-

CADY

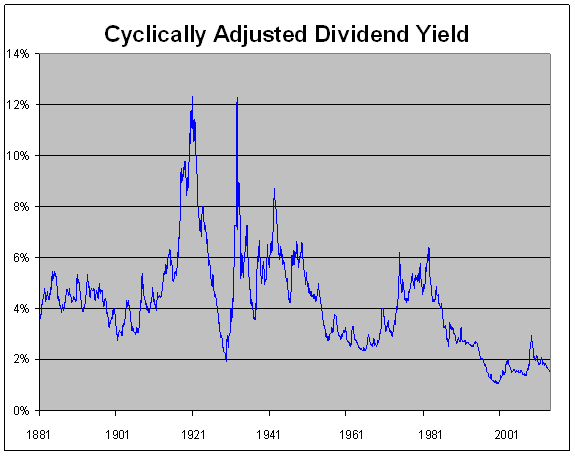

Posted by Eddy Elfenbein on January 13th, 2014 at 12:40 pmThere’s been a lot written lately on the Cyclically Adjusted Price/Earnings Ratio (or CAPE). I highly recommend what Josh and Jesse have written.

CAPE is the Price/Earnings Ratio but based on the last 10 years of earnings instead of the last one year. I’ve never been much of a fan of CAPE. My reasoning is pretty basic — valuations are cyclical so there’s no need to adjust the earnings side of the P/E Ratio.

I went to look at the data on Prof. Shiller’s website, but I made one small adjustment. I changed the earnings input to dividends.** So instead of the trailing 10 years of earnings, this is what the trailing 10 years of dividends looks like, or as I’m calling it, CADY (Cyclically Adjusted Dividend Yield):

We see much the same as the CAPE graph, the current market is vastly overpriced. In fact, with CADY it’s even more so. But this underscores the point Josh makes—it’s not different this time, it’s different every time. According to CADY, the market has been priced above its long-term average every month over the last 28 years. The current stock market would have to drop 64% before CADY reached its long-term average.

Sounds crazy? I would argue that CADY has a major advantage over CAPE in that we don’t have to dig through all the accounting issues (Jesse does a great jobs on this). A dividend payment, after all, is a dividend payment.

Some of you might object to CADY by noting that dividend payout ratios have fallen so the yield should be less. But that’s my point exactly. The nature of stock ownership has changed over the decades, so the valuations metrics have also changed. By looking at CADY, I hope it highlights the problems of looking at CAPE. I love looking at old stock data, but be leery of drawing too many conclusions when looking at stock data before 1960.

** For the excel file, I changed the J’s in column K to I’s, and divided by the H cell factor instead of vice versa.

-

GoodBrokas

Posted by Eddy Elfenbein on January 13th, 2014 at 11:59 amOver the weekend, I saw “The Wolf of Wall Street.” I thought it was an entertaining albeit flawed movie. It’s disappointing to see a movie by one of your favorite directors about a subject you’re familiar with fall short of what you had hoped for. (I should mention that in the early 1990s, I was a cold-caller for a shady brokerage outfit in Boston, but rest assured gentle reader, it was a far cry from the buffoonish culture of Stratton Oakmont.)

I’m not in the habit of reviewing movies, so take my comments as the views of an amateur. For one, I though the movie was far too long. There’s nothing wrong with a movie going on for three hours, but so much of the “The Wolf of Wall Street” was redundant. We see similar scenes over and over again.

For example, Martin Scorsese’s attempt to capture the over-the-top lifestyle of Stratton Oakmont was itself over-the-top. We get it—there were drugs, prostitutes and debauchery, but does that has to be shown repeatedly?

But what troubled me most was that once you peel away the drug-coated layers of Jordan Belfort, there’s nothing particularly interesting about him, his character or his crimes. He’s just a petty thief, but on a larger scale. The guys at Stratton Oakmont aren’t smart or interesting.

I can’t help but think what a movie about the Great Salad Oil Swindle of 50 years ago would be like. Now those guys were smart.

