-

CWS Market Review – March 3, 2017

Posted by Eddy Elfenbein on March 3rd, 2017 at 7:08 am“Become more humble as the market goes your way.” – Bernard Baruch

John Maynard Keynes famously spoke of how “animal spirits” can override rational human behavior. Given Wall Street’s extreme placidity of late, I think those animals are currently possums, sloths and snails.

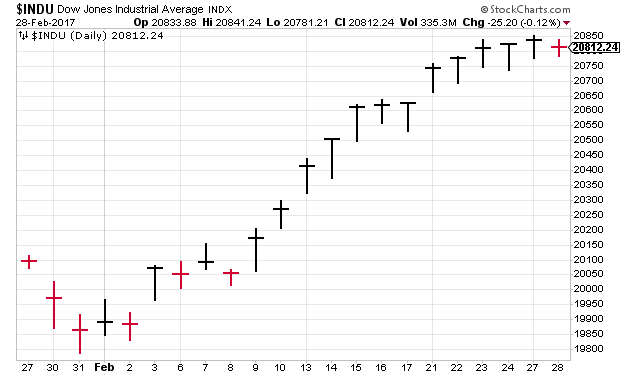

Finally, we saw some action this week. On Tuesday, the Dow snapped its 12-day winning streak, the longest in three decades. Then on Wednesday, the S&P 500 had its first daily move of over 1% in nearly three months. Surprisingly, the move was to the upside. For the first time ever, the index topped 2,400.

So what’s the cause for the burst of optimism? For one, Wall Street reacted positively to President Trump’s Tuesday address. Plus, there’s been more positive economic news. Consumer confidence is now at a 15-year high. In fact, Wall Street is beginning to think that another Fed rate hike will come in less than two weeks.

In this week’s CWS Market Review, I’ll tell you what it all means. I’ll also highlight our two Buy List earnings reports from this week. Both Ross Stores and HEICO beat estimates, plus Ross gave us an 18.5% dividend hike. I’ll also update some of our Buy Below prices. But first, let’s look at why things suddenly look so rosy on Wall Street.

Get Ready for an Ides of March Rate Hike

In December, the Federal Reserve said that they expect to raise interest rates three times this year. At the time, I said that forecast was wildly optimistic. Suddenly, it doesn’t look so wild. In just a few days, Wall Street’s view on a rate increase has shifted dramatically.

What changed? Several things came together all at once. The inflation report for January was well above expectations. Existing home sales rose to a 10-year high. The minutes from the Fed’s last meeting indicated that some members are ready to hike. This week, we learned that consumer confidence rose to a 15-year high and initial jobless claims fell to a 44-year low.

Perhaps the most influential event was when Bill Dudley, the top dog at the New York Fed, said, “I think the case for monetary policy tightening has become a lot more compelling.” After that, the rate-hike odds for March doubled.

The Fed meets again on March 14-15. Two weeks ago, before Janet Yellen testified before Congress, the futures market pegged the odds of a March rate hike at 16%. Now it’s at 79.7%. It doesn’t stop there. The odds of another hike in June are roughly 50-50.

The change of mind is impacting the financial markets in several ways. Obviously, stocks are rallying. An improving economy means consumers have more money to spend, and that means greater profits for companies. The S&P 500 is already up 6.4% this year.

The bond market is also adjusting. The “short-end” of the yield curve is the highest it’s been in years. This week, the yields on the three- and six-month Treasuries, plus the one- and two-year notes, all hit their highest levels in seven or eight years.

On Thursday, for example, the yield on the six-month Treasury closed at 0.84%. Obviously, that’s not very high, but it’s double the yield of six months ago. Let’s remember that just 17 months ago, the two-year was going for 0.08% (see chart below). The one-year Treasury is close to breaking above 1% for the first time since November 2008. After many, many false starts, it appears that yields are truly going higher.

What’s interesting is that the long end of the yield curve (over 10 years) hasn’t moved much recently. After the election, those maturities saw their yields gap up, but since the start of the new year, they’ve been fairly stable. This may suggest that the Fed won’t have to do a lot of hiking to get the job done.

When we see long-term yields go up, that generally aligns with good times for cyclical stocks. When short yields rise, that’s usually good for banks and financials. For example, on our Buy List, Signature Bank (SBNY), recently came within inches of hitting a new all-time high.

