-

CWS Market Review – January 30, 2015

Posted by Eddy Elfenbein on January 30th, 2015 at 7:08 am“Go for a business that any idiot can run—because sooner or later, any idiot probably is going to run it.” – Peter Lynch

The strong U.S. dollar is finally making its presence felt on the income statement. So far, the reported earnings for our Buy List stocks have been quite good. However, this week, two of our big-name tech stocks, Qualcomm ($QCOM) and Microsoft ($MSFT), got pinged for big losses as their outlooks weren’t as rosy as Wall Street had hoped they’d be. In both cases, the rising dollar has taken a bite out of earnings, and they’re not alone. I’ll have more details on those two in a bit.

Overall, earnings season is going OK, but not great; 77% of the companies that have reported have topped earnings expectations. Of course, we have to remember that estimates for Q4 were pared back a lot in the last several weeks. Looking at the top line, 58% of the earnings results so far have beaten their sales expectations. Right now, it looks like earnings are growing, but at a very subdued pace.

But the real drama continues to be in the forex and bond markets. This week, the Federal Reserve said it was going to be “patient” in its desire to raise short-term interest rates. The bond market took the clue, and the yield on the 30-year Treasury plunged below 2.8% to its lowest yield ever (see above). The dollar seems unstoppable, and I think the euro and the dollar could soon reach parity for the first time in 12 years.

In this week’s CWS Market Review, I’ll tell you what the Fed’s “patience” means for us and our portfolios. I’ll also go over our recent earnings reports. Despite the bad news from Qualcomm and Microsoft, we had some solid results as well—CR Bard just capped off an outstanding year. Later on, I’ll preview the five earnings reports we have next week. (You can see our complete Earnings Calendar.) But first, let’s look at why the Fed may not be touching interest rates at all this year.

The Federal Reserve Says “It Can Be Patient”

The Federal Reserve met again this week and on Wednesday afternoon, the central bank released its latest policy statement. The Fedspeak was largely the same as the one from December, but they added several optimistic edits. In fact, it was probably the Fed’s most cheerful outlook for the economy in years. (Central bankers are rarely optimistic.) It’s taken a while, but things are clearly improving. The fewest number of Americans filed for first-time jobless claims in nearly 15 years.

For the last several months, the Fed has hinted that short-term rates will start to rise sometime in the middle of this year. Gradually, I’ve grown to doubt that timetable. Now it appears that the Fed and the bond market are catching on. I think it’s now very possible that we won’t see a rate increase until 2016. In fact, Morgan Stanley just pushed their expectations for a rate hike to Q1 of next year. Of course, even when rates do rise, they will still be well below the rate of inflation.

The key sentence in the Fed’s policy statement read: “Based on its current assessment, the Committee judges that it can be patient in beginning to normalize the stance of monetary policy.” That’s about as exciting as central bankers get, but the message is clear: Until wages pick up, the Fed simply isn’t going to do much of anything.

What does the continuation of low rates mean? It’s very good for stock investors. If rates are going to stay low, even modest dividend yields of 2% or 3% are very inviting. It’s simple math. Ford Motor ($F), for example, recently raised its dividend by 20%. The automaker currently yields 4%, which beats most anything you’ll find in the bond market. (I’ll have more on Ford’s earnings in just a bit.)

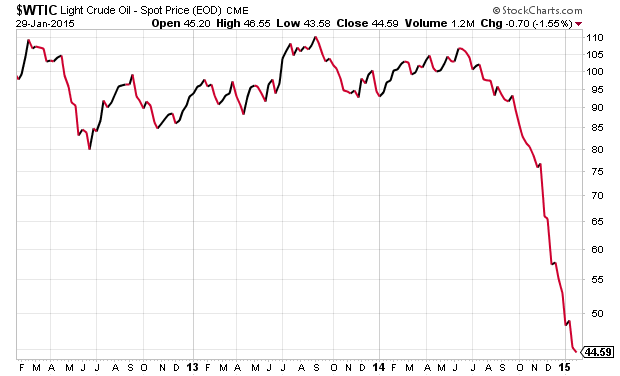

This entire dynamic is due to the Strong Dollar Trade. Actually, the dollar got even stronger against the euro after the left-wing Syriza party won in Greece. The rising dollar has put the squeeze on commodity prices. This means that right now, we’re experiencing deflation. On Monday, gasoline prices rose for the first time in 123 days. That won’t last long. Last month, U.S. oil inventories rose to their highest level for December since 1930. On Thursday, West Texas Crude briefly dropped below $44 per barrel. A lot of Energy and Materials stocks are in rough shape.

