-

Details from BBBY’s Earnings Call

Posted by Eddy Elfenbein on January 9th, 2014 at 9:41 amI wanted to share some details from Bed Bath & Beyond’s ($BBBY) conference call. To recap, their Q3 earnings-per-share rose 8.7% while their sales rose by 6%. Breaking down their sales increase, 78% came from comp store sales and 2% came from new stores. BBBY’s gross margins fell a bit due to inventory acquisition costs, shoppers using more and larger coupons and a shift towards lower margin goods. Expenses for selling, general and administrative dropped a bit partially thanks to lower payroll costs.

What the market is focused on today isn’t so much the third-quarter results but rather the lower guidance for Q4. A few things to point out. Last year’s fourth-quarter was 14 weeks, while this year’s is 13 weeks. Also, the data ranges are a bit off so the comparisons aren’t exactly apples to apples.

The company listed several planning assumptions that factor into their earnings forecast for Q4. I’ll summarize the important parts. BBBY sees comp store sales rising by 2% to 4%, instead of the earlier projection of 3.5% to 5.5%. Net sales are expected to fall by -3.9% to -5.7%. Again, that’s with one less week of sales. The company estimates that adjusting for the missing week, Q4 sales growth is expected to range from -0.3% to +1.6%.

Bed Bath & Beyond lowered their Q4 guidance range by ten cents per share, from $1.70 – $1.77 per share to $1.60 – $1.67 per share. Their full-year range drops from $4.88 – $5.01 per share to $4.79 – $4.86 per share.

The company added some thoughts on the coming fiscal year (Feb 2014 to Feb 2015):

Turning to fiscal 2014. While we are in the progress of completing our annual budget, our preliminary planning assumptions include the following. One, we anticipate opening approximately 30 stores across all our concepts. We anticipate the mix of store openings to be relatively consistent with fiscal 2013. Two, we expect to continue our program of renovating or repositioning stores within markets when appropriate.

Three, our operations will continue to be entirely funded from internally generated sources. Four, as previously discussed, we anticipate completing the current share repurchase program by the end of fiscal 2015. Five, we expect continuing variability in our quarterly tax rates. We will provide further information related to the fiscal first quarter and full year 2014 on our next quarterly conference call on April 9, 2014.

Before concluding this afternoon’s call, a few additional comments relative to our recently concluded fiscal third quarter. Our balance sheet and cash flows remain strong. We ended the fiscal third quarter with cash and cash equivalents and investment securities of approximately $781 million.

The stock is currently down about 11% this morning.

-

Morning News: January 9, 2014

Posted by Eddy Elfenbein on January 9th, 2014 at 6:35 amDraghi Raids Bankers in Rush to Hire 1,000 for Europe Supervisor

U.K. Trade Deficit Narrows as Exports to EU Nations Increase

China’s Answer to Amazon, Alibaba, Bans Bitcoin

China Auto Sales Up Nearly 14% in 2013

India to Seek Foreign Investment in Giant, Creaking Rail Network

Hunt for Kazakh Bank’s Missing Billions Leads to Riviera

The Big Issues Facing Fed Chair Janet Yellen

Holiday Season Sales Rise But Foot Traffic Slides

Tesco, M&S and Morrison Sales Disappoint

Watson Is Moving To NYC: IBM Announces $1 Billion Group Based On Jeopardy Ace Computer

Rupert Murdoch’s 21st Century Fox to Drop Australian Listing

BlackRock Agrees to Stop Pursuing Nonpublic Views

P. Diddy and Diageo Buy Tequila Brand DeLeon

Jeff Carter: Advice on How To Build An Innovative Business-Don’t Become A Suit

Jeff Miller: The Most Expensive “Free” Advice – 2014 Update

Be sure to follow me on Twitter.

-

Bed Bath & Beyond Cuts Guidance

Posted by Eddy Elfenbein on January 8th, 2014 at 5:06 pmAfter the closing bell, Bed Bath & Beyond (BBBY) released a very disappointing earnings report. For the third quarter (Sep-Oct-Nov), the home furnishings company earned $1.12 per share. That was three cents below Wall Street’s forecast.

The company had said they expected Q3 to range between $1.11 and $1.16 per share. So technically, BBBY hit their own guidance, but the Street was expecting more (and so was I).

Net sales rose 6% from last year’s third quarter. Comparable store sales, which is a key metric for retailers, rose by 1.3%. Honestly, that’s not that great.