In last week’s issue, I mentioned the earnings report from Continental Building Products (CBPX). I think of the company as a classic cyclical stock. What’s interesting is that traders didn’t know what to do after the earnings report. At one point last Friday, the shares were down more than 4%. Then the market changed its mind, and CBPX rallied. From Friday’s low to Thursday’s close, the stock gained more than 12%. You never know what will happen in the short term. CBPX is now one of our seven Buy List stocks that are up double digits in 2017.

The last few weeks have been very busy with earnings reports. Now that earnings season is behind us, we’re in for a long stretch with almost no earnings. Over the next six weeks, only RPM Inc. (RPM) is scheduled to release its earnings. Now let’s turn to our two Buy List earnings reports from this week.

Ross Stores Beats and Raises Dividend

After the closing bell, Ross Stores (ROST) reported fiscal Q4 earnings (ending January 28) of 77 cents per share. That’s a good number. The deep discounter had told us to expect Q4 earnings between 72 and 75 cents per share. Wall Street pegged Q4 at 75 cents per share.

Quarterly sales rose 8% to $3.5 billion, and comparable-store sales were up 4%. The latter is the key metric to watch for any retailer, and 4% growth is quite good. For all of 2016, Ross made $2.83 per share. That’s up 13% over last year. Full-year sales rose 8% to $12.9 billion. Comp-store sales were up 4%.

Barbara Rentler, Chief Executive Officer, commented, “We are very pleased with our better-than-expected sales and earnings results for the fourth quarter and fiscal year, especially given our strong multi-year comparisons and the highly competitive and promotional holiday season. Our results continued to benefit from our ability to offer customers great values on a wide assortment of gifts and fashions for the family and the home.”

Ms. Rentler continued, “Fourth-quarter operating margin grew 90 basis points to 13.6%, up from 12.7% in the prior year. This improvement was mainly driven by our above-plan sales along with a favorable comparison of packaway-related costs versus last year’s fourth quarter. For the 2016 fiscal year, operating margin increased 40 basis points to a new record of 14.0%.”

Those are some solid numbers. Ross also approved a new, two-year $1.75 billion share-buyback program. At ROST’s current price, that’s about 6% of their outstanding shares.

Ross also bumped up its quarterly dividend from 13.5 to 16 cents per share. That’s an increase of 18.5%. Over the last seven years, Ross has raised its dividend by 300%. The new dividend is payable on March 31 to stockholders of record as of March 10.

Now for guidance. Bear in mind that Ross tends to be very conservative with their forecasts. Ross projects full-year 2017 earnings between $3.02 and $3.15 per share. That’s up 7% to 11% over 2016. However, the current fiscal year is 53 weeks long. The company estimates that the extra week adds eight cents per share. Ross sees same-store growth this year of 1% to 2%.

For Q1, Ross forecasts earnings of 76 to 79 cents per share and comp-store sales growth of 1% to 2%. This strikes me as very conservative.

Why so low? The CEO said, “There continues to be uncertainty in the political, macro-economic, and retail climates, and we also face our own challenging sales and earnings comparisons. Thus, while we hope to do better, we believe it is prudent to remain somewhat cautious in planning our business for the 2017 fiscal year.”

Ross was one of the few stocks to lose ground on Wednesday. I’m not at all concerned. Ross Stores remains a buy up to $70 per share.

HEICO Beats and Raises Guidance

Also on Tuesday, HEICO (HEI) reported fiscal Q1 earnings of 59 cents per share. That’s five cents higher than expectations. Net sales grew 12% to $343.4 million. The company makes replacement parts for the aircraft industry.

Laurans A. Mendelson, HEICO’s Chairman and CEO, commented on the Company’s first-quarter results, stating, “We are pleased to report exceptional first quarter year-over-year increases in net sales and operating income within both our Flight Support Group and Electronic Technologies Group. These results principally reflect strong organic growth of 8% within both of our operating segments as well as the excellent performance of our well-managed and profitable fiscal 2016 acquisitions.

Cash flow provided by operating activities was strong, increasing 24% to $56.0 million in the first quarter of fiscal 2017, representing 137% of net income, as compared to $45.2 million in the first quarter of fiscal 2016.

Our total-debt-to-shareholders’-equity ratio was 38.3% as of January 31, 2017. Our net-debt-to-shareholders’-equity ratio was 34.1% as of January 31, 2017, with net debt (total debt less cash and cash equivalents) of $371.4 million principally incurred to fund acquisitions in fiscal 2016 and 2015. We have no significant debt maturities until fiscal 2019 and plan to utilize our financial flexibility to aggressively pursue high-quality acquisition opportunities to accelerate growth and maximize shareholder returns.

