-

Verizon to Buy Yahoo

Posted by Eddy Elfenbein on July 24th, 2016 at 7:03 pmVerizon said it’s going to buy Yahoo’s core business for $4.8 billion. Yahoo will still have its investment in Alibaba, plus its patents.

Founded in 1994, Yahoo was one of the last independently operated pioneers of the web. Many of those groundbreaking companies, like the maker of the web browser Netscape, never made it to the end of the first dot-com boom.

But Yahoo, despite constant management turmoil, kept growing. Started as a directory of websites, the company was soon doing much more, offering searches, email, shopping and news. Those services, which were free to consumers, were supported by advertising displayed on its various pages.

For a long time, the model worked. It seemed like every company in America — and across much of the world — wanted to reach people using the new medium, and ad revenue poured in to Yahoo.

In the end, the company was done in by Google and Facebook, two younger behemoths that figured out that survival was a continuous process of reinvention and staying ahead of the next big thing. Yahoo, which flirted with buying both companies in their infancy, watched its fortunes sink as users moved on to apps and social networks.

I’ve often been critical of Yahoo as a potential investment. I don’t know how I can say it more plainly — the company simply isn’t that profitable.

While Google was singularly focused on search, Yahoo recast itself as a content company under its second chief executive, Terry Semel, who succeeded Timothy Koogle in 2001.

By the mid-2000s, Yahoo was struggling. Web portals, as they were called, were fading in importance, and social networks like Facebook were emerging as powerful competitors for people’s attention. Google had become the world’s dominant internet company through its search engine and its lucrative search ads.

In 2007, Mr. Semel was pressured to resign and Mr. Yang took over as chief executive. The next year, Mr. Yang rebuffed a $44.6 billion acquisition offer from Microsoft, infuriating many Yahoo shareholders.

If you were to turn back the clock to 1998, Yahoo was in a perfect position to own the Web. They had all the talent and all the smarts. They blew it.

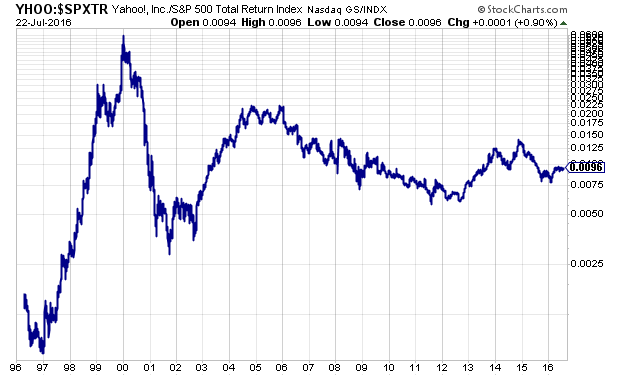

Here’s Yahoo divided by the S&P 500 Total Return Index. The stock has been in a long 16-year downtrend.

If Yahoo had merely kept pace with the S&P 500 Total Return Index, the stock would be at $244 today instead of $39.

-

CWS Market Review – July 22, 2016

Posted by Eddy Elfenbein on July 22nd, 2016 at 7:08 am“Every generation laughs at the old fashions, but follows religiously the new.”

– Henry David ThoreauFor the last several weeks, the market has been distracted by a flurry of distracting events, ranging from Turkey and Brexit to the Federal Reserve and oil prices, not to mention a soap opera-like election campaign. But now we’re at earnings season. This is what really counts.

So far, things are going well for our Buy List. We’ve had impressive earnings beats from stocks like Biogen (BIIB), Microsoft (MSFT) and Alliance Data Systems (ADS). Biogen creamed estimates, gave an optimistic forecast and jumped more than 7% (see below). Microsoft is cleaning up with its cloud business, and the stock just hit a new 52-week high. We’ve also had some disappointments from stocks like Signature Bank (SBNY).

In this week’s CWS Market Review, I’ll recap our earnings reports from this past week, plus I’ll highlight the ones coming our way next week. We have a lot of earnings reports to cover, so let’s get right to it.

Decent Earnings for WFC, Very Good Earnings for MSFT

Last Friday, Wells Fargo (WFC) kicked off earnings season for our Buy List by reporting Q2 earnings of $1.01 per share. That exactly matched Wall Street’s forecast. In last week’s issue, I said that Wall Street’s consensus “sounds about right.”