So far this year, BBBY has earned $3.20 per share for the first three quarters. That’s a nice increase over the $2.89 per share from the same period last year.

Now for the bad news. Bed Bath & Beyond cut their Q4 guidance. I was afraid this might happen. The previous range was $1.70 to $1.77. Now it’s $1.60 to $1.67 per share — so 10 cents at both ends. That lowers the full-year range from $4.88 – $5.01 per share to $4.79 – $4.86 per share. I had been expecting the company to clear $5 per share for the year. For some context, last year, BBBY earned $4.56 per share.

The stock is getting pounded in the after-hours market. It’s currently down $6.63 or 8.32%. This is ugly, but I urge you to not get rattled. This has happened to Bed Bath & Beyond a few times before. In fact, it’s been much worse before — and each time, the stock has come back.

Here are the sales and earnings figures for the past few quarters:

Quarter Sales Gross Profit Operating Profit Net Profit EPS May-99 $356,633 $146,214 $28,015 $17,883 $0.06 Aug-99 $451,715 $185,570 $53,580 $33,247 $0.12 Nov-00 $480,145 $196,784 $50,607 $31,707 $0.11 Feb-00 $569,012 $238,233 $77,138 $48,392 $0.17 May-00 $459,163 $187,293 $36,339 $23,364 $0.08 Aug-00 $589,381 $241,284 $70,009 $43,578 $0.15 Nov-01 $602,004 $246,080 $64,592 $40,665 $0.14 Feb-01 $746,107 $311,802 $101,898 $64,315 $0.22 May-01 $575,833 $234,959 $45,602 $30,007 $0.10 Aug-01 $713,636 $291,342 $84,672 $53,954 $0.18 Nov-02 $759,438 $311,030 $83,749 $52,964 $0.18 Feb-02 $879,055 $370,235 $132,077 $82,674 $0.28 May-02 $776,798 $318,362 $72,701 $46,299 $0.15 Aug-02 $903,044 $370,335 $119,687 $75,459 $0.25 Nov-03 $936,030 $386,224 $119,228 $75,112 $0.25 Feb-03 $1,049,292 $443,626 $168,441 $105,309 $0.35 May-03 $893,868 $367,180 $90,450 $57,508 $0.19 Aug-03 $1,111,445 $459,145 $155,867 $97,208 $0.32 Nov-04 $1,174,740 $486,987 $161,459 $100,506 $0.33 Feb-04 $1,297,928 $563,352 $231,567 $144,248 $0.47 May-04 $1,100,917 $456,774 $128,707 $82,049 $0.27 Aug-04 $1,273,960 $530,829 $189,108 $120,008 $0.39 Nov-05 $1,305,155 $548,152 $190,978 $121,927 $0.40 Feb-05 $1,467,646 $650,546 $283,621 $180,980 $0.59 May-05 $1,244,421 $520,781 $150,884 $98,903 $0.33 Aug-05 $1,431,182 $601,784 $217,877 $141,402 $0.47 Nov-06 $1,448,680 $615,363 $205,493 $134,620 $0.45 Feb-06 $1,685,279 $747,820 $304,917 $197,922 $0.67 May-06 $1,395,963 $590,098 $148,750 $100,431 $0.35 Aug-06 $1,607,239 $678,249 $219,622 $145,535 $0.51 Nov-07 $1,619,240 $704,073 $211,134 $142,436 $0.50 Feb-07 $1,994,987 $862,982 $309,895 $205,842 $0.72 May-07 $1,553,293 $646,109 $154,391 $104,647 $0.38 Aug-07 $1,767,716 $732,158 $211,037 $147,008 $0.55 Nov-08 $1,794,747 $747,866 $203,152 $138,232 $0.52 Feb-08 $1,933,186 $799,098 $259,442 $172,921 $0.66 May-08 $1,648,491 $656,000 $118,819 $76,777 $0.30 Aug-08 $1,853,892 $739,321 $187,421 $119,268 $0.46 Nov-08 $1,782,683 $692,857 $136,374 $87,700 $0.34 Feb-09 $1,923,274 $785,058 $231,282 $141,378 $0.55 May-09 $1,694,340 $666,818 $142,304 $87,172 $0.34 Aug-09 $1,914,909 $773,393 $222,031 $135,531 $0.52 Nov-09 $1,975,465 $812,412 $245,611 $151,288 $0.58 Feb-10 $2,244,079 $955,496 $370,741 $226,042 $0.86 May-10 $1,923,051 $775,036 $225,394 $137,553 $0.52 Aug-10 $2,136,730 $874,918 $296,902 $181,755 $0.70 Nov-10 $2,193,755 $896,508 $305,110 $188,574 $0.74 Feb-11 $2,504,967 $1,076,467 $461,052 $283,451 $1.12 May-11 $2,109,951 $857,572 $288,948 $180,578 $0.72 Aug-11 $2,314,064 $950,999 $371,636 $229,372 $0.93 Nov-11 $2,343,561 $958,693 $357,020 $228,544 $0.95 Feb-12 $2,732,314 $1,163,669 $550,765 $351,043 $1.48 May-12 $2,218,292 $887,199 $313,398 $206,836 $0.89 Aug-12 $2,593,015 $1,032,669 $365,137 $224,330 $0.98 Nov-12 $2,701,801 $1,074,010 $361,649 $232,750 $1.03 Feb-13 $3,401,477 $1,394,877 $598,034 $373,872 $1.68 May-13 $2,612,140 $1,032,971 $323,101 $202,490 $0.93 Aug-13 $2,823,672 $1,113,484 $389,766 $249,304 $1.16 Nov-13 $2,864,837 $1,121,690 $374,647 $227,197 $1.12 -