I’ve never seen a movie where another movie, in this case, Goodfellas, ghostly floats through each scene. From Belfort’s rise and fall to his tempestuous marriage, so much of the Wolf of Wall Street strives to catch Goodfellas. Leonardo DiCaprio even sounds like Ray Liotta. But there’s a critical difference. We see behind the worldview, character and motivations of Henry Hill and his gangster associates. Consider this famous line:

Hundreds of guys depended on Paulie and he got a piece of everything they made. And it was tribute, just like in the old country, except they were doing it here in America. And all they got from Paulie was protection from other guys looking to rip them off. And that’s what it’s all about. That’s what the FBI could never understand. That what Paulie and the organization does is offer protection for people who can’t go to the cops. That’s it. That’s all it is. They’re like the police department for wiseguys.

That’s a brilliant line and it tells us so much. There’s nothing in the Wolf of Wall Street that comes close to that one line. Jordan Belfort? He’s just a dumb crook. He even distorts the famous 1991 Forbes article. For one, no one ever called him the Wolf of Wall Street. Belfort made up his own nickname. The Forbes article is one of disdain and it was clear that he was going to be caught eventually.

Even the oleaginous Gordon Gekko in “Wall Street” has a larger (but damaged) worldview. Remember that he closes his famous “greed is good” speech by saying that greed will save “that other malfunctioning corporation called the USA.” It’s that movie’s flaw that Gekko is finally done in by breaking the law instead of the consequences of how he sees the world. Chalk that up to Oliver Stone’s heavy-handedness.

A movie covering the misdeeds of Wall Street could be fascinating. But despite Mr. Belfort’s self-given nickname, Stratton Oakmont has little to do with the real Wall Street. The workings of Goldman Sachs or Morgan Stanley might as well be in another universe as some bucket shop on Long Island.

Last year, Leonardo DiCaprio played another Long Island-based fraudster who threw big parties:

If personality is an unbroken series of successful gestures, then there was something gorgeous about him, some heightened sensitivity to the promises of life, as if he were related to one of those intricate machines that register earthquakes ten thousand miles away.

There’s nothing gorgeous about Jordan Belfort. Instead of Jay Gatsby, the Wolf of Wall Street gives us a bunch of drug-addled bros.

-

Morning News: January 13, 2014

Posted by Eddy Elfenbein on January 13th, 2014 at 6:44 amHSBC Sees Ruble Offering 6% Drop to Growth Effort

$51 Billion and Change: Sochi Most Expensive Olympics Ever

Cost of Cool in India? An iPhone

Chew Marks on $4 Million Has U.S. Seeing Shaggy Dog Story

Total Becomes Largest Oil Producer to Acquire U.K. Shale

With Data Vulnerable, Retailers Look For Tougher Security>

Amec Agrees to Buy Swiss Rival for $3.2 BIllion

Sanofi Pays $700 Million for Alnylam Drugs and Stake

Airbus Posts Record Orders, Ponders Higher Production

New CEO Barra A ‘Lifer’ Bent on Tearing Down Walls

BMW Aims For Another Gain in Vehicle Sales After 2013 Record

Etihad CEO Says Will Not Be Rushed on Alitalia Decision

Dollar Stores Are Now Getting Too Expensive for Many Americans

Cullen Roche: The Biggest Myths in Economics

Jeff Miller: Weighing the Week Ahead: Can Earnings Growth Propel Stocks Higher?

Be sure to follow me on Twitter.

-

With 7 Trading Days In….

Posted by Eddy Elfenbein on January 10th, 2014 at 4:42 pmNow that the 2014 investing year is seven days old, I’m happy to report that our Buy List has a very, very, very tiny lead over the S&P 500.

Or to be more accurate, we’re down a smidgen less than they are. Through Friday, our Buy List has lost -0.29% compared with the S&P 500’s loss of -0.32%.

I do have a serious point here. I really don’t care about trading results over such a short time horizon. I believe we’ll do well over the long haul. But the important lesson here is that our Buy List is beating the market despite yesterday’s big plunge in Bed Bath & Beyond ($BBBY). That stock dropped more than 12% on Thursday.

That’s why having a well-diversified portfolio is so important. I specifically design our Buy List to be diversified so the overall portfolio is rather conservative. You’d be surprised how many investors think diversification means owning both Facebook AND Twitter. Think of portfolio diversity as a tool, not an obligation. It really does work.

-

How to Succeed with Brunettes

Posted by Eddy Elfenbein on January 10th, 2014 at 4:12 pmThe trading week is over, but we don’t stop bringing you valuable information. From the U.S. Navy in 1966, here’s “How to Succeed with Brunettes.”

