-

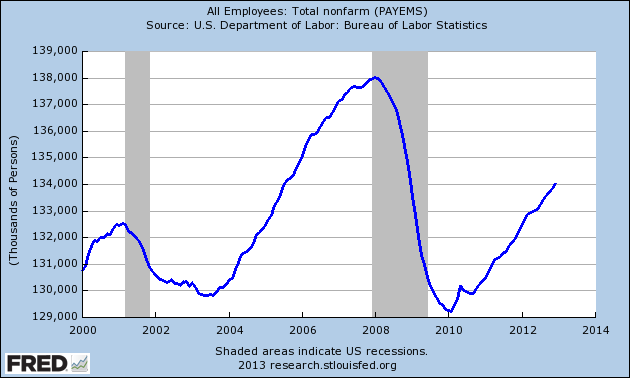

December NFP +155,000

Posted by Eddy Elfenbein on January 4th, 2013 at 9:39 amKind of a boring jobs report. The economy created 155,000 jobs last month which was very close to expectations. The unemployment rate ticked up to 7.8%. It was just 2,000 jobs away from rounding up to 7.9%. The price of gold has dropped to a four-month low.

The details of the report paint a similarly solid but uninspiring picture. The unemployment rate was driven by a combination of more people entering the labor force, 192,000 of them, a gain not matched by the number of people reporting having a job. If that pattern were to continue, it would eventually push the jobless rate up even as employers create new positions. A broader measure of unemployment that captures people working part time who want a full-time job and those who have given up looking for work out of frustration was unchanged at 14.4 percent.

The employment gains were relatively broad, with an 25,000 rise in manufacturing employment and a welcome 30,000 gain in construction jobs. Those might, in part, reflect a ramp-up in activity to rebuild following Hurricane Sandy, but the construction gain in particular is a welcome change after months in which the sectors job tally hasn’t kept up with a rise in homebuilding.

-

CWS Market Review – January 4, 2013

Posted by Eddy Elfenbein on January 4th, 2013 at 8:17 am“You get recessions, you have stock market declines. If you don’t understand

that’s going to happen, then you’re not ready, you won’t do well in the markets.”

– Peter LynchHappy New Year! This has been an exciting week: the Fiscal Cliff is done and gone, stocks are near multi-year highs and our Buy List officially beat the market for the sixth year in a row!

For the last several weeks, I’ve been telling investors not to get caught up in all the ridiculous hype surrounding the Fiscal Cliff. What else can I say but that the financial media behaved irresponsibly in stoking the fears of this manufactured crisis? Congress was even worse. At some point, I believed, a deal would be reached—and that’s exactly what happened.

The market celebrated the deal on Wednesday with its strongest rally in more than a year. In just two days, the Volatility Index ($VIX), also known as the Fear Index, plunged by one-third, and the S&P 500 made back everything it had lost since mid-October. Before a late-day sell-off on Thursday, the index was flirting with its highest close since 2007. On top of that, our 2013 Buy List has already grabbed a slight lead over the S&P 500.

It’s times like this I’m glad we’re long-term investors. I can’t imagine what it’s like trading through all these vacuous pronouncements during the Fiscal Cliff debate. The math is still very much on the side of stocks. Six weeks ago, I told you I thought the S&P 500 would break 1,500 sometime early this year. At the time, that seemed like a bold forecast. Now it looks more like a cakewalk. The index is currently less than 3% away from topping 1,500.

In this week’s CWS Market Review, we’ll take a look at what’s driving the current rally. Plus, Q4 earnings season is only days away and I’m expecting solid results from our Buy List stocks. In fact, one of the newbies on our Buy List is already making waves. Ross Stores ($ROST) soared 8% on Thursday on higher earnings guidance! This came exactly one day after an analyst at Citigroup downgraded Ross. Now let’s take a look at the current market.

The High-Beta Rally

The big two-day surge we just had was interesting because it comprised the final trading day of one year and the opening day of the next. This past December 31st was the single-best final-day gain since 1974.

But this hasn’t been a standard rally. It’s been what traders call a “high-beta” rally. These are rallies that have concentrated on the most volatile stocks (or more technically, it’s correlated volatility). That’s why we’ve seen small-cap stocks and tech stocks do the best. The Russell 2000 ($RUT), which is a widely-followed index of small-cap stocks, just broke out to a new all-time high. The Equal Weighted version of the S&P 500 also hit an all-time high. The regular S&P 500 is weighted by market cap, so the mega-caps, which have been lagging of late, have greater weight.

Here’s a chart showing a High-Beta ETF ($SPHB) compared with the S&P 500, and you can see that’s been crushing the market lately.