The Fed Did Discuss Adjusting the Evans Rule

Posted by Eddy Elfenbein on January 8th, 2014 at 2:38 pmThis morning, I laid out my thoughts on the Fed changing or even ditching the Evans Rule (the threshold of 6.5% unemployment before raising short-term interest rates). It turns out, they did discuss this issue in December:

Participants also considered the potential for clarifying or strengthening the Committee’s forward guidance for the federal funds rate.

In general, participants who favored amending the forward guidance saw a need to more fully communicate how, if the unemployment rate threshold was reached first, the Committee would likely set monetary policy after that threshold was crossed.

A number of participants pointed out that the federal funds rate paths underlying the economic forecasts that they prepared for this meeting, as well as expectations for the funds rate path priced into financial markets, were consistent with the view that the Committee would not raise the federal funds rate until well after the time that the threshold was crossed. (Yep, that seems very much the case. – Eddy)

A few participants discussed the potential advantages and disadvantages of using medians of the projections of the federal funds rate from the SEP as a means of communicating the likely path of short-term interest rates.

Some worried that, if the Committee began to reduce asset purchases, market expectations might shift, and they wanted to reinforce the forward guidance to mitigate the risks of an undesired tightening of financial conditions that could have adverse effects on the economy.

In light of their concern that inflation might continue to run well below the Committee’s longer-run objective, several participants saw the need to clearly convey that inflation remains an important consideration in adjusting the target funds rate.

Participants debated the advantages and disadvantages of lowering the unemployment rate threshold provided in the forward guidance.

In the view of the few participants who advocated such a change, a lower threshold would be a clear signal of the Committee’s intentions and was an appropriate adjustment in light of recent labor market and inflation trends. (I agree.)

In contrast, a few others expressed concern that any change in the threshold might be confusing and could undermine the credibility of the Committee’s forward guidance. (But your credibility will also be hurt if you don’t adhere to your previous guidance.)

Most were inclined to retain the current thresholds for the unemployment and inflation rates and to instead provide qualitative guidance regarding the Committee’s likely behavior after a threshold was crossed.

So no change for now, but it’s on the radar. That’s a good thing.

-

Riverbed Gets $19 Offer

Posted by Eddy Elfenbein on January 8th, 2014 at 2:27 pmLast February, shares of Riverbed Technology ($RVBD) got smashed. In March, I highlighted Riverbed when it had fallen below $15 per share. I said “the shares have dropped down to a good price.”

RVBD bounced around for much of last year but started to catch fire in late October. The stock closed yesterday at $17.85. Today brought word that Paul Singer, a prominent hedge fund manager, is offering $19 per share for RVBD.

“We believe in the quality of Riverbed’s assets,” Jesse Cohn, an Elliott portfolio manager wrote in a letter to Riverbed’s board of directors. “However, Riverbed’s valuation has been impaired by slowing growth in its core WAN optimization market and by significant investments in both acquisitions and operating expenses undertaken to diversify away from the core WAN optimization business.”