The best news is that HEICO is raising its outlook for this year. Unfortunately, they don’t provide EPS guidance. Previously, HEICO expected sales growth of 5% to 7%, and net income growth of 7% to 10%. Now they see sales growth of 6% to 8%, and net income growth of 9% to 11%. Assuming share count doesn’t change, the EPS range works out to $2.53 to $2.57.

HEICO also said they’re considering a stock split. This week, I’m raising my Buy Below on HEICO to $89 per share.

I also want to update a few of our Buy Below prices. This week, I’m raising Fiserv’s (FISV) Buy Below to $122 per share. The shares recently had a run of rising 14 times in 16 days. I’m also raising Cerner (CERN) to $57 per share. CERN was one of our worst stocks last year but one of our best this year. Interesting how that works. I’m lifting Danaher’s (DHR) Buy Below to $90. Last week, DHR raised its dividend by 12%. Finally, I’m raising Stryker (SYK) to $136. Since mid-November, SYK has rallied more than 22%.

Before I go, here are a few links to pass along. Morningstar looked at Ingredion (INGR). Barron’s highlighted Axalta Coating Systems (AXTA). Cinemark (CNK) was featured in Forbes.

That’s all for now. The big news next week will be the jobs report on Friday, March 10. This will be the last major event before the Fed meeting. If the report is strong (over 175,000 nonfarm jobs), then that almost certainly guarantees another rate hike. It will also increase the odds for a second hike in June. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: March 3, 2017

Posted by Eddy Elfenbein on March 3rd, 2017 at 7:05 amGreece Should Be Added to ECB’s Bond-Buying List

One Bitcoin Is Now Worth More Than One Ounce Of Gold

A Fit U.S. Shale Industry Challenges OPEC Once Again

Retailers Had a Dismal Christmas and Now Comes Ryan’s Import Tax

Snap Inc Popped on its First Day, But The Crackle Needs to Come From Monetisation

How a Money-Losing Snap Could Be Worth So Much

Masayoshi Son, Sprint and a Bet on the Trump Economy

Caterpillar’s Headquarters Raided By Federal Authorities Including The DoJ And IRS

Following Earnings Miss, Costco Plans To Hike Membership Fees

WPP Drops After Projecting Slower Growth, Weak New Business

The Case For A Hollister Spinoff

Murdoch’s Fox Seeks EU Okay For $14.4 Billion Sky Takeover Bid

Hedge Fund Titans Face What Comes Next as They Pass Certain Age

Cullen Roche: Learning To Be A Good Loser

Jeff Miller: Stock Exchange: How To Trade An Overbought Market

Be sure to follow me on Twitter.

-

Josh Brown v. Mark Faber

Posted by Eddy Elfenbein on March 2nd, 2017 at 1:29 pmI’m not a fan of perma-bear Mark Faber. I especially don’t like how he eludes tough questions. That’s why I love this clip of Josh Brown trying to ask him a direct question. You’ll notice how Faber does everything he can to ignore it.

-

Morning News: March 2, 2017

Posted by Eddy Elfenbein on March 2nd, 2017 at 6:56 amWhat Booming Markets Are Telling Us About the Global Economy

Forget Email, Wormholes Are Connecting Workers Across the Globe

China Says Supports WTO After U.S. Trade Threat

Fed’s Brainard Says Interest-Rate Hike Likely Appropriate ‘Soon’

F.C.C., in Potential Sign of the Future, Halts New Data Security Rules

7 Challenges Snapchat’s Parent Company Has to Overcome Before It Can Be Wall Street’s ‘New Facebook’

Lyft Is Trying To Raise $500 Million In Its Fight Against Uber

McDonald’s U.S. Turnaround Shifts To Technology, Speedier Service

AmEx Offers Uber Rides After Chase Makes a Splash With Sapphire

AB InBev Suffers First Core Profit Decline on Brazil Slump

Wells Fargo Warns a Deeper Review May Uncover More Bogus Accounts

Yahoo’s Top Lawyer Resigns and C.E.O. Marissa Mayer Loses Bonus in Wake of Hack

Bridgewater Shakes Up Management Again as Dalio Drops Co-CEO Role

Howard Lindzon: Snaps to Snapchat…The Camera Company that Is Not a Camera

Jeff Carter: No Occupation Is Immune From Automation

Be sure to follow me on Twitter.

