-

There’s No Small-Cap Market

Posted by Eddy Elfenbein on April 13th, 2017 at 11:39 amOne of the misunderstood points of financial markets is that Affect A is very often the outgrowth of Effect B.

A good example is volatility. Commentators often discuss volatility as if it’s an entity above and apart from the market, but that’s not really the case. In reality, movements in the VIX are strongly correlated to what the market recently did. I once found a 70% correlation between the VIX and the distance the S&P 500 is from its six-month high. Markets don’t rise because volatility is low. Instead, volatility falls because the market is up.

Another example is gold. It’s not some mystery risk quotient. Rather, movements in gold are strongly tied to movements in real interest rates. Sure, there’s some noise mixed in, but once you clear things off, that’s what’s really going on.

Today I want to turn my sights to the small-cap market. There’s a great deal of literature about the “small cap premium.” Frankly, I’m pretty skeptical that it truly exists. Even if it does, it appears to be quite small and highly volatile. The data shows that small-caps have underperformed for several years at a time.

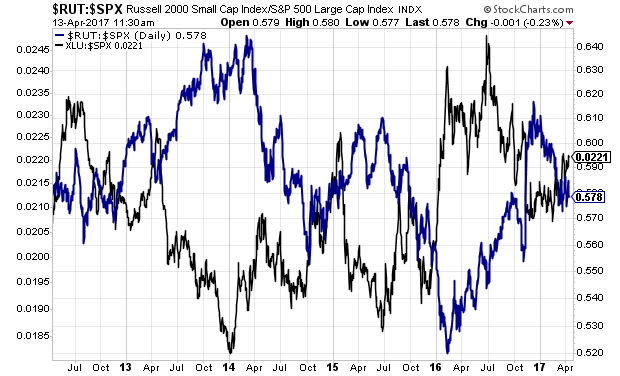

Likewise, movements in the Russell 2000 aren’t anything magical. The Russell 2000 is largely the S&P 500 just without utility stocks. Check out this chart. It’s the Russell 2000 divided by the S&P 500 (blue line) compared with the Utility ETF divided by the S&P 500 (black line).

Over five years, and they’re like mirror images.

My point is that for me to be convinced that there’s truly a small-cap premium, I would need to see a comparison of similar companies in similar industries with similar balance sheets and similar risk profiles. Obviously that can’t literally be done, but in a theoretical exercise, once everything is corrected for, I doubt there’s much of a small-cap premium.

-

Morning News: April 13, 2017

Posted by Eddy Elfenbein on April 13th, 2017 at 7:05 amOil Retreats as U.S. Production Gain Offsets Stockpile Decline

Venezuela Staves Off Default, But Low Oil Prices Pose a Threat

China Exports Jump the Most in Two Years as Imports Moderate

Trump Isn’t Wrong on China Currency Manipulation, Just Late

Trump Liking Yellen Ignites Prospects for Fed Policy Continuity

Wounded by ‘Fearless Girl,’ Creator of ‘Charging Bull’ Wants Her To Move

This Is The Jeff Bezos Playbook For Preventing Amazon’s Demise

Tesla Seeks Independent Directors as Board’s Musk Ties Eyed

Lessons From the United Airlines Debacle

Fox News’s $200 Million Golden Goose Gives CEO His Biggest Test

Investors Are Cherry-Picking the Assets of a Fallen Renewable Energy Giant

KPMG Fires 6 Over Ethics Breach on Audit Warnings

Jeff Miller: Are You Fooled By This Chart?

Cullen Roche: (Another View on) The Slowdown in Lending: A Rorschach Test

Be sure to follow me on Twitter.

-

The S&P 500 Loses Its 50-DMA

Posted by Eddy Elfenbein on April 12th, 2017 at 5:04 pmFor the first time since November 8th (Election Day), the S&P 500 has closed below its 50-day moving average. We traded above the 50-DMA for more than five straight months. This is one of the longest such streaks in recent years.

Today’s close of 2,344.93 is the lowest since the closing low from March 27 of 2,341.59. Interestingly, today’s intra-day low dipped to 2,341.18, a hair below that key mark.

-

Amazon’s Letter to Shareholders

Posted by Eddy Elfenbein on April 12th, 2017 at 12:42 pmHere’s a sample:

“Jeff, what does Day 2 look like?”

That’s a question I just got at our most recent all-hands meeting. I’ve been reminding people that it’s Day 1 for a couple of decades. I work in an Amazon building named Day 1, and when I moved buildings, I took the name with me. I spend time thinking about this topic.

“Day 2 is stasis. Followed by irrelevance. Followed by excruciating, painful decline. Followed by death. And that is why it is always Day 1.”

To be sure, this kind of decline would happen in extreme slow motion. An established company might harvest Day 2 for decades, but the final result would still come.

I’m interested in the question, how do you fend off Day 2? What are the techniques and tactics? How do you keep the vitality of Day 1, even inside a large organization?

Such a question can’t have a simple answer. There will be many elements, multiple paths, and many traps. I don’t know the whole answer, but I may know bits of it. Here’s a starter pack of essentials for Day 1 defense: customer obsession, a skeptical view of proxies, the eager adoption of external trends, and high-velocity decision making.

Read the whole thing.

