spoke before Congress this week and strongly hinted that the Fed was ready to lower interest rates. How many times is still not known, but Wall Street is pleased with the news. Since June 3, the S&P 500 is up over 9%.

In this week’s CWS Market Review, I’ll go over the latest from the Fed. Also, earnings season is upon us. We have our first Buy List earnings reports coming next week. I’ll preview what’s in store.

The Fed Signals It’s Ready to Cut Rates

Last Friday, shortly after I sent you last week’s issue, the government reported that the U.S. economy created 224,000 net new jobs in June. That was an impressive figure, and it was higher than Wall Street had been expecting. The unemployment rate rose a tick to 3.7%.

On Thursday, we got a CPI report that was a bit higher than expected. The government said that inflation rose 0.1% last month, while the “core rate,” which ignores food and energy, rose by 0.3%. That was the highest jump for core inflation since early 2018.

Also on Thursday, the jobless-claims report fell to 209,000. That’s the lowest in three months.

Taking these three news items together, it appears that the labor market is doing well, and there may be cost pressures building in the economy.

This seems to have had zero effect on the Federal Reserve and its plans for interest rates. This week was the Humphrey-Hawkins testimony. This is the law that requires that the Chairman of the Federal Reserve to go to Capitol Hill twice a year to testify before the House and Senate Committees.

(Years ago, I used to go to these. Once I got the coveted the seat directly behind Bernanke.)

The chairman was asked directly if he thought the labor market was running hot. He said, “We don’t have any basis, or any evidence, for calling this a hot labor market.” That’s unusually frank language for a Fed chair. They’re trained to speak in Obfuscation.

Also this week, we got the minutes from the Fed’s June meeting. They seemed to indicate a growing consensus at the Fed for an interest-rate cut.

Consequently, on Thursday, the Dow, Nasdaq and S&P 500 all closed at record highs. The unemployment rate is near a 50-year low, and the Fed is ready to rescue us. I have to admit that I don’t see the need for a rate cut right now. I thought the December hike was a mistake, so I suppose I can see one rate cut. Wall Street, however, sees a string of rate cuts coming our way. According to the futures markets, there’s a 100% chance of a cut at the end of this month. It’s hard to get more certain than that.

That’s not all. Traders think there’s a 70% chance of another cut in September, plus a third rate cut in December. That could be right. Chairman Powell said, “we hear lots of reports of companies having a hard time finding qualified labor; nonetheless, we don’t really see wages responding.”

One concern is that if the Fed doesn’t cut, then it would be out of alignment with monetary policy in Europe. The European Central Bank may start a new round of bond buying. In fact, the ECB may soon cut interest rates again, which are already negative. Inflation expectations have plunged in Europe.

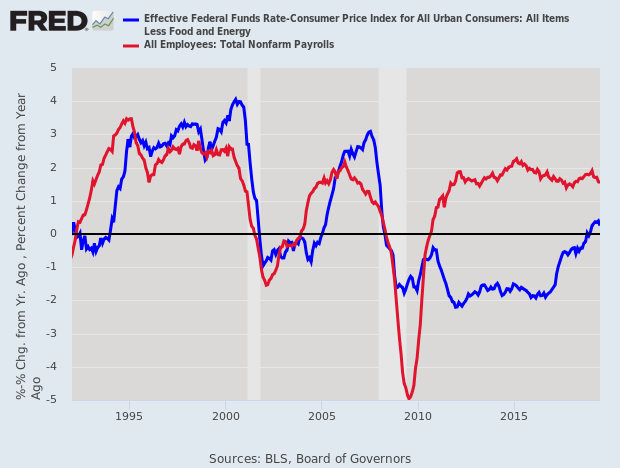

Here’s an interesting chart. The blue line is the real Fed funds rate based on core inflation. The red line is the year-over-year growth in nonfarm payrolls. These two lines had a fairly moderate correlation that was broken apart by the last recession.

Can the Fed cut rates when the market is near an all-time high? Ryan Detrick ran the numbers and found that since 1980, the Fed has cut rates 17 times when the S&P 500 was within 2% of a new high. One year later, the market was higher all 17 times.

One of the good aspects of our style of investing is that we don’t need to predict Fed policy. While I find the Fed’s plans to be stronger than necessary, they don’t alter our basic approach. The important takeaways are that lower short-term rates are mostly bullish for the stock market. Lower short rates usually allow for higher equity valuations. Indeed, that probably explains why the market jumped to new highs this week.

There are also important internal changes to the market. When short-term rates fall, high-dividend stocks are more appealing. We can certainly see that effect in our portfolio. Conversely, financial stocks tend to lag as rates fall. (Please note that I’m speaking in very general terms.)