Cyclical stocks also tend to do well during high-beta rallies. In essence, what the market is doing is shifting towards riskier assets. This is good news because investors need to be rewarded for being willing to shoulder more risk. It’s the willingness to put your money down that helps the entire economy move along. The move has been slow, but the market is becoming more risk-friendly. High-yield spreads, for example, are at an 18-month low, and high-dividend stocks were laggards in 2012.

When the world economy went kablooey a couple of years ago, everyone ran screaming to the most secure assets. Gold and U.S. Treasuries soared as stocks and junk bonds plunged into the abyss. Banks and businesses just sat on their cash. But a major turning point came last summer when Mario Draghi made his now-famous statement: “Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.” My friends, that’s what we call a game-changer.

Even though this was an announcement from a European central banker, it sent shock waves around the world, and investors here in the U.S. took this as a signal to move towards risk. When I use the word “risk” here I don’t mean to use it with the negative connotations of recklessness or imprudence. Rather, I mean areas that have a longer time horizon to pay off. For example, I have a pretty good idea where Treasury bill yields will be in a week, but I have no idea what AFLAC’s ($AFL) stock will do. Yet over the next, say, two or three years, I have a very high level of confidence that AFLAC will still be pulling down a sizeable profit despite a fluctuating stock market. The latter investment simply needs more time to pay off.

I should also point out that it isn’t so much that investors are becoming riskier. Instead, it’s that investors are moving from a state of extreme risk-phobia to a more normal state of affairs. The day before Dragi’s statement, the yield on 10-year Treasury bonds hit an historic low of 1.4%. Since then, they’ve soared all the way to a still-puny 1.9%. Put it this way: Microsoft ($MSFT), which is a new member of the Buy List, is one of the largest and best-known blue chips stocks in the world, yet its yield is nearly double that of the 10-year.

The rotation towards risk got another big boost a few weeks after Draghi’s announcement when the Federal Reserve said it would pursue its QE Infinity policy. I should add that I was completely and totally wrong about this announcement. For weeks beforehand, I had said that the Fed was in no way pursing such a policy. Shows what I know!

Fortunately, our Buy List was perfectly poised to ride the market’s rotation. One great example is Ford Motor ($F). In the CWS Market Review from August 24th, I highlighted Ford as a good bargain. I wrote: “I don’t see how the stock can go for less than $10, but it is.” Just a few days before I wrote that, I remember that Ford had even dropped below $9. But patience once again paid off for us. Yesterday, shares of Ford got as high as $13.70. The stock is up more than 52% from its summer low.

The company just announced that December sales rose 1.9%. It was Ford’s best December since 2006. Look for another solid earnings report later this month. Ford remains an excellent buy up to $15 per share.

Ross Stores Soar 8% on Higher Guidance

One of the new stocks on this year’s Buy List is Ross Stores ($ROST). This is a very solid retailer. On Thursday, one day after an analyst at Citigroup downgraded the stock, ROST reported outstanding sales and guided higher for Q4. December sales rose 11% to $1.276 billion.

The key metric for a retailer is comparable-store sales. Wall Street was expecting ROST to report an increase of 2.7%. Instead, it was 6%. The company also raised its earnings guidance for Q4 (which ends in one month). Before, Ross was expecting earnings of 99 cents to $1.04 per share. Now they expect earnings of $1.04 to $1.05 per share. Ross expects comparable-store sales to rise between 1% and 2% for January. This is excellent news. The shares gapped up 7.97% on Thursday to close at $58.78. Thanks to the rally, I’m raising my Buy Below on Ross to $62 per share. Expect to see their 19th-straight annual dividend increase in a few weeks.

Before I go, I want to point out some good bargains on the Buy List. Bed Bath & Beyond ($BBBY) has dropped down recently. My Buy Below price is currently $60, but if you can get BBBY below $57, that’s a really good deal for the long-term. CA Technologies ($CA) is pretty cheap. At its price, CA yields 4.42%. Also, Microsoft ($MSFT) continues to be the stock everyone loves to hate, but it looks very attractive below $28 per share. Actually, one of the reasons why I like it is that everyone else hates it so much. MSFT currently yields 3.38%.

That’s all for now. Earnings season starts next week. Our first Buy List stock to report will be Wells Fargo ($WFC) on Friday, January 11th. Wall Street currently expects 90 cents per share, which sounds about right. Wells is a good buy up to $37. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. It’s official. I’m very happy to report that our Buy List beat the S&P 500 for the sixth year in a row in 2012. The 20 stocks on the Crossing Wall Street Buy List gained 14.56%, while the S&P gained 13.41%. Including dividends, our Buy List gained 17.85%, compared with 16.00% for the S&P.