-

December NFP = 74,000

Posted by Eddy Elfenbein on January 10th, 2014 at 10:34 amThe government released the jobs report for December, and the economy created only 74,000 net new jobs last month. The consensus was for 200,000 jobs. That’s the smallest gain in more than three years.

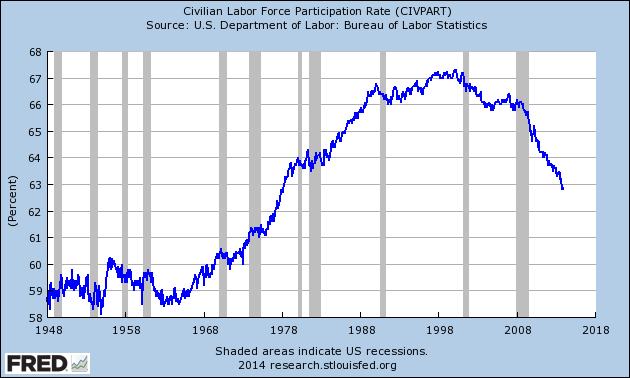

The odd part is that because of a smaller workforce, the unemployment rate dropped down to 6.7%. That’s the lowest in more than four years. The labor force participation rate fell to 62.8% for December. It hasn’t been this low since 1978.

I think this jobs report will cause the Fed to change its unemployment rate threshold for raising short-term interest rates. Right now, that threshold is 6.5%, and we’ll probably pass below it soon. I think the Fed will lower their threshold to 6% sometime this year.

-

CWS Market Review – January 10, 2014

Posted by Eddy Elfenbein on January 10th, 2014 at 7:18 am“It amazes me how people are often more willing to act based on little or

no data than to use data that is a challenge to assemble.” – Robert J. ShillerThere’s a weird new feeling on Wall Street these days. For the first time in a long while, folks are actually optimistic about the economy. How about that? In fact, it’s now conventional wisdom that 2014 will be the best year for the economy since the recession.

Unfortunately, that’s a rather low bar to clear. Still, the signs keep coming in positive. This week, we learned that thanks to rising exports, the U.S. trade deficit fell to a four-year low. Another key indicator is that freight rail traffic is at an all-time high. The housing market is also doing well, and construction spending is the highest it’s been since March 2009.

The GDP report for the third quarter had the second-best growth rate in the last 30 quarters (again, low bar). Lately, firms up and down Wall Street have been revising their estimates for Q4 higher. Merrill Lynch now says they see Q4 GDP coming in at 3%, and they project real consumer spending to rise by 4%.

Of course, there are still lots of weak spots in the economy, and the jobs market is a major concern. I’m writing this to you early on Friday, and the big January jobs report comes out later today. The consensus on Wall Street is that the economy created 200,000 net new jobs last month. I won’t try to predict if that’s right or wrong but I’ll note that ADP’s report, that’s the private payroll firm, came in at 238,000 net new jobs. For us, the important thing is to see if the promising trend remains in place. More jobs mean more consumers and that means more profits. It’s just that simple.

Fourth-quarter earnings season has finally arrived. Over the next five weeks, 16 of our 20 Buy List stocks will report earnings. In this week’s CWS Market Review, I’ll highlight Wells Fargo ($WFC) which will be our first earnings report for this earnings season. I’ll also take a closer look at what the Fed has in store for us this year. Later on, I’ll discuss the terrible, horrible, no good, very bad day Bed Bath & Beyond ($BBBY) had on Thursday. The shares plunged 12.5% after they lowered their Q4 guidance (Spoiler alert: I still like BBBY). On the plus side, Ford Motor ($F) raised its quarterly dividend by 25%. But first, let’s look at what last year’s broad-based rally means for us.

History Says “Let Your Winners Run”

One interesting aspect about the market’s rally is how broad-based it’s been. Previous big rallies have often been uneven and skewed to certain sectors like tech or emerging markets. But last year, 460 of the S&P 500 stocks gained ground. That’s the most since at least 1990. We can also see the broad participation by looking at the equally-weighted version of the S&P 500 (the standard version is weighted by value). The equally-weighted S&P 500 jumped 34% last year and it’s up an amazing 248% from the March 2009 low (below is a chart of an equally weighted S&P 500 ETF).