This week has been a good one for our Buy List. We’re up more than 22% this year. But second-quarter earnings season is about to start. Let’s take a closer look.

Second-Quarter Earnings Preview

There’s hasn’t been a lot of news about our stocks recently. Mostly, it’s been a broad rally, and several of our stocks have made new 52-week highs. On Thursday, both Cerner (CERN) and Moody’s (MCO) made new highs. Both stocks are up over 40% for us this year and have a chance of dethroning FactSet (FDS) as our top performer this year.

Here’s a list of our stocks, the reporting date and Wall Street’s consensus. I have to include my typical warning that these dates and numbers sometimes change. Some companies are, shall we say, not overly forthcoming when it comes to shareholder communication.

| Company |

Ticker |

Date |

Estimate |

| Eagle Bancorp |

EGBN |

17-Jul |

$1.12 |

| Danaher |

DHR |

18-Jul |

$1.16 |

| RPM International |

RPM |

22-Jul |

$1.14 |

| Sherwin-Williams |

SHW |

23-Jul |

$6.40 |

| Torchmark |

TMK |

24-Jul |

$1.65 |

| Check Point Software |

CHKP |

24-Jul |

$1.37 |

| Cerner |

CERN |

24-Jul |

$0.64 |

| Stryker |

SYK |

25-Jul |

$1.94 |

| AFLAC |

AFL |

25-Jul |

$1.07 |

| Hershey |

HSY |

25-Jul |

$1.17 |

| Raytheon |

RTN |

25-Jul |

$2.64 |

| Moody’s |

MCO |

31-Jul |

$2.00 |

| Church & Dwight |

CHD |

31-Jul |

$0.52 |

| Cognizant Technology Solutions |

CTSH |

31-Jul |

$0.92 |

| Intercontinental Exchange |

ICE |

1-Aug |

$0.93 |

| Disney |

DIS |

6-Aug |

$1.76 |

| Becton, Dickinson |

BDX |

6-Aug |

$3.07 |

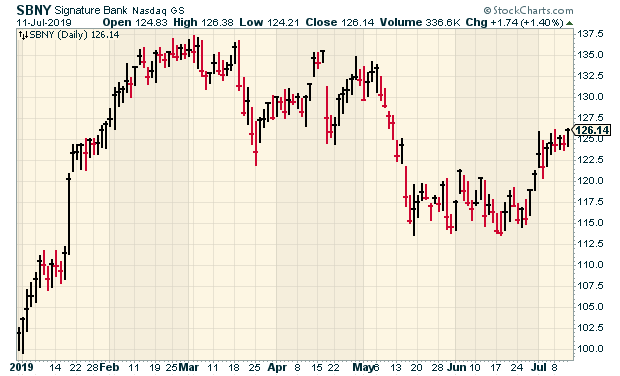

| Signature Bank |

SBNY |

TBA |

$2.71 |

| Fiserv |

FISV |

TBA |

$0.81 |

| Continental Building Products |

CBPX |

TBA |

$0.52 |

| Broadridge Financial |

BR |

TBA |

$1.71 |

I want to cover two earnings reports scheduled for next week.

Eagle Bancorp (EGBN) is due to report on Wednesday, July 17. Three months ago, the bank missed earnings by one penny per share. I’m not too concerned by that.

Eagle is currently going through a transition after the former CEO, Ron Paul, announced his retirement. Susan G. Riel had been the interim President and CEO, and now she’s taken those positions permanently.

About the Q1 results, Riel said, “The Company’s assets ended the quarter at $8.39 billion, representing 9% growth over the first quarter of 2018. First-quarter 2019 earnings resulted in a return on average assets of 1.62% (1.85% excluding nonrecurring costs as defined above) and a return-on-average tangible common equity of 13.38% (15.26% excluding nonrecurring costs as defined above).”

For Q2, Wall Street expects earnings of $1.12 per share. EGBN is currently going for just over 11 times next year’s earnings estimate.

Danaher (DHR) is scheduled to report its earnings the following day, on July 18. Three months ago, Danaher reported Q1 earnings of $1.07 per share. That was three cents more than estimates.

Danaher has been quite busy this year. The company is buying GE’s biopharma business for $21.4 billion. Danaher said it expects Q2 earnings to range between $1.13 and $1.16 per share. The company lowered its full-year guidance. The previous range was $4.75 to $4.85 per share. The new range is $4.72 to $4.80 per share. This reflects the share dilution to buy GE Biopharma. The deal should close sometime in Q4.

Sometime in the second half of this year, Danaher will IPO Envista Holdings, which is their dental business. The ticker symbol will be NVST. Shares of DHR hit a new 52-week high last week.