Obviously, an environment where interest rates stay low for longer is a tough one for any bank. Still, Wells is getting by quite nicely despite the challenges. Wells is a bit different from its mega-bank competitors because it’s more focused on consumers instead of Wall Street. That means it’s more susceptible to shifts in interest rates. The bank’s total loans are up 7.7% from a year ago. WFC’s net interest margin came in at 2.86%. That’s been in a downtrend for several quarters.

Shares of WFC dropped immediately after the earnings report but have regained much of that lost ground since then. There’s not much more to say about Wells, except that it’s a good bank operating in a difficult time for banks. I’m keeping my Buy Below at $52 per share.

On Tuesday, Microsoft (MSFT) gave us a very good earnings report. For its fiscal Q4, the software giant earned 69 cents per share. That was 11 cents better than estimates. I really like the way this company has turned itself around. I think traders completely overreacted to the slight earnings miss three months ago. I should add that according to Microsoft’s CFO, roughly six cents of the earnings surprise was due to a lower-than-expected tax rate.

Once again, we’re seeing that Microsoft’s cloud business is doing quite well. After several missteps, Microsoft is determined not to be left behind in this business space. Although the profit margins aren’t as generous, there are greater opportunities for growth. In a point of contract, Microsoft’s phone revenue is down 71% from a year ago. Thank you, Steve Ballmer.

Overall, I’ve been impressed by the way Satya Nadella has turned the ship around. The job isn’t done yet, but Microsoft is clearly moving in the right direction. The shares jumped more than 5% on Wednesday’s trading and touched a new 52-week high. The stock is even within striking distance of its all-time high ($59.97), set on the second-to-last day of the previous millennium. This week, I’m raising my Buy Below on Microsoft to $59 per share.

Medallion Loans Weigh on SBNY

Our first big earnings disappointment came on Wednesday when Signature Bank (SBNY) reported Q2 earnings of $1.90 per share. That was seven cents below estimates.

For one, Signature is dealing with the tough environment facing all banks. The other issue for them is their taxi medallion business. Thanks to Uber and others, the price for a taxi medallion has basically been cut in half. Signature’s been in the business of financing loans to buy these medallions. During Q1, the bank wrote off $4.4 million in bad medallion loans.

I’ll sum it up as succinctly as possible: Signature is doing fine. The basics of their business continue to do well. The medallion issue is a problem. But what’s particularly difficult is that we can’t say whether this issue has passed us just yet. We don’t know what we don’t know. Last quarter, Signature added $24 million in loan-loss reserves. Last quarter, the medallion loans made up 2% of all their loans. That’s down from 3% in Q1.

Shares of SBNY dropped sharply at Wednesday’s open. At one point, SBNY was below $120 per share, but the stock recovered throughout the day. By the closing bell, it had lost 4.5%. I’m not giving up on SBNY. I believe in their management and continue to see a bright future for them. This week, I’m lowering my Buy Below to $133 per share.

Very Impressive Earnings from ADS and Biogen

We had three more Buy List earnings reports on Thursday morning. First off, Alliance Data Systems (ADS) reported earnings of $3.68 per share. That beat Wall Street’s consensus by nine cents per share.

For Q3, ADS said they see earnings coming in at $4.42 per share. That’s below Wall Street’s consensus of $4.58. But the good news is that ADS sees full-year earnings coming in at $16.85 per share. Wall Street had been expecting $16.78 per share.

The activist fund, ValueAct Capital, recently announced that it has a sizable stake in ADS, and they’ve floated the idea of breaking the company up. I think it’s very possible that the component parts of an un-allied Alliance Data Systems could trade more than the current company.

This has been a tough year for ADS, so it was nice to see the stock pop 6.4% on Thursday. I’m going to cautiously bump up my Buy Below price for Alliance Data Systems to $237 per share.

Biogen (BIIB) became the star of the earnings season! The biotech company reported Q2 earnings of $5.21 per share. That beat estimates by 54 cents per share. The stock jumped 7.6% on Thursday. Biogen’s quarterly revenue rose 12% to $2.89 billion.

The company also announced a $5 billion share buyback, which it hopes to finish up within three years. Biogen also said that its CEO, George Scangos, will be stepping down. Scangos has done a fine job for shareholders, but I think it’s time for new leadership.