Wall Street had been expecting the dollar to take a bite out of Q4 earnings, but I think they were surprised by how large the impact was. In October, Wall Street expected the S&P 500 to post Q4 earnings growth of 8.5%. That’s now down to 1.1%. The strong dollar is having its greatest impact on U.S. manufacturing. We can see evidence of that in the last two durable-goods reports, which were quite weak.

Firms are already cutting back on capital spending. Caterpillar ($CAT), for example, which is a Dow component, said they’re cutting their spending plans. Even consumer-products companies are feeling the heat. Procter & Gamble ($PG) said the strong dollar could reduce their earnings this year by $1.4 billion; nearly half of that is due to the Russian ruble. I also suspect that a lot of companies are jumping in on the strong-dollar excuse so they can temper expectations for the rest of this year. Now let’s take a look at some of our Buy List earnings reports from this week.

Our Recent Buy List Earnings Reports

For the most part, our Buy List stocks have reported good earnings, but the market hasn’t always reacted positively. On Monday, Microsoft ($MSFT) reported Q4 earnings of 71 cents per share. That exactly matched Wall Street’s estimates, but the stock dropped more than 9% on Tuesday.

The problem was their forecast for the rest of this year (Microsoft’s fiscal year ends in June). PC sales have been somewhat sluggish, and Microsoft’s commercial software was surprisingly weak. That had been a recent bright spot for the software giant. Microsoft also cited—I hope you’re sitting down—the recent strength of the U.S. dollar as a negative factor. They said currency exchange will lower revenues by 4% this quarter. The company said they were expecting sales declines in China, Russia and Japan.

While this news is disappointing, most of the key factors such as currency and geopolitics are outside of MSFT’s control. I like Microsoft a lot, and I think Nadella has done a commendable job. To adjust for this week’s pullback, I’m lowering my Buy Below on Microsoft to $45 per share.

Our other tech dud was Qualcomm ($QCOM). But like Microsoft, the results were quite good. For Q4, Qualcomm earned $1.34 per share for Q4, which topped estimates by nine cents per share.

The problem was guidance. Qualcomm had previously said to expect full-year 2015 results of $5.35 per share. Now they say it will range between $4.75 and $5.05 per share. Sales will range from $26 billion to $28 billion. On Thursday, the shares dropped 10.3% to close at $63.69. Ouch!

Qualcomm said that a major customer decided against using their Snapdragon chip in a flagship phone design. The company has long had the field to themselves, and they’re starting to face some competition. I have faith in CEO Steve Mollenkopf and his team. Qualcomm is still a good buy, but I’m lowering my Buy Below to $66 per share.

On Tuesday, Stryker ($SYK) reported Q4 earnings of $1.44 per share. That was one penny below expectations. For all of 2014, the company made $4.73 per share.

For Q1, Stryker expects earnings to range between $1.05 and $1.10 per share; for the entire year, they see earnings coming in between $4.90 and $5.10 per share. Wall Street had been expecting $1.17 per share for Q1 and $5.14 per share for the whole year.

Shares of Stryker actually climbed on the light guidance. I think investors understood that aside from the dollar, Stryker’s business is going quite well. This is a good stock. Stryker remains a buy up to $98 per share. I think it’s very likely that Stryker will do a big deal this year.

CR Bard ($BCR) continues to be one of our brightest stocks. This week, the medical-devices company reported Q4 earnings of $2.29 per share. That was five cents better than estimates. Sales rose to $867.2 million, which beat expectations by $9.5 million.

CEO Timothy M. Ring said, “Two years ago we announced a strategic investment plan with the objective to shift the mix of the portfolio to faster growth through investments in emerging markets and new product development. We said at the time that we expected the early returns from those investments to begin in the back half of 2014. We are pleased with the performance of our investment plan so far, as we delivered accelerating organic revenue growth throughout 2014. We remain focused on executing our plan with the objective of improving the long-term growth profile of the company in a profitable manner that adds value for shareholders.”

For all of 2014, Bard earned $8.40 per share. That’s a very nice increase from $5.78 per share in 2013. The stock has doubled for us in just over three years. This week, I’m raising my Buy Below on CR Bard to $184 per share.

Last week, I said not to place too much emphasis on Ford Motor’s ($F) Q4 earnings report. The results later this year will be far more important, but Ford had a decent Q4. They earned 26 cents per share, which beat estimates by three cents per share.

Ford’s core business continues to be trucks sold in North America, and that’s going well. The bad news for Ford is Europe, which appeared to be improving. Ford is turning things around in the Old World, but not as quickly as they had expected.

