-

Competition and Monopolies

Posted by Eddy Elfenbein on October 21st, 2014 at 2:51 pmLast month, Peter Thiel wrote a provocatively-titled op-ed for the Wall Street Journal, “Competition is for Losers.” In it, Thiel says that textbooks are all wrong: capitalism has little interest in competition. Rather, capitalism wants monopolies—and this, Thiel claims, is a good thing. He highlights Google as an example of a company that dominates search but uses its vast monopoly profits to fund dozens of worthy enterprises.

I think Thiel is onto something-mostly-but I have some notes of caution. For example, his use of the word monopoly is unconventional. Thiel isn’t referring to the strict legal definition of a monopoly but to a company that has little to no real competition. I also think his description of non-monopolies is unduly bleak, as if these are starving castaways fighting over scraps of meat.

But it’s an interesting topic. Consider: Is Harley-Davidson a monopoly? Well, in the legal sense, of course not. There are lots of motorcycle companies. Yet Harley is a brand so differentiated that it can be thought of as a pseudo-monopoly. Harley buyers would never view their hogs as just another bike. Harley is quite aware of this (a good portion of their revenue is apparel).

Thiel says that true differentiation is often claimed but rarely achieved. I’m not so sure about that. I think I differ from him in that I believe high-efficiency can be enough to differentiate an enterprise. There are some companies that follow the message of the old country song, “Do What You Do Do Well.” But we agree that firms desire to avoid competition, and this can be done by separating themselves from everyone else.

Thiel likes creative monopolies and he gives the example of Apple, but he also lists companies like the old AT&T and IBM in the 1960s, two companies which are no longer monopolies. The idea of a former monopoly should be a contradiction, but it happens quite frequently. Indeed, Thiel writes, “the history of progress is a history of better monopoly businesses replacing incumbents.” I have to agree.

A few months ago, I wrote about competitive advantage, an important topic that’s often discussed incorrectly:

Ideally, you want to have a business with high barriers to entry and low barriers to exit, and you want to differentiate yourself with whatever it is you do. You can do that by exclusivity or by price. That’s your competitive advantage. Once you get that, then you get better managers, better advertising and a stronger brand name. But it starts with a competitive advantage.

I think people often have difficulty with the concept of competitive advantage because they want to see sinister forces at work. And make no mistake: I do believe the tempering forces of free enterprise can sometimes break down and give a particular firm a lasting advantage that has nothing to do with its own inherent merit. It could be that they were in the right place at the right time.

For example, many years ago, the Japanese government gave AFLAC a monopoly on selling cancer insurance, and this translates into a huge market share today. Naturally, this is unsettling to those of us raised on the idea that the world wants a better mousetrap. But the truth is, it doesn’t. It wants the one it’s heard of. Just like in politics, the incumbent holds a lot of power.

-

S&P 500 Breaks Above 200-DMA

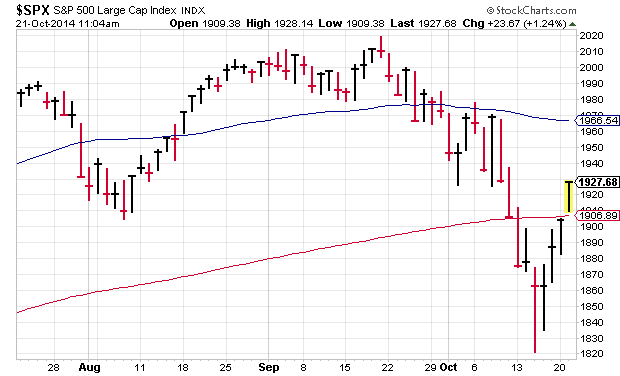

Posted by Eddy Elfenbein on October 21st, 2014 at 11:07 amThe S&P 500 is now back above its 200-DMA, though it’s still short of its 50-DMA. This doesn’t necessarily mean the storm has passed, but the bulls aren’t going down without a fight.

-

The Bounce Back

Posted by Eddy Elfenbein on October 21st, 2014 at 10:52 amThe S&P 500 is up to 1,927 this morning. The index has gained more than 100 points since last Wednesday. It’s interesting that the market has rallied strongly over the past four days yet many investors are wondering how much more we’re going to fall.