I was also pleased to see Biogen offer optimistic guidance for the rest of this year. The company sees revenue coming in between $11.2 and $11.4 billion. They see earnings-per-share ranging between $19.70 and $20. Wall Street had been expecting $18.96 per share.

Biogen has had a difficult year, so I’m glad to see it bounce back. I’ve been pretty conservative with my Buy Below price. This week, I’m going to raise our Buy Below on Biogen to $290 per share.

Snap-on (SNA) reported decent numbers, but traders weren’t impressed. No matter. I think the company is doing just fine. For Q2, Snap-on earned $2.36 per share which beat estimates by 13 cents per share.

One weak spot is that the company’s revenues fell below expectations. For Q2, SNA’s topline was $872.3 million. Wall Street had been expecting $876.9. The stock dropped 3.4% in Thursday’s trading. I’m not sure what caused the selloff, but it’s sometimes hard to divine the market’s wisdom, especially in the short term. Snap-on remains a good buy up to $166 per share.

After the closing bell on Thursday, Stryker (SYK) reported Q2 earnings of $1.39 per share which was two cents better than estimates. That’s up from $1.20 per share of last year’s Q2. The stock has been a huge winner for us this year.

For Q3, the medical-device company said it expects earnings to range between $1.33 and $1.38 per share. That’s a bit of a disappointment, as the Street had been expecting $1.41 per share. For all of 2016, Stryker now expects earnings to range between $5.70 and $5.80 per share. The previous range had been $5.65 to $5.80 per share.

The stock traded lower in the after-hours market, but that’s no guarantee of where the stock will open on Friday. I never understand why the market reacts negatively to a lower-than-expected quarterly outlook when it’s twinned with an improved full-year outlook, yet it happens all the time.

Nevertheless, Stryker is doing quite well. I’m afraid the U.S. dollar will be a headwind for the next few quarters. I’m keeping our Buy Below on Stryker at $122 per share.

Six More Earnings Reports Next Week

We have six more Buy List earnings reports for next week. Express Scripts and Wabtec report on Monday, July 25. CR Bard is due to report on Tuesday, July 26. Then on Thursday, July 28, AFLAC, Stericycle and Ford Motor are due to report. (In last week’s issue, I incorrectly said that Wabtec was due to report this week. WAB is reporting on Monday.)

In April, Express Scripts (ESRX) said it expects Q2 earnings to be between $1.55 to $1.59 per share. The pharmacy-benefits manager also increased its full-year range to $6.31 to $6.43 per share. The shares have been trending upward for several weeks.

Wabtec (WAB) had a very good earnings report in April, and the stock popped to a new high. Since then, however, it has been kind of a dud. On Thursday, shares of WAB settled at $70.40, which is over 18% below its April high.

I’m expecting another good earnings report. Wall Street expects $1.08 per share. The company also recently raised its modest dividend by 25%. The good news for us is that Wabtec has reaffirmed its full-year earnings of $4.30 to $4.50 per share.

CR Bard (BCR) was the big star of last earnings season. They beat and raised guidance. For Q2, Bard sees earnings coming in between $2.43 and $2.47 per share. For the entire year, they expect earnings to range between $10.05 and $10.18 per share. Be careful not to chase this one.

AFLAC (AFL) has been doing well for us lately. I’ll be curious to see how much the surging yen helps AFLAC’s bottom line. I think the company can earn as much as $6.60 per share this year in operating earnings. Even without the currency effect, the duck stock is a solid company.

I don’t understand why Ford Motor (F) is so cheap, but the market doesn’t always make perfect sense. The automaker now yields over 4.3%. The earnings report for Q1 was outstanding. For Q2, Wall Street expects earnings of 60 cents per share.

Stericycle (SRCL) had a disappointing earnings report three months ago. The company gave us full-year guidance of $4.90 to $5.06 per share. For Q2, Wall Street is expecting $1.18 per share.