Elliott Associates first took a stake in Riverbed in September and by November the New York-based activist hedge fund had disclosed a 10.4% stake in the company, causing the company’s stock to rise. Elliott has said it believes the company is “significantly undervalued.”

The stock zoomed higher today. The market, apparently, expects more, perhaps a counteroffer. RVBD is currently at $19.83 per share.

-

Today’s Fed Minutes

Posted by Eddy Elfenbein on January 8th, 2014 at 2:23 pmThe Fed minutes report never tells us who said what. Instead, we’re treated to a stream of indefinite pronouns (“some” members said this, “a few” said that)

Here’s the unaudited count of appearances in today’s Fed minutes:

Some – 11*

Most – 10

A few – 8

Several – 6**

Many – 6

A number of – 5

One – 5

A couple of – 4

Almost all – 2

All – 1

A majority of – 1*Includes one “some other”

** Includes one “several others” -

ADP Report = 238,000 Jobs

Posted by Eddy Elfenbein on January 8th, 2014 at 10:51 amWall Street is intensely focused on this Friday’s jobs report. The last few reports have been pretty good, and investors are curious if we’ll see more of the same. We got a sneak peak today when ADP, the private payroll firm, said that 238,000 net new jobs were added to the economy last month. That’s not bad, but I hasten to add that ADP isn’t always the best forecaster of what the government will say. For Friday, the consensus on the Street is for a gain of 195,000 jobs.

Turning to our Buy List, Ford Motor ($F), is getting a nice lift today after Alan Mulally said that he won’t be taking the CEO spot at Microsoft ($MSFT), another Buy List stock. I thought this was pretty obvious, but there were folks who thought it was a done deal. Shares of Ford got as high as $15.71 today.

Later today, the Fed will release the minutes from its last meeting. This is the meeting at which the Fed finally decided to taper its bond purchases. I’m curious about what the discussion was. (Remember that Fed minutes are a nice lesson is the use of indefinite pronouns—“some” said, “many” said, “a few” dissented from that.)

Not much else is going on. After today’s close, Bed Bath & Beyond ($BBBY) will report its fiscal Q3 earnings. The company has told us to expect earnings to range between $1.11 and $1.16 per share. They’ve also said that earnings for the current quarter, which is not quite halfway done, will range between $1.70 and $1.77 per share. It will be interesting to see if they adjust that forecast.

-

Will the Fed Ditch the Evans Rule?

Posted by Eddy Elfenbein on January 8th, 2014 at 9:23 amA little over a year ago, the Federal Reserve introduced a new policy: The Fed said it wouldn’t raise short-term interest rates until the unemployment rate reached 6.5%. Ben Bernanke was careful to say that this was a threshold and not a trigger. He’s repeated that many times since.

The use of this specific economic metric has been referred to as the Evans Rule in honor of Chicago Fed President Charles Evans, who has advocating using such a strategy. One of the odd parts of monetary policy is that it’s much more effective if it’s seen as credible. A central bank can yammer all they want, but if no one believes them, the implementation of policy becomes that much harder. Credibility is the watchword for any modern central banker.

While the Fed is still seen as an opaque and secretive institution, Ben Bernanke has probably pulled back the curtain more than any other Fed chair. As such, the Bernanke Fed has also been careful in telegraphing their intentions to market participants (see Hilsenrath comma Jon). That’s also why last year’s Taper Tantrum was so bizarre.

I think the commitment to credibility is why the Evans Rule may not live much longer, or more specifically, the 6.5% threshold. The fact is that the unemployment rate is falling, and falling rather quickly. The rate for November was 7.0%. This morning’s ADP report was encouraging, and now it seems very likely that we could hit 6.5% unemployment by the middle of this year. The report for December comes out this Friday.

Yet there seems to be no demand for short-term interest rates to rise anytime soon. The one-year Treasury is still around 0.13%. At this point, most FOMC members don’t expect a Fed rate increase until 2015—and a good majority of them don’t expect much of an increase next year.

Will it hurt the Fed’s vaunted credibility with the market as unemployment drops and the Fed does nothing month after month? You could say that Bernanke’s threshold-not-trigger statement grants them some leeway, but how much? When the Fed adopted the Evans Rule in December 2012, it was a cost-free commitment. The rule told traders what to expect and when, and helped remove a lot of worry from the markets. But now that promise is coming due.