-

Morning News: April 12, 2017

Posted by Eddy Elfenbein on April 12th, 2017 at 7:07 amGlobal Economic Recovery Is Gaining Momentum, IMF’s Lagarde Says

World Trade Seen Growing 2.4% in 2017, Uncertainty Weighs

Trump’s Message to Bankers: Wall Street Reform Rules May Be Eliminated

Trump’s Trademark Continues Its March Across the Globe, Raising Eyebrows

The Correct Question To Ask About The Google, DoL, Spat Over Gender Inequality In Pay

United CEO Apologizes Again After First Mea Culpa Falls Flat

Toshiba Casts Doubt on Its Ability to Stay in Business

Uber Has Lost Its Most Important Political Asset In The UK

Wal-Mart to Discount 1 Million Online Items Picked Up in Stores

Elliott Management Seeks to Remove Akzo Nobel Chairman

Subaru Makes an Even Sleeker Outback

Yahoo Is Sued Over $17 Million Fund for Chinese Dissidents

DALIO: ‘I don’t think we’re going to have a radical change in the economy’

Howard Lindzon: Reading Venture Capitalists

Jeff Carter: The Answer is “Delaware C Corp”

Be sure to follow me on Twitter.

-

Stocks, Bonds and the Election Cycle

Posted by Eddy Elfenbein on April 11th, 2017 at 2:26 pmThis is one of those instances where I did some research and it showed absolutely nothing. Oh well, that’s how a lot of research goes. Still, I’ll post the results anyway.

I was curious to see if there’s a cyclical pattern to the equity risk premium. In this case, I wanted to see how stocks perform relative to long-term corporate bonds (the risk premium more often uses short-term bills).

I used the four-year Presidential Election Cycle. The average behavior of stocks during the period is well-known and I’ve written about it before. But what about bonds? I wasn’t sure if there’s a significant cycle involving corporate bonds.

As it turns out the answer is no. Here’s what the average cycle looks like:

The blue line represents the average return of the stock market over the four years of the election cycle. The data points are monthly. The first 12 are the mid-term year, followed by the pre-election year, election year and post-election year.

The red line is the same but for corporate bonds. In this case, there’s almost no variability in returns. It’s a line that rises about 0.5% each month, every month. There’s not one instance of an average four-month period when corporate bonds lost money. Any movement in the equity risk premium is almost entirely due to stocks.

-

Express Scripts CEO Defends PBMs

Posted by Eddy Elfenbein on April 11th, 2017 at 1:03 pmHere’s a brief clip of the CEO of Express Scripts (ESRX) defending PBMs from the allegation that they’re responsible for high drug prices.

-

When Europe Leads, Here’s What Happens

Posted by Eddy Elfenbein on April 11th, 2017 at 12:55 pm -

Oppenheimer Knocks Alliance Data Systems

Posted by Eddy Elfenbein on April 11th, 2017 at 11:39 amThis morning, Oppenheimer initiated coverage on Alliance Data Systems (ADS) with an underperform rating. That seems to have knocked the shares down more than 4%. (I’m not aware of any other news that would have impacted the stock.)

The company is due to report earnings on April 20. Wall Street expects earnings of $3.89 per share.

-

JFK Attacks the Steel Industry

Posted by Eddy Elfenbein on April 11th, 2017 at 10:25 amFifty-five years ago tomorrow, President Kennedy attacked the steel industry. Gary Alexander explains the fallout.

Fifty-five years ago this week, on April 12, 1962, President John Kennedy held a special press conference to demand that the executives of U.S. Steel (and many other domestic steel companies) roll back their recently-announced $6 per ton price increase. He accused steel executives of being virtually traitorous in their “pursuit of private power and profit.” He said that the Department of Defense would only order steel from the firms that rolled back prices. Steel companies quickly complied, rolling back prices the next day.

By the next day, Friday the 13th of April 1962, the nation’s eight biggest steel companies surrendered to the President’s demands in quick succession: At 3:05 pm, Kaiser Steel was the first domino, followed by Bethlehem Steel at 3:21. U.S. Steel bowed at 5:25, followed by Republic Steel (5:57), Pittsburgh Steel (6:26), Jones & Laughlin (6:37), National Steel (7:33), and finally Youngstown Sheet & Tube (at 9:09).

That did not end the war of words. When it came time to announce U.S. Steel’s disappointing first-quarter 1962 earnings on May 7, CEO Roger Blough told his shareholders: “This concept is incomprehensible to me – the belief that Government can ever serve the national interest in peacetime by seeking to control prices in competitive American business, directly or indirectly, through force of law or otherwise.”

All through May of 1962, stocks kept falling. From its December 1961 peak at 741, the Dow fell by 29% in six months, to 525 by late June, 1962. It turned out to be the worst bear market to befall America in the 32-year expansion between 1942 and 1974. May 28, 1962 was the worst day on Wall Street since the 1929 crash. On that day, steel stocks dropped to 50% of their 1960 levels, as part of a long, long decline.

Steel companies weren’t price-gouging. Profits at U.S. Steel fell 61% from 1958 to 1963, with the biggest drop coming in 1962. The industry lost over 100,000 jobs from 1958 to 1960, including 70,000 jobs lost at U.S. Steel alone. Their profit margin was cut in half. While salaries in the steel industry rose 13% from 1958 to 1961, profits fell, as 85% of U.S. Steel’s 1961 profits were paid out in shareholder dividends.

In 1958, U.S. Steel was #4 in the Fortune 500, and Bethlehem Steel was #9. By 1985, U.S. Steel was in the process of changing its mix of businesses, emerging as USX Corp. The only pure steel company in the Fortune 100 in 1985 was Bethlehem Steel, ranked #68. Clearly, the U.S. steel industry was slowly dying.

The President killed an already-dying industry. By July 1962, the steel industry was working at just 55% capacity, vs. 70% in April, when the President attacked them. Very soon, Japan began to dominate the steel market, which was already beset by competition from non-steel construction products made from plastics, aluminum, cement, or glass. While the normal challenges of business are always present, the President’s attack contributed greatly to the decline of the U.S. steel industry over the next few decades.

As history shows, Presidents possess great powers to inspire or destroy when they propose to take any particular industry to the woodshed. Chances are, market forces are already disciplining those companies.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His