-

Morning News: April 11, 2017

Posted by Eddy Elfenbein on April 11th, 2017 at 7:07 amChina Is Playing a $9 Trillion Game of Chicken With Savers

Yellen Signals Shift From Stimulating Economy to Sustaining Growth

Trump Takes Credit for Planned $1.33 Billion Toyota Spending

Google is Fighting The Labor Department About Equal Pay For Women, And Both Can’t Be Right

AT&T Bets On 5G With Straight Path Communications Buy For $1.25 Billion

Seven Wells Fargo Managers in Board’s Review—and Their Fates

Toshiba Files Earnings Without Auditor Endorsement, Delisting Risk Rises

Toshiba Casts Doubt on Its Ability to Stay In Business

G.M. Takes a Back Seat to Tesla as America’s Most Valued Carmaker

Whole Foods’ Shareholder Battle Sets Up a Clash of Foodie Gurus

Vizio’s $2-Billion Sale to LeEco Called Off Over ‘Regulatory Headwinds’

Why Delta Air Lines Paid Me $11,000 Not To Fly To Florida This Weekend

Scammers Used SeekingAlpha for Bogus Stock Promotions, SEC Says

Roger Nusbaum: Blame It On The Rain

Josh Brown: Some Questions for the Bank CEOs

Be sure to follow me on Twitter.

-

The Best Retail Stocks to Buy Now

Posted by Eddy Elfenbein on April 10th, 2017 at 7:54 pm -

Tesla Surges on Upgrade

Posted by Eddy Elfenbein on April 10th, 2017 at 5:52 pm -

Morning News: April 10, 2017

Posted by Eddy Elfenbein on April 10th, 2017 at 6:54 amChina Insurance Probe Won’t Halt Firms’ Overseas Urge

Oil Surplus or Scarcity? Shale Makes It Even Harder to Predict

Geopolitics From France to Korea Keep Investors Cautious

Impressive Market Resilience Shouldn’t Be Taken for Granted

Trump-Taxes: President Scraps Tax Plan, Timetable Threatened

FCC Chief Ajit Pai Develops Plans to Roll Back Net Neutrality Rules

Battle of Billionaires: Son Set to Clash With Bezos in India

How Steven Colbert Finally Found His Elusive Groove

Women At Google Face ‘Extreme, Systemic’ Wage Gap, According To Labor Dept. Suit

Fox News Troubles Heighten Scrutiny of Rupert Murdoch’s Plan to Acquire Sky

LIBOR: Bank of England Implicated in Secret Recording

Barclays Reprimands Chief Executive For Trying To Identify Whistleblower

Jeff Miller: Will an Earnings Surge Revive the Stock Rally?

Howard Lindzon: The Insurance Boom in Fintech, Street Contxt and Bloomberg Terminal Rivals

Be sure to follow me on Twitter.

-

March 2017 NFP = 98,000

Posted by Eddy Elfenbein on April 7th, 2017 at 8:31 amThe March jobs report is out. The U.S. economy created 98,000 net new jobs last month. That’s well below expectations of 180,000, but the unemployment rate fell to 4.5%.

Manufacturing gained 11,000 jobs, but retail lost nearly 30,000 jobs.

For me, the key number is average hourly earnings. That rose by 0.2% in March. In the last year, AHE is up 2.7%.

Here’s a chart of NFP.

The unemployment rate is lower now than at anytime between March 1970 and April 1998.

12-month gain average hourly earnings.

-

CWS Market Review – April 7, 2017

Posted by Eddy Elfenbein on April 7th, 2017 at 7:08 am“The stock market is designed to transfer money from the active to the patient.”

– Warren BuffettThe stock market has apparently reverted to its tame ways. For the last eight days in a row, the S&P 500 has closed between 2,352 and 2,369. That’s a fairly narrow range. Last week, I thought we might see some action when the S&P 500 briefly dipped below its 50-day moving average. That hadn’t happened since November, but the index failed to close below this crucial technical support level.

So the boring market has continued.