I’m also going to include Signature Bank (SBNY). The bank hasn’t said yet when it will report earnings, but going by previous years, July 18 is a good candidate.

Signature may be one of our most frustrating stocks to own. The stock seems to move in big streaks. SBNY was a 30% winner for us this year by February 11. After that, it started to lag. Fortunately, SBNY is on the rise again.

Three months ago, the shares got dinged after the bank missed estimates by 12 cents per share. For Q2, Wall Street expects earnings of $2.71 per share. The stock is currently going for about ten times next year’s earnings. With the earnings report, the bank may increase its dividend as well.

That’s all for now. In addition to earnings reports, there are some key economic reports next week. On Tuesday, we’ll get the latest report on retail sales and industrial production. Then on Wednesday, the report on housing starts is released. Thursday is jobless claims, and Friday is consumer confidence. We’ll also get an update on the budget for this year. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. Next Friday, July 19, I’ll be on Bloomberg TV’s market wrap segment at 4 p.m. Tune in!

France Moves to Tax Tech Giants, Stoking Fight With White House

Beijing Signals Talks at Early Stage as Trump Vents Frustration

Jerome Powell Is Becoming Central Banker to the World

This Could Be a Rare Time When It’s Smart to Fight the Fed

Bond Returns Have Been Spectacular. Don’t Count on a Sequel.

Buying Lattes Is Not Keeping You From Being Rich

Amazon Plans High-End Echo, Ramps Up Work on Alexa Home Robot

As Nations Look to Tax Tech Firms, U.S. Scrambles to Broker a Deal

Volkswagen to Contribute $2.6 Billion to Ford’s Autonomous Venture

Daimler Warns on Profit Again, Blames Diesel and Recall Costs

Accenture Picks Julie Sweet as Chief Executive

Bed Bath & Beyond Is Circling the Drain

Jeff Miller: Stock Exchange: Are You Guilty Of Risk Creep?

Howard Lindzon: The Tariff Man

Ben Carlson: Trends That May End With The Baby Boomers

Be sure to follow me on Twitter.

This time it’s the Dow’s turn to break a milestone. The index broke through 27,000 this morning. Jay Powell testifies again today but this time before the Senate.

This morning’s CPI report said that inflation rose 0.1% in June. Economists were expecting no change.

However, core inflation rose by 0.3%. That’s the biggest monthly increase since January 2018.

The so-called core CPI was boosted by strong increases in the prices for apparel, used cars and trucks, as well as household furnishings.

There were also increases in the cost of healthcare and rents. In the 12 months through June, the core CPI climbed 2.1% after advancing 2.0% in May.

The overall CPI edged up 0.1% last month, held back by cheaper gasoline and food prices. The CPI rose 0.1% in May. It increased 1.6% year-on-year in June after rising 1.8% in May.

Economists polled by Reuters had forecast the CPI unchanged in June and rising 1.6% year-on-year.

The Fed, which has a 2% inflation target, tracks the core personal consumption expenditures (PCE) price index for monetary policy. The core PCE price index increased 1.5 percent year-on-year in May and has undershot its target this year.

Central Banker With Too Much Gold Wants Treasuries Instead

The Nordic Model May Be the Best Cushion Against Capitalism. Can It Survive Immigration?

Bleak China Autos Outlook Triggers Raft of Profit Warnings

U.S. Announces Inquiry of French Digital Tax That May End in Tariffs

China and U.S. Differ Over Agricultural Purchases Trump Boasted About

What Powell’s Rate Cut Signal Means for China’s Central Bank

Wall Street Banks Bailing on Troubled U.S. Farm Sector

Want to Profit From a Trade War? There’s an Investment Fund for That

As Fresh Water Grows Scarcer, It Could Become a Good Investment

Deutsche Bank Faces U.S. Justice Department Probe Over 1MDB

Reckitt to Pay $1.4 Billion to End Opioid Addiction Treatment Probes

Now Fruit Juice Is Linked to a Higher Cancer Risk

Jeff Carter: New Security Token on Open Finance Platform

Cullen Roche: Will Active ETFs Save Active Management?

Roger Nusbaum: Is Maximum Optionality The Most Important Gift You Can Give Yourself?

Be sure to follow me on Twitter.

For a brief moment this morning, the S&P 500 broke 3,000. Of course, this is an arbitrary number, but it’s worth reflecting on the market’s stunning climb. Ten years ago, the index was around 900. For context, the S&P 500 broke 30 on August 16, 1929 (this was the old S&P 90). The S&P 500 broke 300 on March 23, 1987.

Fed Chairman Jay Powell testified today before the House Financial Services Committee. Tomorrow, he’ll go before the Senate. His comments have been interpreted as being dovish. In other words, the Fed may cut at the end of this month. That’s good for stocks and it’s why we’re up today.