-

Morning News: January 4, 2013

Posted by Eddy Elfenbein on January 4th, 2013 at 7:15 amMost European Stocks Fall as Fed Considers Stimulus Cut

Euro-Area Consumer Prices Rise More Than Estimated on Food

Shock Fall In UK Services Activity Raises Recession Fears

Dollar Climbs to 29-Month High vs. Yen as U.S. Interest Rates Rise

U.S. Jobless Claims Rise 10,000 To 372,000

A Victory for Google as F.T.C. Takes No Formal Steps

Barnes & Noble Holiday Sales Decline on Nook Devices

Transocean $1.4 Billion Gulf Spill Deal Lures Investors

JMP Securities Upgrades Bank of America to Market Perform (BAC)

Hormel to Buy Skippy Peanut Butter

BMW Tops Mercedes as U.S. Auto Sales Highest Since 2007

7 ETFs To Be Excited For In 2013

Swiss Bank Wegelin & Co. Pleads Guilty in U.S. Tax Probe

Jeff Carter: Seed Round Financing: Why Crowdfunding Will Be Challenging

Be sure to follow me on Twitter.

-

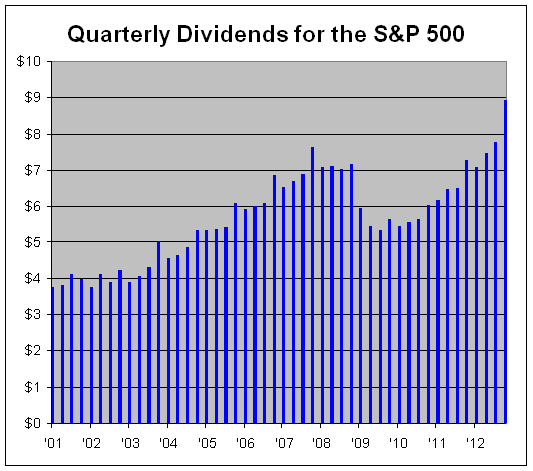

Dividend Growth Soars 22.8% in Q4

Posted by Eddy Elfenbein on January 3rd, 2013 at 2:14 pmThanks to higher profits and special dividends, quarterly dividends for the S&P 500 jumped 22.77% in the fourth quarter. All told, the S&P 500 paid out $8.93 in dividends (that’s just to the index).

For the year, the S&P 500 paid out $31.25. To add some context, that means that the index yields 4.6% for investors who bought at the March 2009 low.

Dividends have been hot recently. Consider that dividends grew 18.2% last year which followed a 16.3% increase in 2011.

-

Mic’d Up RGIII

Posted by Eddy Elfenbein on January 3rd, 2013 at 12:43 pmI don’t how to embed this, but here’s amazing video of a mic’d up RGIII during the Redskins’ win over the Cowboys. Trust me, it’s very cool.

-

Ross Stores Soars 7%

Posted by Eddy Elfenbein on January 3rd, 2013 at 11:01 amThe stock market opened 2013 with a strong day yesterday. In two days, the S&P 500 gained back everything it lost since mid-October. Today so far, the market is down just a bit.

Retail stocks are having a very good day as many are reporting strong holiday sales figures. In fact, we already have a star stock this year as Ross Stores ($ROST) has gained 7% today. The company raised its fourth-quarter profit estimate to a range of $1.05 to $1.06 per share from the earlier range of 99 cents to $1.04 per share. Comparable same-store sales rose 6% which was far more than the 2.7% analysts were expecting.

Right after breaking $13, Ford Motor ($F) has motored above $13.50. The company said today that its U.S. sales rose 1.9% in December.

The Labor Department reported that unemployment claims rose to 372,000. That’s an increase of 10,000 from last week’s revised number of 362,000. Technically, this report was worse than expected (Wall Street’s consensus was for 360,000), but everyone is focused on the big jobs report for tomorrow. The ADP report, which is done by a private payroll firm, showed an increase of 215,000 jobs. According to ADP, private employers added 1.7 million jobs in the last year.

Wall Street’s consensus for tomorrow’s jobs report is a gain of 157,000.

-

Morning News: January 3, 2013

Posted by Eddy Elfenbein on January 3rd, 2013 at 7:19 amSome Breaks for Industries Are Retained in Fiscal Deal

Moody’s Says ‘Fiscal Cliff’ Deal Doesn’t End Credit Downgrade Risk

Dollar Rises As U.S. Budget Deal Optimism Wanes

CEOs Pan Fiscal Cliff Deal, Vow to Continue Debt Fight

Basel Becomes Babel as Conflicting Rules Undermine Safety

UK Construction Hits a Six-Month Low

Spain Sees Jobless Total Fall In December

Al Jazeera Seeks a U.S. Voice Where Gore Failed

China Poised for 2013 Rebound as Debt Risks Rise for Xi

Global Natural Catastrophe Losses Fell in 2012, Munich Re Says

Avis Will Buy Zipcar For $500 Million

Starbucks to Open First Store in Vietnam

Google Said Poised to Resolve FTC Antitrust Probe Today

Jeff Miller: Analyzing the Fiscal Cliff Outcome

Stone Street: Down So Long It Looks Up – Zipcar

Be sure to follow me on Twitter.