I rate this as an event with a low probability but one with a large potential impact. At some point this year, the Fed may alter the Evans Rule and lower the threshold to 6%.

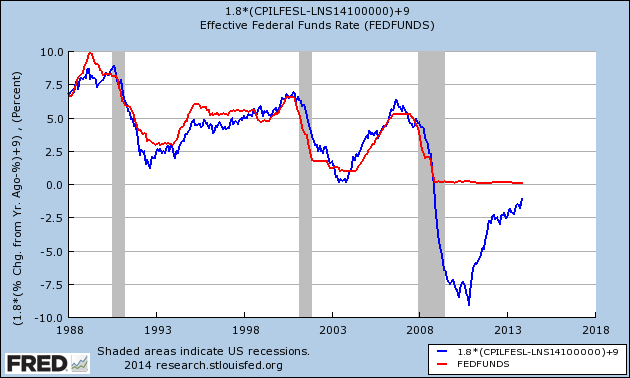

One final note: Here’s a very simplified version of the Taylor Rule, with variables via Paul Krugman (the Fed Funds rate should be 1.8 times the difference between unemployment and inflation, plus 9). Please note that Krugman has said that “using historical estimates of the Taylor rule is not a good way either to predict Fed policy or to recommend Fed policy at this point in our history.” It’s a better estimate to what the Fed has been thinking.

-

Morning News: January 8, 2013

Posted by Eddy Elfenbein on January 8th, 2014 at 6:46 amEuro-Zone Retail Sales in Surprise Surge

America to Europe: Stronger Banking Union Would Help Boost Growth

U.K. Banks to Ramp Up Lending After Surge in Demand

Calls to Drop 1970s-Era U.S. Oil Export Ban Stir Political Fight

Natural Gas Prices Surge on Cold Snap

Obama Speaks of Better Days for Economy, With Asterisk

House Financial Services Chairman to Seek Volcker Rule Change

JPMorgan to Pay $2.6 Billion Over Madoff Scheme Lapses

Madoff Trustee Tops $10 Billion Recovery With Bank Deal

Facebook to Buy Android App Monitoring Tool Maker

Aereo Receives $34 Million Boost

Cisco CEO Pegs Internet of Things as $19 Trillion Market

Chinese Tycoon Admits New York Times Bid Faces Obstacles

Cullen Roche: The Biggest Myths in Economics

Edward Harrison: Tightening Into Frothy Markets in the Asset-Based Economy

Be sure to follow me on Twitter.

-

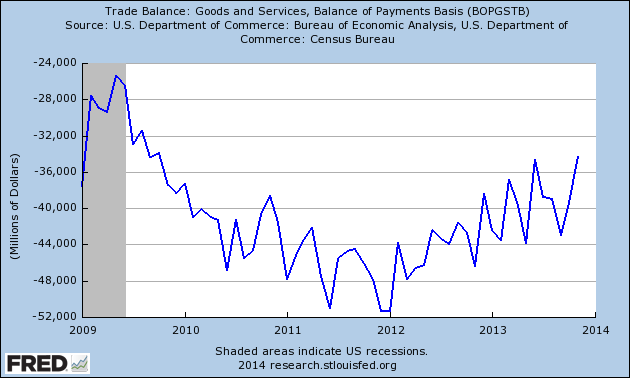

Trade Deficit Falls to Four-Year Low

Posted by Eddy Elfenbein on January 7th, 2014 at 10:32 amAfter three straight down days, the stock market is finally looking up this morning. The S&P 500 is currently up about 11 points or 0.6%. Healthcare stocks are doing particularly well. Buy List stocks like Medtronic ($MDT) and CR Bard ($BCR) are solidly in the black this morning.

The Commerce Department reported that the trade deficit for November fell to $34.3 billion. That’s the smallest gap in more than four years. A key driver of the smaller deficit is lower oil prices. The deficit for November was less than Wall Street’s consensus of $39.9 billion. Most of the trade deficit is with China, and that gap fell to $26.9 billion in November. Exports are now 17% above where they were before the recession.

This is the quiet period before earnings season begins. The first big company to report will be Alcoa ($AA) which reports after the bell on Thursday. Bed Bath & Beyond ($BBBY) is also due to report this week, but that’s for the period ending in November.

Bloomberg notes that according to analyst estimates, “earnings for companies in the S&P 500 will climb 9.7 percent on average this year, almost twice the rate of 2013, while sales will probably increase 3.8 percent.”

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His