That’s all for now. Stay tuned for a lot more earnings reports next week. We also have a Fed meeting on Tuesday and Wednesday. The policy statement is due out on Wednesday afternoon. I’m not expecting any rate change, but the odds of at least one rate hike before the end of the year are growing. They’re still not high, but they are growing. We’ll also get our first look at the Q2 GDP report next Friday. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: July 22, 2016

Posted by Eddy Elfenbein on July 22nd, 2016 at 7:03 amU.K. Chancellor Ready to ‘Reset’ Fiscal Policy on Brexit

Britain’s Economy Wilting Fast After Brexit Vote, May Prompt More Spending

Pointing a Finger at the Fed in the Lehman Disaster

Oil Prices Fall on Glut in Refined Products

Fracklog in the Biggest U.S. Oil Field May All But Disappear

Roger Ailes’ Unparalleled Impact On The Public Sphere

Amazon Is Now Offering Discounted Student Loans as a Prime Perk

FDA Raises Concerns Over Valeant’s Eye Drop

Syngenta Says U.S. Talks Over ChemChina Bid ‘Constructive’

Boeing Sees $2.1 Billion Cost on 787 Dreamliners, Air Tanker

McDonald’s Stops Selling Big Mac in Venezuela Due to Bread Shortage

Schlumberger Posts a Loss as Job Cuts Deepen

Spotify Ramps Up Its Audio Ad Business as It Prepares for Its IPO

Roger Nusbaum: Deploying Cash When the Market Is At All-Time Highs

Cullen Roche: Revisiting My “Useless” 2016 Predictions

Be sure to follow me on Twitter.

-

Three More Earnings Beats

Posted by Eddy Elfenbein on July 21st, 2016 at 9:00 amWe had three more Buy List earnings beats this morning.

Biogen (BIIB) reported earnings of $5.21 per share. They beat estimates by 54 cents per share. The company also announced a $5 billion buyback. Quarterly revenues rose 11.7% to $2.89 billion. Biogen’s CEO, George Scangos, said he’ll be stepping down.

Biogen said they expect full-year earnings to range between $19.70 and $20 per share. Wall Street had been expecting $18.96 per share.

Snap-on (SNA) reported Q2 earnings of $2.36 per share. Wall Street had been expecting $2.23 per share.

Alliance Data Systems (ADS) earned $3.68 per share which was nine cents more than expectations. The company now expects Q3 earnings of $4.42 per share and full-year earnings of $16.85 per share. -

Morning News: July 21, 2016

Posted by Eddy Elfenbein on July 21st, 2016 at 7:18 amKuroda Says No Need and No Possibility for Helicopter Money

Investors Think the Bank of Japan Will Pull the Trigger Next Week

US Treasury Chief Stresses Need for Greek Debt Relief

Here’s How the World’s Biggest Beer Merger Won U.S. Antritrust Approval

Komatsu Signals Mining Optimism With $2.9 Billion Joy Takeover

HSBC Top Manager Arrested Over Foreign Exchange Fraud Claims

Roger Ailes’s Exit Is Unlikely to Erode the Fox News Citadel

Southwest Airlines’ Profit Misses Estimates as Fares Decline

Dish Network Tops Profit Views, Loses Subscribers

Pairing New Cancer Drugs With Older Ones Bolsters Roche Profit

Daimler Posts Slight Growth in Profit

AmEx Profit Rises on Gain Tied to Costco Portfolio Sale

Josh Brown: Peter Boockvar: And Now, Everyone Is Bullish

Howard Lindzon: The S&P is at All-Time Highs …Today is a Better day to Panic

Be sure to follow me on Twitter.

-

Signature Bank Earns $1.90 per Share

Posted by Eddy Elfenbein on July 20th, 2016 at 10:18 amShares of Signature Bank (SBNY) are down about 7% this morning. The bank reported Q2 earnings of $1.90 per share which was eight cents below expectations. Their net interest margin for Q2 was 3.18%.

“There are many uncertainties in the current global environment – political, economic and regulatory, among others. However, the one constant is our conviction to depositor safety. In times of turmoil, volatility and market disruption, we rely on the strength and success of Signature Bank’s highly focused depositor-first model to sustain our growth. This deposit first-and-foremost strategy continues to allow us to not only weather storms, but also to seize opportunities arising from changing market conditions,” explained Joseph J. DePaolo, Signature Bank President and Chief Executive Officer.

(…)

Non-interest income for the 2016 second quarter was $13.1 million, up $3.4 million when compared with $9.8 million reported in the 2015 second quarter. The increase was due to a $4.4 million increase in net gains on sales of securities.