The most important news for us is that Ford is sticking by its 2015 forecast for a pretax profit between $8.5 billion and $9.5 billion. That’s very good news. Until now, I’ve kept a wide range for our Buy Below price, but I want to tighten that a little bit. This week, I’m lowering my Buy Below on Ford to $16 per share, but this is in no sense a downgrade.

Next Week’s Buy List Earnings Reports

We have five more earnings reports due next week. On Tuesday, AFLAC and Fiserv will report. Cognizant Technology Solutions follows on Wednesday. Then two of our new stocks, Ball Corp. and Snap-on, will report on Thursday. As always, check the blog for the latest updates.

AFLAC ($AFL) has been one of our more frustrating stocks because the company has done very well from a standpoint of operations. It’s an efficient and well-run company. However, their financial results have been greatly impacted by the sinking yen. AFLAC does a ton of business in Japan, and the government there has been trying to bring down its currency relative to the U.S. dollar. That means that AFLAC’s profits get stung when the money is translated from yen into dollars.

In October, AFLAC said it was expecting Q4 operating earnings to range between $1.28 and $1.37 per share. But that was assuming the yen stayed between 105 and 110 to the dollar. It’s currently at 118.23. For 2015, AFLAC aims to increase their operating earnings by 2% to 7% on a currency-neutral basis.

Three months ago, Fiserv ($FISV) raised their expectations for Q4. They now see quarterly earnings between 86 and 90 cents per share. That means full-year 2014 earnings of $3.34 to $3.38 per share, up from $2.99 per share for 2013. The shares hit another new all-time high this week. I’ll be curious to see if they provide guidance for 2015. Fiserv is one of my favorite long-term holdings.

Cognizant Technology Solutions ($CTSH) had an outstanding earnings season three months ago. From October 20 to November 7, the shares rallied 23%. The IT outsourcer raked in 66 cents per share for Q3, which was seven cents better than estimates. Quarterly revenues jumped 11.9% to $2.58 billion.

For Q4, Cognizant sees earnings of at least 63 cents per share. Wall Street had only been expecting 59 cents per share. That would bring full-year earnings to at least $2.57 per share. CTSH also said they expect revenues to range between $2.61 and $2.64 billion. That was above the Street’s forecast of $2.59 billion. Last Friday, the shares hit an all-time high of $56.62 per share.

Ball Corp. ($BLL) is a brand-new member of our Buy List. The company is the largest producer of recyclable beverage cans in the world. Ball also has an aerospace unit that makes parts for NASA. They’re somewhat boring, but very profitable. Ball has beaten earnings for the last five quarters in a row. Wall Street currently expect 85 cents per share for Q4.

Snap-on ($SNA) is another new stock for us. They’re a maker of high-end hand and power tools. They also make lots of machines for car repair, like hydraulic lifts and tire changers. Snap-on makes products for the marine, rail and aviation industries. In November, Snap-on raised their dividend by 20.5%. Wall Street’s consensus for Q4 is $1.81 per share.

That’s all for now; there are still more earnings reports to come next week. On Monday, we’ll get the ISM report for January. On Tuesday, the report on factory orders comes out. This leads up to the big January jobs report on Friday morning. The unemployment rate for December was 5.6%, which is a six-year low. The number for January may be even lower. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: January 30, 2015

Posted by Eddy Elfenbein on January 30th, 2015 at 7:03 amRussia Unexpectedly Cuts Key Rate as Economy Eclipses Ruble

Russian Banks Rush to Rescue Credit-Starved Large Corporates

Spain Grows at Fastest Rate in Seven Years

China In New Steps Against Foreign Tech

Intuit Cries Uncle, Will Reverse TurboTax Deluxe Changes

Apple’s Shares Should Continue To Rise

Amazon Shares Jump as Earnings Top Expectations

Dealing With Recalls, Honda Cuts Profit Forecast for the Year

Lilly Lowers 2015 Revenue Forecast Citing Strong U.S. Dollar

Google Revenue Hurt by Rising Dollar

Qatar Airways Takes $1.7 Billion Stake in British Airways-Owner IAG

Shake Shack, Born in a Park, Is Going Public With Big Dreams

Roger Nusbaum: The Benefits of Proper Risk Budgeting

Joshua Brown: The First Casualty of a Bear Market

Be sure to follow me on Twitter.

-

30-Year Yield Off All-Time Low

Posted by Eddy Elfenbein on January 29th, 2015 at 2:21 pmAfter yesterday’s Fed meeting, the yield on the 30-year Treasury dropped down to 2.29%. That’s the lowest since the Treasury started issuing 30-year bonds in 1977.