-

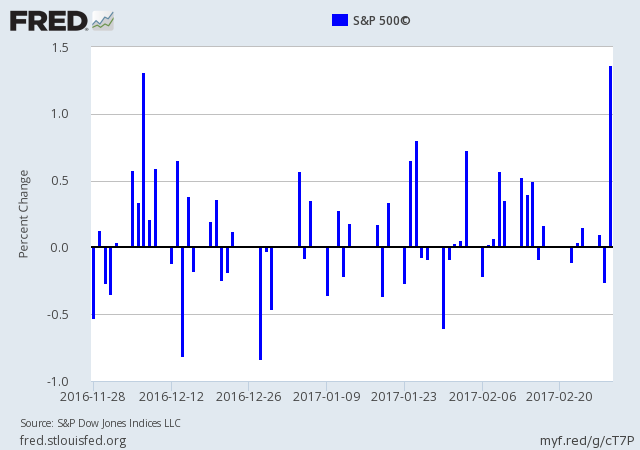

The S&P 500 Gains 1.37%

Posted by Eddy Elfenbein on March 1st, 2017 at 10:30 pmFor the first time since December 7, the S&P 500 moved more than 1% in a day. By the closing bell, the S&P 500 advanced 1.37% on the day.

The S&P 500 Financial Sector gained 2.84% today. That was followed by the Energy Sector at +2.05% and the Materials Sector at +1.82%.

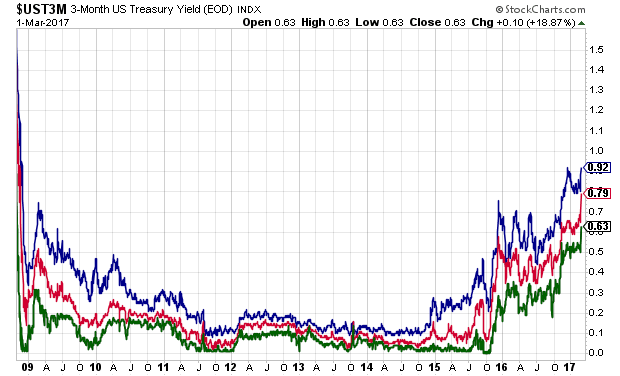

In the bond market, a few maturities set multi-year highs today. The three-month yield closed at 0.63% today which is the highest since October 28, 2008. The six-month yield closed at 0.79% today which is the highest since November 17, 2008.

The one-year yield closed at 0.92% today which is the highest since November 26, 2008. The two-year yield rose to 1.29%. That’s the highest since August 7, 2009.

Here’s a chart showing the three- and six-month yields, plus the one-year yield.

-

The 1% Streak May End Today

Posted by Eddy Elfenbein on March 1st, 2017 at 11:50 amThe S&P 500’s remarkable run of daily closes less than 1% may come to an end today. What’s most surprising is that it may end with a 1% up day.

President Trump’s speech is being warmly received by Wall Street. The S&P 500 is currently up 1.22%.

The bond market is selling off, while financials and cyclicals are doing the best. Interest rate-sensitive stocks are doing the worst.

On our Buy List, HEICO (HEI) is having a very good day after its earnings report. Currently it’s up 6.1%. Continental Building Products (CBPX) is up 5.2%. This stock had a strange reaction to what I thought was a good earnings report.

-

Morning News: March 1, 2017

Posted by Eddy Elfenbein on March 1st, 2017 at 7:11 amChina’s Richest Win, Mexican Billionaires Lose With Trump Effect

Trump’s Trade Retreat Could Hurt Push for Labor Rights Abroad

Fed Trumps Trump as Dollar, U.S. Treasury Yields Soar

Ad Buyers Push Snapchat to Have Metrics Audited

A Delivery Man Just Became One of the Richest People in China

Lowe’s Forecasts 2017 Sales Ahead of Estimates; Shares Up

Target Shares Dive on Earnings Outlook, Price Cut Plans

Taiwan’s Foxconn ‘Definitely Bidding’ for Toshiba Chip Business

Hershey To Cut Thousands of Jobs Globally

Kite Pharma’s Shares Soared Today Thanks to Its Revolutionary Blood Cancer Drug

‘I Must Fundamentally Change And Grow Up’: Uber CEO Travis Kalanick’s Big Apology

Uber Case Could Be a Watershed for Women in Tech

Hundreds of Workers Allege Sex Bias by Jeweler, Files Show

Josh Brown: Snap vs Facebook vs Twitter Cheatsheet

Roger Nusbaum: Mixed Signals From Higher Equity Prices

Be sure to follow me on Twitter.