-

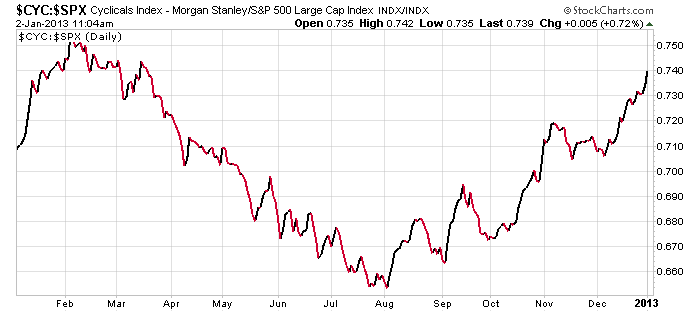

Cyclicals Continue to Lead

Posted by Eddy Elfenbein on January 2nd, 2013 at 11:08 amHere’s a look at the Morgan Stanley Cyclical Index ($CYC) relative to the S&P 500.

The cyclicals grabbed the lead right after Mario Draghi said that the ECB would do “whatever it takes” to save the euro. As I said before, today is a high-beta rally. The Russell 2000 ($RUT) and the Equal Weight S&P 500 are at all-time highs.

-

2013 Is Off to a Strong Start

Posted by Eddy Elfenbein on January 2nd, 2013 at 10:52 amFor the last few weeks I’ve cautioned investors to ignore the hype about the Fiscal Cliff. Eventually, I believed, some deal would be reached, and late last night, that’s exactly what happened. Here are the details.

It wasn’t pretty and not everybody got what they wanted, but compromise is the cornerstone of democracy. Plus, there will be more battles ahead on the debt ceiling.

The good news is that the markets are responding very well this morning. The S&P 500 has been as high as 1,457.53 this morning. That’s a 2.2% jump and it brings the index just eight points shy of its highest close since 2007. On our Buy List, Oracle ($ORCL) is up to an 18-month high this morning.

Today’s rally is what’s called a high-beta rally which means that the leaders are small-cap stocks plus industries like tech (like Oracle), finance and cyclicals. High-beta rallies usually (but not always) tend to pull along lower-quality stocks with them. There are lots of sketchy names among small-cap tech stocks. Since our Buy List is concentrated among high-quality stocks, we tend to lag the broader markets on days like this. The Russell 2000, which is a popular index of the small-cap sector, is up to an all-time high this morning.

Still, our Buy List is beginning 2013 on a strong note. Every stock but Ross Stores ($ROST) is higher today. I was pleased to see that CR Bard ($BCR) was upgraded by JPMorgan today. (The Buy List is so new I haven’t had time to enter in comments for the new additions. I’d better get on that.)

On the economic front, the ISM Index for December rose to 50.7. If you recall, the number for November was 49.5 which was a dud. Any reading above 50 means the manufacturing sector is expanding. Below 50 means it’s shrinking. The worry zone doesn’t really kick in until the ISM drops to 45 or so. The next big report will be Friday’s jobs report.

-

Morning News: January 2, 2013

Posted by Eddy Elfenbein on January 2nd, 2013 at 6:49 amU.S. Fiscal Cliff Deal Prompts Broad Global Market Rally

Bipartisan House Backs Tax Deal Vote as Next Fight Looms

Bond Tab for Biggest Economies Seen Falling $220 Billion

Senate Plan Undoes Most of $600 Billion in Budget Changes

Euro-Zone Manufacturing Shrinks in December

Macau Casinos End Year on a High

Malls Blossom in Russia, With a Middle Class

Tech Giants Brace for More Scrutiny From Regulators

Arcelormittal To Sell $1.1bln Stake In Canadian Unit

Hyundai, Kia Forecast Slowest Growth in Seven Years

Middleby Buys Appliance Maker Viking For $380 Million

Buffett Combines BofA With Buybacks to Beat S&P 500

Crime Forfeiture Pays for U.S. Attorney’s Office (Sometimes in Dinosaur Bones)

Joshua Brown: Binary Sunset, Revisited

Phil Pearlman: Crushing It Is a Process

Be sure to follow me on Twitter.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His