Today, it’s risen a bit to 2.34%.

-

Initial Jobless Claims at 15-Year Low

Posted by Eddy Elfenbein on January 29th, 2015 at 2:17 pmThis morning we learned that initial jobless claims dropped to 265,000 last week. That’s the lowest figure since April 15, 2000. It’s also the second-lowest report since December 1, 1973. That means we just had one of the strongest jobs reports in 41 years,

Now I should caution that the jobless claims report tends to be very “noisy,” meaning it bounces around a lot. That’s why it’s important to focus on the larger trend rather than the last one or two data points. Still, the longer trend has been quite impressive, and looks ready to continue.

-

Morning News: January 29, 2015

Posted by Eddy Elfenbein on January 29th, 2015 at 7:10 amCarney Says ECB QE Not Enough Without Fiscal Support

Fed Upbeat on U.S. Economy, Cites Strong Job Gains

Ford Fourth-Quarter Profit Slumps 98%

The One Missing Ingredient In Facebook’s All-Out Drive For TV Ad Dollars

McDonald’s Promotes Easterbrook to Supersize His U.K. Success

Alibaba Holiday-Quarter Revenue Disappoints

Time Warner Cable Gains Subscribers; Results Miss

Potash Corp’s Profit Beats as Potash Sales Rise, Costs Fall

Thermo Fisher Fourth-Quarter Results Top Expectations on Life Tech Buy

Boeing Says Dreamliner to Yield More Cash in ’15

Shell to Cut Spending by $15 Billion Over Three Years

Nokia’s Network Unit Beats on North America Growth

Diageo Reports Better Quarter But US And China Still Drag

Cullen Roche: The Fed’s “Crazy Train” and the Stability that Breeds Instability

Jeff Carter: Great Advice For Entrepreneurs (and Investors)

Be sure to follow me on Twitter.

-

Qualcomm Had Good Earnings But Poor Guidance

Posted by Eddy Elfenbein on January 28th, 2015 at 9:15 pmAfter the bell, Qualcomm ($QCOM) reported Q4 earnings of $1.34 per share which was nine cents better than estimates.

Underlining the strength of broader phone demand, and illustrating how much most phone makers still depend on its chips, Qualcomm topped estimates for fiscal first-quarter profit and gave a rosy forecast for the current period.

A record quarter for Apple Inc.’s iPhone, which uses a Qualcomm modem chip, helped the chipmaker’s earnings. For the period ended Dec. 28, Qualcomm’s net income rose to $1.97 billion, or $1.17 a share, from $1.88 billion, or $1.09, a year earlier. Sales rose 7.2 percent to $7.1 billion. Excluding certain costs, profit was $1.34 a share. Analysts on average had projected profit of $1.25 a share on sales of $6.94 billion.

Profit before some items in the second quarter, which ends in March, will be $1.28 to $1.40 a share, the company said Wednesday. Sales will be $6.5 billion to $7.1 billion. On average, analysts projected profit of $1.28 a share and revenue of $6.72 billion, according to data compiled by Bloomberg.

The problem is that the company lowered their full-year guidance:

Sales for fiscal 2015 will be $26 billion to $28 billion, the San Diego-based company said in a statement. Profit excluding certain costs for the year will be $4.75 to $5.05 a share. The company previously projected as much as $28.8 billion in revenue and $5.35 in per-share profit.

The stock fell 8.3% in the after-hours market.

-

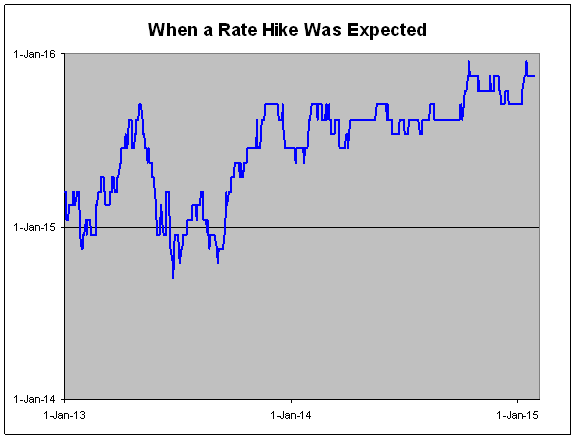

What Does the Futures Market Expect and When Does it Expect it?

Posted by Eddy Elfenbein on January 28th, 2015 at 2:55 pmAs readers of my blog know, I’m a big fan of Bespoke Investment Group. They always have great research and info. Lately, Bespoke has been running a “Countdown to Liftoff” chart. This is based on Fed Funds futures and it shows how much time the futures market thinks there is between now and the first Fed rate hike.