A broad-based rally has historically been an omen for more good things to come. When more than 400 stocks in the S&P 500 rally, the market averages a 14% return the following year. Also, some folks are worried about rising valuations, but history is again on the side of the bulls. Since 1936, there have been 156 quarters in which the S&P 500’s P/E Ratio has expanded. The index climbed 108 times in the following quarter (or 69% of the time). In other words, letting your winners run has been a good strategy.

I should also note that firms are starting to invest their massive cash hordes. The companies in the S&P 500 are sitting on a total of $3.8 trillion. Between you and me, that’s a lot of money. This is what some folks are calling “the capex recovery,” and I think it’s for real. Don’t get me wrong. I love me some dividends, but companies are beginning to realize they need to invest in order to grow. Getting next to nothing for your cash may have been fine in 2009 or 2010, but that won’t cut it in 2014. Ford and Microsoft are two such companies that have ambitious business investment plans for this year. Now let’s look at what the Federal Reserve may have up its sleeve.

Will the Fed Alter the Evans Rule?

On Monday, Janet Yellen was confirmed as the next Chairman of the Federal Reserve. She’ll take over from Bernanke on February 1, but that may not be the only big change at the Fed. I think there’s a small but growing chance that the Fed may alter the “Evans Rule.”

Let me explain. A little over a year ago, the Federal Reserve introduced a new policy: The Fed said it wouldn’t raise short-term interest rates until the unemployment rate reached 6.5%. Ben Bernanke was careful to say that this was a threshold and not a trigger. He’s repeated that many times since.

The use of this specific economic metric has been referred to as the Evans Rule in honor of Chicago Fed President Charles Evans, who has advocating using such a strategy. One of the odd parts of monetary policy is that it’s much more effective if it’s seen as credible. A central bank can yammer all they want, but if no one believes them, the implementation of policy becomes that much harder. Credibility is the watchword for any modern central banker.

While the Fed is still seen as an opaque and secretive institution, Ben Bernanke has probably pulled back the curtain more than any other Fed chair. As such, the Bernanke Fed has also been careful in telegraphing their intentions to market participants. That’s also why last year’s Taper Tantrum was so bizarre.

I think the commitment to credibility is why the Evans Rule may not live much longer-or more specifically, the 6.5% threshold. The fact is that the unemployment rate has fallen a good deal, and there’s a good chance we could hit 6.5% by the middle of this year.

Yet there seems to be no demand for short-term interest rates to rise anytime soon. The one-year Treasury is still around 0.13%. At this point, most FOMC members don’t expect a Fed rate increase until 2015—and a good majority of them don’t expect much of an increase next year.

This week, we got the minutes from the Fed’s December meeting. This was the one where the Fed finally decided to taper their bond purchases. I thought it was interesting that the minutes indicated that some members felt the FOMC needed to lower the unemployment threshold. While this view wasn’t adopted by the committee, it’s clearly on their radar.

It could hurt the Fed’s credibility with the market if unemployment drops and the Fed does nothing month after month. I suppose that Bernanke’s threshold-not-trigger statement grants them some leeway, but I’m not sure how much. I expect to see more tapering in 2014, but I doubt we’ll see any interest rate increases. There’s just no inflation pressure-at least, not yet.

When the Fed adopted the Evans Rule in December 2012, it was a cost-free commitment. The rule told traders what to expect and when, and it helped remove a lot of worry from the markets. But now that promise is coming due.

Frankly, I rate altering the Evans Rule as an event with a low probability but one with a large potential impact. At some point this year, the Fed may alter the Evans Rule and lower the threshold to 6%. In my view, that would be very good for the market.

Bed Bath & Beyond Drops 12.5%

After the closing bell on Wednesday, Bed Bath & Beyond ($BBBY) released a disappointing earnings report. For the third quarter (Sep-Oct-Nov), the home furnishings company earned $1.12 per share. That was three cents below Wall Street’s forecast.

Previously, the company had said they expected Q3 to range between $1.11 and $1.16 per share. So technically, BBBY hit their own guidance, but the Street was expecting more (and so was I). Net sales rose 6% from last year’s third quarter. Comparable store sales, which is a key metric for retailers, rose by 1.3%. Honestly, that’s not that great. So far this year, BBBY has earned $3.20 per share for the first three quarters, and that’s a nice increase over the $2.89 per share from the same period last year.