The Fed also released the minutes from their June meeting. These were largely seen as helping the case that the Fed will soon cut rates. The futures market currently thinks there’s a 100% chance the Fed will cut in three weeks. There’s another 73% chance that the Fed will cut again in September. (And a third cut by Christmas!)

Japan Curbs Could Drag On, Hurt Global Economy: Moon

UK Watchdog Says All Top Accountants Fail Audit Quality Test

Trump’s Concern About Strengthening Dollar Shows Up in Fed Interviews

Fed, Pressed by Trump to Cut Rates, Faces Fire No Matter What It Does

Wall Street Unbound: Old Shackles Quietly Disappear Under Trump

Amazon Customer Helpline Not Required, Says Europe’s Top Court in Boost for E-commerce

Trump Administration Will Allow Some Companies to Sell to Huawei

Apple Starts China App Development Program in Services Business Push

De Niro and Netflix Bet That New York Can Be a New Hollywood

IBM Closes Its $34 Billion Acquisition of Red Hat

The New Deutsche Bank Might Actually Be Better. But Authorities Should Be Prepared If It Isn’t

Nick Maggiulli: The Price of Admission

Howard Lindzon: The Markets – What Happened In The First Half of 2019…and Investing For a New Cold War

Ben Carlson: 3 Ways to Decrease Your Portfolio’s Volatility

Michael Batnick: The 7 Deadly Sins of Investing & Talk Your Book: The Acquirer’s Fund

Be sure to follow me on Twitter.

Global Recession Risks Are Up, and Central Banks Aren’t Ready

How Each Country Contributed to the Explosion in Energy Consumption

Turkey’s Long, Painful Economic Crisis Grinds On

Fed Chairman Jerome Powell’s Approach to Interest-Rate Policy Wins Bipartisan Backing

Judge Blocks Trump Rule Requiring Drug Companies to List Prices in TV Ads

Why Olympic Steel Should Acquire A.M. Castle

Deutsche Bank Shares Plunge as Skepticism Mounts Over Revamp

Kohl’s Is Betting on Amazon Returns to Drive Sales

Richard Branson’s Space Unit to Go Public

Apple: The Worst Case Scenario

PepsiCo Results Beat Estimates on Demand for Sodas, Chips

Collectors Are Shelling Out $395 for Bear Stearns Stock Certificates

Cullen Roche: Is Value Investing Dead?

Joshua Brown: How Economic Data Works

Roger Nusbaum: Is Financial Resiliency Your Most Important Trait?

Be sure to follow me on Twitter.

The market is down today but it’s nothing too severe. The strong jobs report from Friday doesn’t seem to have had much impact on the markets. The indicators still show that Wall Street overwhelmingly expects rate cuts soon. Personally, I just don’t see it, but I’m not an FOMC member.

This week, Chairman Powell will testify before Congress. We’ll learn more about where he sees the economy. The questions from the members of Congress usually don’t help the reputation of Congress.

We’ll also get a look at the minutes from the Fed’s last meeting. We’ll also finally get a look at earnings. There hasn’t been much real news on our Buy List stocks in a few weeks.

In Firing Central Bank Chief, Turkey’s Leader Trades Credibility for Growth

Fed Easing Could Prompt First China Rate Cut in Four Years

Where to Invest When the Fed Cuts Rates

Morgan Stanley Turns Bearish on Global Stocks as Challenges Grow

Deutsche Bank Plans Radical Surgery After CEO Runs Out of Options

The ‘Texas Miracle’ Missed Most of Texas

Hedge Funds Chart Course Through ‘IMO 2020’ Storm

Huawei Outlines Investment Plans in Poland Depending on 5G Role

Amazon Workers Plan Prime Day Strike Despite $15-an-Hour Pledge

British Airways Faces Record $230 Million Fine for Data Breach

Microsoft Closes The Book On Its E-Library, Erasing All User Content

Mad Magazine, Irreverent Baby Boomer Humor Bible, Is All but Dead

Michael Batnick: Stop Counting Other People’s Money

Jeff Miller: Who Really Runs the Fed?

Ben Carlson: The Thing That’s Probably Blowing a Hole in Your Budget & My Questions About Negative-Yielding Debt

Be sure to follow me on Twitter.

We got a strong jobs report this morning. The U.S. economy created 224,000 net new jobs last month. That was a lot more than expectations. The unemployment rate ticked up to 3.7%.

In the past year, average hourly earnings are up 3.1%. The broader U6 unemployment rate is 7.2%.

-

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His Buy List has beaten the S&P 500 over the last 20 years. (more)

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His Buy List has beaten the S&P 500 over the last 20 years. (more)

-

Archives