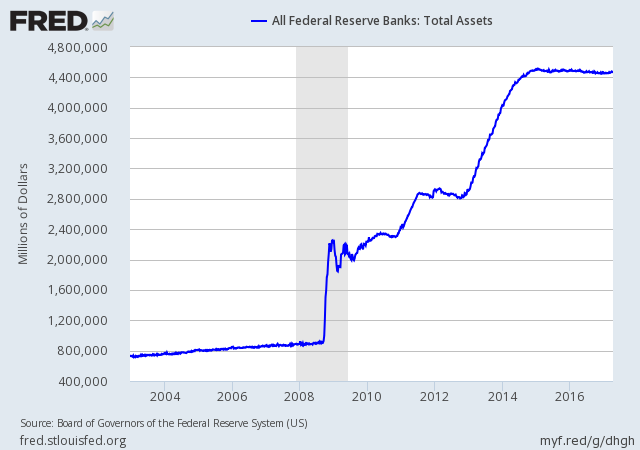

Even though the stock market peaked over a month ago, there hasn’t been much momentum in either direction. But there was some interesting news from Washington this week. We learned that the Federal Reserve is finally considering ways to reduce its gargantuan balance sheet. This could be an important issue later this year. I’ll tell you what it means.

Now we’re in April and first-quarter earnings season is about to begin. This could be one of the better quarters in recent years. I’ll tell you what to expect. I’ll also discuss this week’s earnings report from RPM Inc., plus I have some other Buy List updates for you. But first, let’s look at what the Fed has planned in order to unwind its gigantic balance sheet.

Don’t Panic Over the Fed’s Balance Sheet

On Wednesday, the Federal Reserve released the minutes from last month’s policy meeting. This is the one where the Fed decided once again to raise interest rates. This was a notable increase because it wasn’t foreseen a month beforehand. By the time it happened, it wasn’t a surprise. But for those key weeks, the expectations completely changed. I think Wall Street was surprised by how forceful and direct the Yellen Fed could be.

The Fed has become pretty good at conveying its intentions to Wall Street. But that’s regarding interest rates. What about the Fed’s balance sheet? Before the world economy went kablooey nine years ago, the Fed’s balance was less than $1 trillion. Then the Fed got busy. Very, very busy. Today, the balance sheet is $4.5 trillion.

As you might expect, this is a wee bit disconcerting for investors and folks inside the government. The problem is that if the Fed moves too quickly and dumps its holdings, that could cause long-term interest rates to rise. The Fed has been reinvesting the proceeds of its securities, but that could end soon. According to the minutes from the March meeting, “Provided that the economy continued to perform about as expected, most participants anticipated that gradual increases in the federal funds rate would continue and judged that a change to the Committee’s reinvestment policy would likely be appropriate later this year.”

As always, I apologize for quoting Fed officials. Despite their dull writing, this is actually a big honking deal. First off, let’s make the important point that the Fed will keep using interest-rate adjustments as its main policy tool. For its balance sheet, almost certainly, the plan will be to deflate it slowly and quietly. We don’t want a repeat of Wall Street’s “Taper Tantrum” in 2013. My guess is that the first step will be a decision to end reinvestment of agency debt, not Treasury debt.

As we know, the bond market is notoriously ornery. Yes, they’ll scream and holler every step of the way. But ultimately, I doubt the Fed’s plans will have a sizeable impact on long-term rates. There’s simply too much demand from investors all over the world to hold U.S. debt. Plus, there’s no hurry for the Fed to lower its holdings. If need be, they can wait out a storm.

Instead, my fear is that the Fed will raise rates too much too fast. Looking at the data, there’s not a great need for higher rates. Later today, we’ll get the jobs report for March. We’ll see more job gains. I hope we’ll see more improvement in wages, but we have a long way to go. Inflation is still not a problem. While oil has moved up recently, it’s down for the year.

Eric Rosengren, the top dog at the Boston Fed, recently said he thinks the Fed needs four hikes this year. I’m sorry, but I just don’t get it. Maybe one more raise this year. Outside chance of two more. The problem, of course, is that just because it’s a bad idea doesn’t mean the Fed won’t do it.

In the last year, long-term rates have gapped up significantly, and I’m starting to question how much of that is truly justified. I wouldn’t be surprised to see the yield on the 10-year Treasury fall back below 2%. Of course, much of this outlook is dependent on where the economy goes from here. Very soon, we’re going to get a slew of earnings reports. Let’s take a closer look at what Q1 earnings season has in store.

Preview of Q1 Earnings Season

According to the latest estimates, Wall Street expects earnings growth of 9.1% for Q1. What helps that figure is the comparison against weak numbers from a year ago. Still, if the forecast is correct, that would be the fastest growth rate since Q4 of 2011. Bank of America Merrill Lynch noticed a fascinating factoid. In company earnings calls for Q4, 52% of companies used the word “optimistic.” That’s the highest ever in data going back to 2003.