The S&P 500 also broke above its 200-DMA. Right as people start debating the correction is often when it’s already over. The Volatility Index is down to 16.80. Last Wednesday, it was at 31.

-

The Panic of 1907

Posted by Eddy Elfenbein on October 21st, 2014 at 9:32 amToday marks the 107th anniversary of the start of the Panic of 1907. Gary Alexander of Navellier Marketmail describes the tumultuous week:

This Week in History: The Panic of 1907

Here’s a day-by-day rundown of the week that made Mark Twain’s “October” prediction come true:

On Monday, October 21, 1907, depositors staged a run on Knickerbocker Trust Company, the third-largest mega-bank in New York City. John Steele Gordon wrote (in “The Great Game: The Emergence of Wall Street”), “Bedlam reigned as depositors fought to get to a teller and withdraw their assets from the bank’s imposing new headquarters on Fifth Avenue.” No luck. “The bank closed the next day after an auditor found that its funds were depleted beyond hope. The bank’s president, Charles Barney, shot himself several weeks later, prompting some of the bank’s outstanding depositors to commit suicide.”

On Tuesday, October 22, the president of Knickerbocker Trust Company bravely opened the doors of his troubled bank, but that was not a wise move. Within hours, depositors had withdrawn $8 million. By afternoon, Knickerbocker Trust Company announced its insolvency and closed its doors for good.

On October 23, lower Manhattan streets were choked with anxious bank depositors lined up in front of even the soundest of banks. On this day, the Trust Company of America looked suspect. By 1:00 p.m., they had only $1.2 million in cash on hand. By 1:20, it was down to $800,000. By 1:45, they had $500,000 and at 2:15 they were down to $180,000. About then, bank president Oakleigh Thorne (what a great name!) rushed over to J.P. Morgan’s office for help. When Morgan was convinced that the Trust Company was otherwise sound, he said, “Then this is the place to stop the trouble,” and he transferred enough cash to tide the bank over for the rest of the day. Morgan deposited roughly $30 million in major New York banks and told those banks to lend the money out to instill confidence among depositors.

On October 24, New York Stock Exchange (NYSE) officials came to Morgan and said, in effect, “Please make enough cash available to our brokers to meet their obligations or we will close the stock exchange.” Morgan called all the major bankers to his office. Within five minutes, he raised $27 million. Then, he said that any bears would be “dealt with.” That night, he called every important banker in the city to his private library on East 36th Street. After hours of indecision, the bankers came up with a plan to use clearinghouse certificates instead of cash to settle the transactions. The effect was to increase the money supply by a then-huge $84 million. As quickly as that, the Panic of 1907 was over.

On October 25, markets were back in good order, after Morgan’s defining moment. Hs partners compared Morgan’s rescue efforts to great generalship in a war. Even President Theodore Roosevelt, who railed against “the malefactors of great wealth” during the early months of 1907, said, “Those substantial businessmen acted with wisdom and public spirit.” But Morgan was 68 and in bad health. He didn’t want to do this again. He argued that Washington, DC should handle the next panic…and so the Fed was born.

P.S. The Dow Jones index kept falling, reaching a low of 38.83 on November 15, 1907, a 48.5% decline from 75.45 at the beginning of 1906. But the Dow almost fully recovered by late 1909, peaking at 73.64.

-

Morning News: October 21, 2014

Posted by Eddy Elfenbein on October 21st, 2014 at 6:54 amUK Government Borrowing Rises: What The Economists Say

Triple Whammy Looms for China’s Oil Refiners as Crude Plunges

China Posts Slowest Growth Since Global Crisis, More Stimulus Expected

US Urges Japan to Be Bolder in Opening Markets

Forex-Rigging Fines Could Hit $41 Billion Globally: Citi

As Apple Pay Arrives, Witnessing the Next Step in Money. Maybe.