But the bad news is that BBBY cut their Q4 guidance. I was afraid this might happen. The previous range was $1.70 – $1.77 per share. Now it’s $1.60 – $1.67 per share, so 10 cents at both ends. That lowers their full-year range from $4.88 – $5.01 per share to $4.79 – $4.86 per share. I had been expecting the company to clear $5 per share for the year. For some context, last year, BBBY earned $4.56 per share.

Yesterday was ugly. The stock got crushed for a 12.5% loss. I know this is painful and I apologize for the volatility, but traders aren’t always so rational. In fact, this kind of thing has happened to BBBY before. Eighteen months ago, BBBY got hammered for a one-day loss of 17%. What happened? They had actually beaten expectations but lowered their quarterly and full-year guidance.

The odd thing is that once those results were known, many months later, they really weren’t that far off from Wall Street’s original estimate. Before the June 2012 plunge, Wall Street had expected full-year earnings of $4.63 per share, and as I had mentioned before, they earned $4.56 per share last year. So the market panicked with a 17% drop in response to (what turned out to be) an earnings adjustment of less than 2%. Not surprisingly, the aftermath of the sell-off was a great buying opportunity. This is exactly why we like high-quality stocks.

Now let’s break down some of the numbers. For Q3, Bed Bath & Beyond’s EPS grew by 8.7% while their sales rose by 6%. Of that sales increase, 78% came from comp store sales and 2% came from new stores. BBBY’s gross margins fell a bit due to inventory acquisition costs, shoppers using more and larger coupons and a shift towards lower margin goods. Expenses for selling, general and administrative dropped a bit partially thanks to lower payroll costs.

There are also a few technical points. Bed Bath & Beyond doesn’t use three-month quarters; they use 13-week quarters. Since one year isn’t exactly 52 weeks, every so often, they have to use a 14-week quarter. Last year’s fourth quarter was a 14-weeker so the comparisons aren’t quite apples to apples. Also, the date range isn’t the same either (this is important because it covers the important holiday shopping season).

For Q4, BBBY sees comp store sales rising by 2% to 4%, instead of the earlier projection of 3.5% to 5.5%. Net sales are expected to fall by -3.9% to -5.7%. Again, that’s with one less week of sales. The company estimates that adjusting for the missing week, Q4 sales growth will range from -0.3% to +1.6%.

Bed Bath & Beyond didn’t have a lot to say about the coming fiscal year, but they did say they anticipate opening 30 stores next year. They also continue to have a very strong balance sheet. I expect more details in April when the Q4 report comes out.

Here’s my take: This is where our locked-and-sealed strategy comes to the test. Lots of investors would dump BBBY at the first sign of trouble, but I’m not doing that. This is a very well-run outfit that really had a fairly minor adjustment to their earnings outlook. The shares are going for a bit over 14 times this year’s earnings. Sure, the one-day plunge ain’t a lot of fun, but that’s how the stock market works. The long-run is still in our favor and I’m sticking with BBBY. To reflect the sell-off, I’m lowering the Buy Below to $77 per share.

Ford Raises Dividend By 25%

Not all the news was lousy this week. Ford Motor ($F) investors got some pleasant news when CEO Alan Mulally officially withdrew his name from consideration for the top job at Microsoft ($MSFT). From the beginning, I doubted he would jump ship. Mulally and his team have done a commendable job in turning around Ford, but the job is far from done. Their European operations still need a lot of work.

In the CWS Market Review from November 8, I wrote, “I also expect the company will raise their quarterly dividend in January. The current dividend is 10 cents per share, and I think it can rise to 12 or 13 cents per share.” This week, Ford raised their quarterly dividend by 25% to 12.5 cents per share. So it turns out, they chose the middle-point of my range.

Ford’s CFO, Bob Shanks, said, “This increase in the dividend provides our shareholders with a regular, growing dividend that we believe is sustainable over an economic or business cycle.” Things continue to move in Ford’s direction. Two years ago, Ford restored its dividend at five cents per share. Last year, they doubled it to ten cents, and now we’re at 12.5 cents. Going by Thursday’s close, the stock yields 3.16%. Ford remains a good buy up to $17 per share.

Wells Fargo Is a Buy up to $48 Per Share

The first Buy List stock to report this earnings season will be our favorite big bank, Wells Fargo ($WFC). Wells is due to report on Tuesday morning, January 14. Business at Wells has been going pretty well lately. The bank has beaten its earnings estimates for the last eight quarters in a row. For Q4, the current consensus on Wall Street is for earnings of 98 cents per share.