I suggested slightly altering the chart to show the y-axis as a date. Bespoke was good enough to pass along their data, so here’s what the chart looks like.

This chart may look a bit off at first because both axes are dates, but bear with me. The x-axis shows the date. The y-axis indicates when people thought the first rate hike was coming.

Starting in the fourth quarter of 2013, the market was expecting the first rate hike by mid-2015. In March 2014, Yellen sent the market into a tizzy with her “something on the order of six months” remark, referring to the period between the end of QE and the first rate increase.

That remained the case all the way through September of last year when August 2015 was seen as I-Day. Lately, however, the first rate hike expectation is beginning to drift back. The market currently sees a rate hike in November 2015. After today’s Fed news, I think we’re soon going to see the futures market point to 2016.

-

Today’s Fed Statement

Posted by Eddy Elfenbein on January 28th, 2015 at 2:02 pmHere’s today’s Fed statement:

Information received since the Federal Open Market Committee met in December suggests that economic activity has been expanding at a solid pace. Labor market conditions have improved further, with strong job gains and a lower unemployment rate. On balance, a range of labor market indicators suggests that underutilization of labor resources continues to diminish. Household spending is rising moderately; recent declines in energy prices have boosted household purchasing power. Business fixed investment is advancing, while the recovery in the housing sector remains slow. Inflation has declined further below the Committee’s longer-run objective, largely reflecting declines in energy prices. Market-based measures of inflation compensation have declined substantially in recent months; survey-based measures of longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace, with labor market indicators continuing to move toward levels the Committee judges consistent with its dual mandate. The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced. Inflation is anticipated to decline further in the near term, but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of lower energy prices and other factors dissipate. The Committee continues to monitor inflation developments closely.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate. In determining how long to maintain this target range, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. Based on its current assessment, the Committee judges that it can be patient in beginning to normalize the stance of monetary policy. However, if incoming information indicates faster progress toward the Committee’s employment and inflation objectives than the Committee now expects, then increases in the target range for the federal funds rate are likely to occur sooner than currently anticipated. Conversely, if progress proves slower than expected, then increases in the target range are likely to occur later than currently anticipated.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Jeffrey M. Lacker; Dennis P. Lockhart; Jerome H. Powell; Daniel K. Tarullo; and John C. Williams.

-

Morning News: January 28, 2015

Posted by Eddy Elfenbein on January 28th, 2015 at 7:05 amGerman Consumer Sentiment to Reach 13-Year High in February

China Accuses Alibaba Of Lax Merchant Control, Tells It To Stop Being Arrogant

Alibaba Creates a Consumer Credit Rating Service

London’s Canary Wharf: Qatar Bid Wins Battle

Consumer Confidence in U.S. Rises More Than Forecast on Jobs

Morgan Stanley: The Fed Isn’t Raising Rates Until March 2016

Obama Proposes Offshore Drilling From Virginia to Georgia

Apple Smashes Forecasts, Selling 74.5 Million iPhones In Q1

TE Connectivity to Sell Broadband Network Unit to CommScope

Nintendo’s Outlook Disappoints and Mario Can’t Save Wii U

Roche Earnings Stagnate for First Time in Three Years on Costs

H&M Posts Rise in Quarterly Profit, Plans 400 New Stores

In DuPont Fight, Activist Investor Picks a Strong Target

Ben Carlson: Would Keynes Have Been Fired As a Money Manager Today?

Roger Nusbaum: 11 Investing and Personal Finance Hacks

Be sure to follow me on Twitter.

-

Stryker Earns $1.44 per Share

Posted by Eddy Elfenbein on January 27th, 2015 at 4:14 pmStryker ($SYK) just reported Q4 earnings of $1.44 per share. That was one penny below expectations. For all of 2014, the company made $4.73 per share. Here’s the outlook for 2015:

We expect 2015 constant currency sales growth in the range of 5.5% to 7.0%, including organic sales growth in the range of 4.5% to 6.0%. Based on current foreign currency exchange rates we expect adjusted diluted net earnings per share to be in the range of $1.05-$1.10 and $4.90-$5.10 in the first quarter and the full year, respectively. If foreign currency exchange rates hold near current levels, we expect sales in the first quarter and full year of 2015 to be negatively impacted by approximately 3% to 4% and adjusted diluted net earnings per share to be negatively impacted by approximately $0.08 and $0.30 in the first quarter and the full year, respectively.

Wall Street had been expecting $1.17 per share for Q1, and $5.14 for the whole year.

Shorter version: Business is going well but the strong dollar is causing some pain.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His