Non-interest expense for the second quarter of 2016 was $92.3 million, an increase of $7.4 million, or 8.7 percent, versus $84.9 million reported in the 2015 second quarter. The increase was primarily a result of the addition of new private client banking teams, as well as an increase in costs in our risk management and compliance related activities.

-

Morning News: July 20, 2016

Posted by Eddy Elfenbein on July 20th, 2016 at 7:18 amU.S. Targets $1 Billion in Assets in Malaysian Embezzlement Case

Justice Dept. Will Seek to Block Two Health Insurance Mergers

Roger Ailes is Negotiating His Departure as Chairman of Fox News

Pimco’s New Turnaround Man: Manny Roman

For Berkshire Hathaway’s Latest Multibillion-Dollar Deal, Warren Buffett Goes Back to Insurance

Unilever Buys Dollar Shave Club for $1 Billion

United Profit Exceeds Analysts’ Estimates on Cost Reductions

Discover Financial Loans Rise 4%

BHP Says 2017 Iron Ore Output May Be Flat, Cuts Oil Spending

EMC Shareholders Voted to Approve the Multi-Billion Dollar Merger With Dell

Inside the High-Profile Downfall of a $8 Billion Hedge Fund

Hyperloop One Files $250 Million Countersuit In Response To ‘Failed Takeover Attempt’

Jeff Carter: Financial Statements and Valuation

Roger Nusbaum: So Now Brexit Is Good For Markets?

Be sure to follow me on Twitter.

-

Microsoft Earns 69 Cents per Share

Posted by Eddy Elfenbein on July 19th, 2016 at 8:34 pmA very good earnings report from Microsoft (MSFT). The software giant earned 69 cents per share which was 11 cents better than expectations.

Microsoft Corp. remains a distant second to Amazon.com Inc. in cloud computing, but the software giant’s latest quarterly results suggest that it is effectively managing the transition from selling software licenses to selling on-demand computing services.

In its fiscal fourth quarter, sales of the Redmond, Wash., company’s Azure cloud computing service more than doubled, offsetting a decline in the segment that includes its flagship Windows operating system and its struggling mobile-phone business.

The strength of Microsoft’s cloud business surprised investors. The company beat expectations for both sales and profit, which spurred a 4% rise in Microsoft’s shares in after-hours trading.

Microsoft has proved especially adept at selling its cloud services to existing customers, taking advantage of longstanding relationships with companies that have run its software in their own data centers.

“They are effectively getting their customers to transition to the cloud,” Stifel Nicolaus & Co. analyst Brad Reback said.

Microsoft’s transition to the cloud comes with an important cost: eroded margins. When the company relied on software licenses sold to companies every few years, it registered fat profits. But margins on cloud services, which are sold by subscription, are slimmer.

For the quarter, gross margins slid 14% to $12.64 billion.

The stock was up 4.2% in after hours trading.

-

Morning News: July 19, 2016

Posted by Eddy Elfenbein on July 19th, 2016 at 7:06 amCrude Oil: Is A Gasoline Glut Emerging?

German ZEW Investor Sentiment Deteriorates in Brexit Aftermath

EU to Fine Truck Makers Over Price-Fixing and Other Collusion

SoftBank’s Quest for ARM Spanned Turkish Coast to No. 10 Downing Street

D.C. Decision, Expected In Fall, Could Reverse CFPB’s Actions, Change Structure

Yahoo Revenue Falls 15% and Profit Drops 64%Thanks to Pokémon Go, Nintendo’s Market Cap Just Doubled to $42 Billion

Investor Challenges Baidu on Sale of Video Service to CEO

UnitedHealth Profit Beats on Optum Unit Strength

Wal-Mart Escalates Fight With Visa, Blocks Cards at Three Canadian Stores

Monsanto and Bayer Move Closer to a Deal

Novartis Says Profit Could Dip as It Boosts Investment in Heart Drug Entresto

Netflix Disappoints Wall Street as Subscriber Growth Slows

Josh Brown: Middle Out Compression

Cullen Roche: There Are No “Bond Kings” in This Bond Market

Be sure to follow me on Twitter.

-

On Vacation

Posted by Eddy Elfenbein on July 18th, 2016 at 3:47 pmI’m relaxing in Canada this week so posting will be light. We have a busy week for Buy List earnings, so I’ll provide updates for those.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His