If Wells does earn 98 cents for Q4, that would give them $3.87 for all of 2013, which is quite good. That’s a strong improvement over the $3.37 per share they made in 2012. The easy earnings growth may be a bit harder to come by in 2014. On one hand, the improving economy means that more people are paying their bills on time. But the downside is that Wells’s mortgage business has slowed down. If you recall, WFC laid off 5,300 people in their mortgage division last year. That was painful but necessary. Wall Street currently expects Wells to earn $4.01 per share next year, which is probably a bit low. Even if that’s right, it gives the stock a forward P/E of just 11.5. That’s a good value.

Fortunately, the stock has continued to do well. On Thursday, WFC got as high as $46.20 per share which is another all-time high. Later this spring, I expect to see another dividend increase from Wells. Until the earnings report comes out, I want to keep a tight leash on our Buy Below price. Wells Fargo is a very good buy up to $48 per share.

That’s all for now. Next week will be the first full week of earnings season. We’ll also get some key economic reports. On Tuesday, we get retail sales. The Fed’s Beige Book is on Wednesday, and the CPI report comes out on Thursday. I’m also curious to see the Industrial Production report which is due on Friday. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: January 10, 2014

Posted by Eddy Elfenbein on January 10th, 2014 at 6:29 amEuropean Central Bank Ready For ‘Decisive Action’ To Aid Economy

Covered Bond Shock Forces Denmark to Devise Plan B for Banks

Skagen Says Ignore Wall Street, Bet on Emerging Markets

China Exports to Face Tough 2014 as Yuan Climbs

Japanese Begin to Question Protections Given to Homegrown Rice

Warren Says She Expects Yellen Will Boost Fed’s Bank Oversight

New Mortgage Rules Aim to Protect Home Buyers, Owners

Retailers of All Stripes Sing Holiday Blues

Gartner Says Worldwide PC Shipments Declined 6.9 Percent in Fourth Quarter of 2013

Alcoa Posts $2.3-Billion Loss in Fourth Quarter on Write-Downs

Infosys Q3 surprises D-Street; Five Factors That Could Make Infosys Stock Rally

Is Uber’s Surge-Pricing an Example of High-Tech Gouging?

Overstock Accepts Bitcoin Now – But Doesn’t Keep Them

Edward Harrison: Why T-Mobile’s John Legere Will Continue to Shake Up the Telecom Industry

Joshua Brown: Chart o’ the Day: A Technical Case for European Stocks

Be sure to follow me on Twitter.

-

We Need to See Some Heroic Entrepreneurs in the Movies

Posted by Eddy Elfenbein on January 9th, 2014 at 6:01 pmThe 86th Oscar nominations come out next week, and the early buzz is that “The Wolf of Wall Street” will be among the favorites for best picture, best director (Martin Scorsese) and best actor (Leonardo DiCaprio in the title role). Businessmen are usually villains in a Hollywood script. Rarely do we see entrepreneurs glorified in film. But as I look over my extensive data base of market history (as you may have noticed, I use history as a hook in GrowthMail), I visualize three movie script ideas from a century ago this week:

Three Movie Script Ideas from 100 Years Ago This Week

On Monday morning, January 5, 1914, an army of assembly line workers walked to their posts in Henry Ford’s Model T factory and found out that their pay envelope has doubled overnight, to $5 per day. What’s more, their day had been shortened to eight hours. Pinch me! I’m dreaming! A classic “robber baron” figured out that it was good business to treat his workers well. This way, he could insure that his best workers would not run to the competition with their best new ideas.

On Tuesday, January 6, 1914, Charles E. Merrill hung out a shingle on 7 Wall Street, “Charles E. Merrill & Co: Operations Department.” The sign lied: There was no company, only him, and no money, or Operations. His dream was to bring stock market investing to the masses, not just the well-heeled patricians of established wealth. Six months later, Edmund Lynch joined him, only to be told that the stock market would be closed “indefinitely” (for five months, as it turned out).

On Wednesday, January 7, 1914, the first steamboat passed through the new Panama Canal. It was a French crane boat called the Alexandre La Valley. For the previous 50 years, visionaries had dreamed of a route linking the Atlantic and Pacific, but it took a few bold men with grit – President Theodore Roosevelt, Army engineer George Washington Goethals and Army Doctor Walter Reed – to make this massive project possible, linking the world’s oceans for commerce.