IBM Reports Slowdown in Busines, Ditches 2015 Operating EPS

Ride-Sharing Companies Accused of Misleading Customers on Safety

How Cheap Oil Could Become a Real Problem for Airlines

UPS Says U.S. Rates to Rise 4.9% As Of December 29

Travelers Profit Jumps 6.4% on Investments, Weather

Platform Specialty Products to Pay $3.5 Billion for Arysta LifeScience

Roger Nusbaum: AdvisorShares Weekly Market Review – Week Ending 10/17/014

Howard Lindzon: Stocktoberfest – How to Invest for Profit and Joy as the Boom Continues

Be sure to follow me on Twitter.

-

Warren Buffett on Berkshire Hathaway’s Stock

Posted by Eddy Elfenbein on October 20th, 2014 at 8:12 pm -

Two More Charts

Posted by Eddy Elfenbein on October 20th, 2014 at 11:20 amHere are two charts I alluded to in Friday’s newsletter. The first shows the recent plunge in the two-year Treasury yield (the red line). I think this highlights the market’s view that higher rates may not come until later 2015, or even early 2016. I included the one-year yield (blue line) for comparison.

The second chart shows the falloff in the five-year “breakeven” rate. In simpler terms, inflation expectations have fallen a great deal in the last four months.

-

Ginni Rometty on IBM’s Quarter

Posted by Eddy Elfenbein on October 20th, 2014 at 11:09 am -

27 Years On

Posted by Eddy Elfenbein on October 20th, 2014 at 10:36 amYesterday was the 27th anniversary of the 1987 Crash. The Dow fell 508 points in one day, which was a loss of 22.6%. Today that would be a drop of 3,700 points.

Here’s the long-term chart. On the long view, the 1987 drop is barely a blip.

I ran the numbers and found that the Dow has risen 7.64% annualized since the 1987 Crash, and 8.66% annualized since the day after the 1987 Crash.

October is rife with market anniversaries. This Friday is the 85th anniversary of Black Tuesday. Next Monday is the 17th anniversary of the 1997 mini-Crash. Tomorrow is the 107th anniversary of the start of the Panic of 1907.

-

Microsoft: “a textbook example of how not to do CEO succession”

Posted by Eddy Elfenbein on October 20th, 2014 at 9:26 amAt Vanity Fair, Bethany McLean has a 7,500-word article on the challenges faced by Microsoft. Here’s a sample:

Many people blame Microsoft’s predicament on Steve Ballmer, the big, bald, manic, fist-pumping sales guy who was Bill Gates’s longtime best friend and anointed successor, becoming C.E.O. in 2000. His contentious tenure ended more abruptly than most people expected when he stepped down last February, after announcing he would do so in August 2013. After a five-month search for a new C.E.O., which Fortune called a “textbook example of how not to do CEO succession,” and which at first focused on candidates who didn’t work inside the company, Nadella, who has spent 22 years at Microsoft, was chosen. Until then, his name was barely known in the outside world. As one former Microsoft executive puts it, “He was flying commercial a year ago!”

Not the least of the board’s problems in finding a new C.E.O. was that there weren’t a lot of outsiders who wanted the job. Gates and Ballmer are both aggressive personalities. They stopped speaking to each other as a result of the bad blood surrounding Ballmer’s resignation. But both were then still sitting on the board, ready to second-guess each other and, perhaps, the new C.E.O.’s decisions.

The balance of power between Gates and Ballmer is not as obvious as it may seem. At Gates’s current clip of stock sales he will be out of Microsoft by the end of the decade. Meanwhile, Ballmer has sold very rarely, and so the consigliere now owns more of the company than the founder. Indeed, Ballmer’s 333 million shares, worth some $15 billion, make him Microsoft’s largest individual shareholder, with a 4 percent stake.

In July, Ballmer announced his $2 billion purchase of the Los Angeles Clippers basketball team from the embattled Donald Sterling; in August he abruptly announced his retirement from Microsoft’s board, citing his “multitude of new commitments.” These days Ballmer, the man who once referred to Microsoft as his “fourth child,” is working out of a 40th-floor condominium some 20 minutes from the sprawling campus he once presided over, having meetings with basketball greats. “I’m kind of moving on,” he says. It will make Nadella’s job a little bit easier.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His