Another welcome change is that earnings estimates haven’t been slashed as they’ve been in previous quarters. It’s the norm to expect Wall Street’s forecasts to be pared back as earnings season approaches, but it’s been far more muted this time.

This earnings season will also be different because we’ll see better results from energy companies. The downturn in oil was brutal for many earnings stocks, but prices have rebounded. Typically, the big banks report early on in the earnings season. That often sets the tone for the rest of the earnings. Our own Signature Bank (SBNY) is due to report on April 17.

We’re also seeing decent topline growth. The early part of the bull market was often criticized for being driven by cost-cutting. Companies were growing their profits but not growing their firms. They were just laying off people. At some point, we needed to see more customers come in and buy more things. We’re now seeing more jobs leading to more spending leading to higher revenue. Wall Street currently expects Q1 revenue growth of 7.1%. That will be a five-year high. Not surprisingly, we recently saw consumer confidence touch a 16-year high.

We’re also somewhat safer now from an issue in previous quarters, namely the strong U.S. dollar. The greenback soared after the election, but it has pulled back since the start of the year. Last year, you may recall how often companies stressed that their “currency-adjusted” profits were doing just fine.

I’m particularly looking forward to the earnings report from Microsoft (MSFT). Wall Street currently expects earnings of 70 cents per share from the software giant. They should have little trouble topping that. Now let’s look at the only Buy List earnings report we’ve had in five weeks.

RPM Inc. Is a Buy Up to $55 Per Share

On Thursday, RPM Inc. (RPM) reported fiscal third-quarter earnings of nine cents per share. That result, however, includes five cents per share related to the company’s “Restore intangible impairment and the European facility closure.” Looking past that, RPM made 14 cents per share, which was three cents better than estimates.

I should explain that RPM is on the February/May/August/November reporting cycle. As such, they’re one of our few Buy List earnings reports over the last several weeks. Since most of our stocks (and most stocks in general) ended their last quarter in March, we’ll see a flurry of earnings reports soon.

RPM’s earnings report is a bit unusual because only a very small portion of its annual profit comes during their fiscal Q3. By my rough estimate, Q3 makes up about 5% to 7% of RPM’s full-year haul. The company expects full-year earnings to range between $2.57 and $2.67 per share. That’s a reduction of five cents per share from their previous forecast due to charges I mentioned before. Quarterly revenue rose to $1.02 billion, which was just shy of estimates of $1.04 billion.

“Our businesses serving the U.S. commercial construction market again experienced solid organic growth. Most businesses in Europe were up in the low- to mid-single-digit range in local currencies, and current-year acquisitions contributed nicely to the segment’s overall sales growth. We were very pleased with the strong EBIT leverage achieved on solid top-line sales,” stated Sullivan.

RPM is a good example of a solid company that’s having a sluggish year. The key takeaway is that profits will be about the same as last year. There’s no reason to run. The shares pulled back 3.6% on Thursday. This week, I’m dropping my Buy Below down to $55 per share.

Buy List Updates

I also want to change a few Buy Below prices. Shares of Cerner (CERN) have been doing quite well recently. I’m going to bump our Buy Below up to $62 per share. It’s our top-performing stock this year, and it was one of our worst last year.

Shares of JM Smucker (SJM) have been trending downward over the past month. I’m lowering my Buy Below to $138 per share. Fiscal Q4 earnings are due out in early June.

I’m also going to raise the Buy Below on HEICO (HEI) to $90 per share, ahead of the stock’s split later this month. HEICO will be split 5-for-4, which means shareholders will be getting 25% more shares but the share price will fall about 20%.

That’s all for now. The March jobs report will be out later this morning. I expect to see more gains in non-farm payrolls, but I’m especially curious to see any gains in earnings. There’s been some improvement here. There will be a few early earnings reports next week, but none from our Buy List. The stock market will be closed next Friday for Good Friday. This is the one day of the year when the market is shuttered and most government offices are open. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: April 7, 2017

Posted by Eddy Elfenbein on April 7th, 2017 at 7:04 amBOE’s Carney Urges Banks to Prepare for Any Brexit Outcome