Alas, none of these movies have been made, or will likely ever be made. When it comes to movies about making cars, “Tucker: A Man and His Dream” (1988), my favorite pro-business film, lost $4.3 million, while Oliver Stone’s assault on corruption in “Wall Street” (1987) tripled its costs in box office receipts.

As for the Panama Canal, I wonder if Dreamworks has enough special effects to make the danger and daring of that project as impressive as it was in fact. Read David McCullough’s 1977 award-winning book, “The Path between the Seas: The Creation of the Panama Canal, 1870-1914” to see what I mean. This year, the big dig continues, as the Canal widens to 180 feet (from 110) and deepens to 60 feet (from 42 feet) in depth, all in order to accommodate ships of up to 1200 feet in length, up from today’s 964 feet.

This leaves us with Charlie Merrill – the ideal hero for a populist movie about Wall Street’s marriage with Main Street. Mr. Merrill brought investing to the masses, starting 100 years ago, but it was a rocky road. Fortunately, a new book could serve as a guide for scriptwriters. It’s called “Catching Lightning in a Bottle: How Merrill Lynch Revolutionized the Financial World,” by Winthrop H. Smith, Jr., son of the last-named partner in the firm’s eventual name: “Merrill, Lynch, Pierce, Fenner and Smith.” The book has a sad ending, since Merrill lost its way in recent years, but its first 85 years deliver an inspiring tale.

Charlie Merrill’s Passion Can Still Work for the Average Investor

Charlie Merrill brought several innovations to Wall Street. One was to be customer-centered, by paying associates a salary instead of a commission; another was to broaden the reach of stock market investing to the common man; and a third goal was to reflect core values, etched into concrete in their headquarters building: “Client focus. Respect for the individual. Teamwork. Responsible citizenship. Integrity.”

The firm grew large, but its beginnings could not have been smaller. Charles E. Merrill, born October 19, 1885, in the suburbs of Jacksonville, Florida, arrived in Manhattan just as the Panic of 1907 began. He found and lost a number of jobs before 1914, when he set up shop on Wall Street. It was an uphill battle from the beginning. First, he borrowed $10 to take a businessman to lunch in order to offer 20% of his new (then worthless) company, in exchange for a $2 million capital loan. Along the way, Merrill always had a keen eye for value. For instance, he launched and ran the grocery chain, Safeway, in 1928, since he thought stocks had become too overvalued. In effect, he sat out the disastrous 1930s. He only returned to the brokerage business when Winthrop Smith, Sr., persuaded him to return in 1940. Merrill would only do so if the company committed to an advertising campaign to bring stock market investing to the masses.

The 1940s marked the optimum decade for buying stocks, but most Americans avoided stocks like the plague. In 1949, the Dow was still mired below 200 (50% below its 1929 peak, 20 years earlier). A 1949 Federal Reserve Board survey found that 69% of U.S. families with incomes over $3,000 a year were opposed to investing in stocks. Another 1949 survey found that 90% of the richest residents of St. Paul Minnesota had never purchased a share of stock in their lifetime. When most Americans heard the word “stock,” they thought of Chicago’s stockyards, not Wall Street’s brokerage firms. Merrill changed that.

Merrill bemoaned the fact that Americans spent $9 billion a year on cars but just $540 million on stocks, so Merrill – more than anyone else – turned the tide of public sentiment. His 1949 newspaper ads targeted women who’d “like to know more about investments.” (Merrill always had a way with the ladies!) With that single ad, he lured 30,000 into an eight-week course, despite widespread fears over the dangers of stock market investing. Later, he invited both husbands and wives to the same forum, so that both would be involved with their family’s financial future. His seminars advocated dollar-cost averaging of as little as $40 per month. Merrill also set up tents at agricultural fairs and converted buses into “stock-mobiles.”

As a result of Merrill’s efforts, the number of individual shareholders began to soar in the 1950s, growing by 10% a year, reaching 8.6 million in 1956, when Merrill died, He was “bullish on America” to the end.