-

The Streak Ends

Posted by Eddy Elfenbein on February 28th, 2017 at 5:05 pmAfter rising 12 days in a row, the Dow finally falls.

-

HEICO Beats and Guides Higher

Posted by Eddy Elfenbein on February 28th, 2017 at 4:41 pmAlso after the bell, HEICO (HEI) reported fiscal Q1 earnings of 59 cents per share. That’s five cents higher than expectations. Net sales grew 12% to $343.4 million.

Laurans A. Mendelson, HEICO’s Chairman and CEO, commented on the Company’s first quarter results stating, “We are pleased to report exceptional first quarter year-over-year increases in net sales and operating income within both our Flight Support Group and Electronic Technologies Group. These results principally reflect strong organic growth of 8% within both of our operating segments as well as the excellent performance of our well managed and profitable fiscal 2016 acquisitions.

Cash flow provided by operating activities was strong, increasing 24% to $56.0 million in the first quarter of fiscal 2017, representing 137% of net income, as compared to $45.2 million in the first quarter of fiscal 2016.

Our total debt to shareholders’ equity ratio was 38.3% as of January 31, 2017. Our net debt to shareholders’ equity ratio was 34.1% as of January 31, 2017, with net debt (total debt less cash and cash equivalents) of $371.4 million principally incurred to fund acquisitions in fiscal 2016 and 2015. We have no significant debt maturities until fiscal 2019 and plan to utilize our financial flexibility to aggressively pursue high quality acquisition opportunities to accelerate growth and maximize shareholder returns.

He also said the company is considering a stock split. The best news is that HEICO is raising its outlook for this year. Previously, the company expected sales growth of 5% to 7%, and net income growth of 7% to 10%. Now they see sales growth of 6% to 8%, and net income growth of 9% to 11%.

-

Ross Stores Beats and Raises Dividend

Posted by Eddy Elfenbein on February 28th, 2017 at 4:16 pmAfter the closing bell, Ross Stores (ROST) reported fiscal Q4 earnings (ending January 28) of 77 cents per share. The deep discounter had said to expect Q4 earnings between 72 and 75 cents per share. Wall Street pegged Q4 at 75 cents per share.

Quarterly sales rose 8% to $3.5 billion, and comparable store sales were up 4%. For all of 2016, Ross made $2.83 per share. That’s up 13% over last year. Full-year sales rose 8% to $12.9 billion. Comp store sales were up 4%.

Barbara Rentler, Chief Executive Officer, commented, “We are very pleased with our better-than-expected sales and earnings results for the fourth quarter and fiscal year, especially given our strong multi-year comparisons and the highly competitive and promotional holiday season. Our results continued to benefit from our ability to offer customers great values on a wide assortment of gifts and fashions for the family and the home.”

Ms. Rentler continued, “Fourth quarter operating margin grew 90 basis points to 13.6% up from 12.7% in the prior year. This improvement was mainly driven by our above-plan sales along with a favorable comparison of packaway-related costs versus last year’s fourth quarter. For the 2016 fiscal year, operating margin increased 40 basis points to a new record of 14.0%.”

Those are some solid numbers. Ross also approved a new two-year $1.75 billion share buyback program. At the current price, that’s about 6% of their outstanding shares.

Ross also bumped up their quarterly dividend from 13.5 to 16 cents per share. That’s an increase of 19%. The new dividend is payable on March 31 to stockholders of record as of March 10.

Now for guidance. Bear in mind that Ross tends to be very conservative with their forecasts. Ross projects full-year 2017 earnings between $3.02 and $3.15 per share. That’s up 7% to 11% over 2016. However, the current fiscal year is 53 weeks long. The company estimates that the extra week adds eight cents per share. Ross sees same-store growth this year of 1% to 2%.

For Q1, Ross forecasts earnings of 76 to 79 cents per share and comp store sales growth of 1% to 2%. The strikes me as very conservative.

The CEO said, “There continues to be uncertainty in the political, macro-economic, and retail climates, and we also face our own challenging sales and earnings comparisons. Thus, while we hope to do better, we believe it is prudent to remain somewhat cautious in planning our business for the 2017 fiscal year.”

-

Archives

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His