U.S. Jobs Report: What to Watch For

U.S. South, Not Just Mexico, Stands in Way of Rust Belt Jobs Revival

Trump and Warren Agree? Maybe, on Plan to Shrink Big Banks

The $90 Billion Investor Who’s Out to Fire Wall Street

Wall Street Is Making It Harder To Buy A Car

Even Amid Trade Tensions, Ford Pushes Pickup Trucks in China

212 Tesla Owners Can’t Be Wrong: How Tesla Can Be Worth More Than Ford

Twitter Sues the Government to Block the Unmasking of an Account Critical of Trump

Billionaire Ev Williams Plans to Sell Up To 30% Of His Twitter Stake

Adidas to Mass-Produce 3D-Printed Shoe With Silicon Valley Start-Up

Uber Rival Lyft Raises $500 Million in Funding

Norway to Build $315 Million Ship Tunnel in World First

Roger Nusbaum: Avoiding Groupthink Yield Chasing

Jeff Miller: Stock Exchange: Finding Trading Ideas in a Low Volatility Market

Be sure to follow me on Twitter.

-

RPM Earns 14 Cents Per Share

Posted by Eddy Elfenbein on April 6th, 2017 at 12:03 pmThis morning, RPM Inc. (RPM) reported fiscal third quarter earnings of 14 cents per share. This was for the quarter that ended on February 28. Wall Street had been expecting earnings of 11 cents per share.

This is a bit unusual because only a very small portion of RPM’s annual profit comes during their fiscal Q3. The company expects full-year earnings to range between $2.57 and $2.67 per share. That’s a reduction of five cents per share from their previous forecast due to “combined third quarter charges for the Restore intangible impairment and the European facility closure.”

Quarterly revenue rose to $1.02 billion which was just shy of estimates of $1.04 billion.

“Our businesses serving the U.S. commercial construction market again experienced solid organic growth. Most businesses in Europe were up in the low- to mid-single-digit range in local currencies and current-year acquisitions contributed nicely to the segment’s overall sales growth. We were very pleased with the strong EBIT leverage achieved on solid top-line sales,” stated Sullivan.

-

Morning News: April 6, 2017

Posted by Eddy Elfenbein on April 6th, 2017 at 6:56 amChina Moves a Step Forward in Its Quest for Food Security

Traders Need to Start Giving the Euro and Pound Some Respect

Traders Bet the Fed Will Slow Rate Hikes to Shrink Balance Sheet

Flood of U.S. Oil to Asia Comforts Tanker Market Trashed by OPEC

Fed and Trump Signals Give Stocks Double Trouble

Cohn Backs Wall Street Split of Lending, Investment Banks

Jeff Bezos Says He Is Selling $1 Billion a Year in Amazon Stock to Finance Race to Space

A Coffee Empire Grows as Panera Is Sold to JAB Holding Company

Unilever Promises Cash to Shareholders After Rebuffing Kraft Approach

Boeing Forms Venture Group, Invests in Two Tech Startups

Twitter Creates ‘Lite’ Version For Data-Starved Users

Cody Brown Has a Broad Vision for Virtual Reality

7-Eleven Operator to Buy U.S. Stores From Sunoco For $3.3 Billion

Josh Brown: The State of Wealth Management in 2017

Howard Lindzon: The Year 2017 – So Much Wealth and So Much Cheating

Be sure to follow me on Twitter.

-

Morning News: April 5, 2017

Posted by Eddy Elfenbein on April 5th, 2017 at 7:12 amTrump and Xi: Two Imposing Leaders With Clashing Agendas

Behind Trump’s Trade Deficit Obsession: Deficient Analysis

Richmond Fed President Resigns

Even Under Trump, a U.S. Coal Giant Plots Cautious Comeback Plan

Dimon: U.S. Is ‘Exceptional’ But Faces ‘Significant’ Problems

Global Shipping Fleet Braces for Chaos of $60 Billion Fuel Shock

To Unravel Tesla, GM and Einhorn, Look To Oil

Consumers In Line For $70 Million In Refunds After Amazon, FTC Settlement

Panera Is Exploring Possible Sale After Receiving Interest

America Is ‘Over-Stored’ And Payless ShoeSource Is The Latest Victim

Ralph Lauren Is the Latest Fashion Victim in a New Era for Retailers

The Jenna Lyons Era at J. Crew Comes to an End

`O’Reilly Factor’ Advertisers Jump Ship in Blow to Fox News

Roger Nusbaum: Brexit Is On The Clock

Jeff Carter: How To Do Social Entrepreneurship Right: Guard Llama

Be sure to follow me on Twitter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His