The theme of the movie I have in mind is captured in The Economist’s review of Smith’s new book: “When Finance was for the 99%.” Imagine a world in which only the stuffed-shirt rich invest in stocks. Along comes a kid with an “Occupy Wall Street” mentality. He sets up a kiosk in the middle of Grand Central Station, showing off a stream of stock price to passing commuters. (Yes, Charlie did that!) By luring working stiffs to his stock seminars, he lifted some of the 99% to the ranks of the top 10%.

Former SEC chairman Arthur Levitt has said that Merrill Lynch was the only Wall Street firm with a “soul,” by which he undoubtedly meant its 10-word credo. But Win Smith, Jr., said the company began to lose its soul in the late 1990s, particularly after 9/11, when the board and CEO Stanley O’Neal began investing heavily in risky subprime debt, closing international operations, and firing 24,000 associates.

There is a happy ending. Two of Winthrop Smith Jr’s nephews work at Bank of America Merrill Lynch and say they were taught the old ways of putting customers first. That would make for a great final reel.

Another Great Pro-Business Film Idea from 125 Years Ago This Week

Not all businesses succeed, of course. As 1889 dawned, world-famous author Mark Twain touted, and invested in, a revolutionary new automatic typewriter called the Paige Compositor, while a Census clerk, a former engineering professor, fiddled with some punched cards in order to streamline the 1890 Census.

Here are the facts: On Saturday, January 5, 1889, Mark Twain wrote in his diary: “EUREKA! I have seen a line of movable type, spaced and justified by machinery!” He invested his life savings in the Paige Compositor, a machine that he said would make older inventions – like the phone or locomotives – “mere toys, simplicities.” Twain invested $300,000 to take over full ownership of the firm, which was under the scientific direction of James W. Paige, whom Twain called “a Shakespeare of mechanical invention.”

Before we check on the success of the Paige Compositor, let us switch frames to the workshop of Herman Hollerith. On Tuesday, January 8, 1889 – 125 years ago tomorrow – Hollerith was granted a patent for his electric tabulating machine – something like a punched-card calculator. The Hollerith system was first used to count heads in the Census of 1890. Hollerith then formed the Tabulating Machine Co., which in 1911 became the Computing Tabulating Recording Company, which, starting in 1914, Thomas Watson turned into International Business Machines (IBM), one of the greatest corporations of the 20th Century.

Meanwhile, the Paige Compositor proved to be too temperamental to handle rough print shop work. The more rough-and-ready Linotype won the race to commercial dominance in type-setting. Mark Twain was driven into bankruptcy in 1894 after losing $300,000. The good news is that he had to go back to writing for a living. In 1894, he wrote “Pudd’nhead Wilson,” which includes these painful investment lessons:

“Behold, the fool saith, ‘Put not all thine eggs in the one basket’ – which is but a matter of saying, ‘Scatter your money and your attention’; but the wise man saith, ‘Put all your eggs in the one basket and – WATCH THAT BASKET.”

“October is one of the peculiarly dangerous months to speculate in stocks. The others are July, January, September, April, November, May, March, June, December, August, and February.”

“The holy passion of Friendship is of so sweet and steady and loyal and enduring a nature that it will last through a whole lifetime, if not asked to lend money.” – All quotes are from “Pudd’nhead Wilson,” 1894.

– Gary Alexander

Navellier Marketmail -

Ford Raises Dividend By 25%

Posted by Eddy Elfenbein on January 9th, 2014 at 10:31 amGood news from Ford ($F). The automaker sweetened its dividend by 25%. The quarterly dividend will rise from 10 cents to 12.5 cents per share. That’s 50 cents on the year.

Ford said its dividend increase reflects strong 2013 performance and its plans going forward and is consistent with the company’s One Ford goal of delivering profitable growth for all stakeholders.

“Our capital strategy continues to be focused on financing our One Ford plan, further strengthening our balance sheet and providing attractive returns to our shareholders,” said Bob Shanks, chief financial officer, Ford Motor Company. “This increase in the dividend provides our shareholders with a regular, growing dividend that we believe is sustainable over an economic or business cycle.”

Through the first three quarters of 2013, Ford increased its liquidity position by $3 billion and has extended to 14 the number of consecutive quarters of positive Automotive operating-related cash flow.

Two years ago, Ford restored its dividend at five cents. Last year, they doubled it to ten cents, and now we’re at 12.5 cents. The stock closed yesterday at $15.54, so the new dividend works out to a yield of 3.22%. Shares of Ford are currently up about 2% today.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His