Archive for 2013

-

Morning News: February 14, 2013

Eddy Elfenbein, February 14th, 2013 at 7:20 amEuro Zone 2012: Not a Single Quarter Showing Economic Growth

BOJ Chief Defends Policy Ahead Of G20 As Economy Contracts

Indian Inflation Slows to 38-Month Low; Boosts Rate-Cut Case

BNP Paribas Begins Overhaul After Fourth-Quarter Profit Drop

Obama Bid for Europe Trade Pact Stirs Hope on Both Sides

Calmly, Pick for Treasury Offers Replies to Senators

401(k) Balances Reached Record on 2012 Stock Market Rally

Small Businesses Still Struggle, and That’s Impeding a Recovery

American and US Airways Announce $11 Billion Merger Deal

Citigroup Lost $15 Million With UBS’s ‘Crap’ CDO Blessed by S&P

Cisco Forecasts Sales That Miss Some Analysts’ Estimates

Rio Tinto’s New CEO Vows Cost Cuts And Disposals

India’s Tata Motors Q3 Net Profit Halves, JLR Margin Sags

Groupon Surges on Expected E-Commerce Expansion

Credit Writedowns: Japanese RORO

Roger Nusbaum: Not All Stock Picking is Wildly Complex

Be sure to follow me on Twitter.

-

11 Stocks to Sell Right Now

Eddy Elfenbein, February 13th, 2013 at 12:01 pmHere’s a list of 11 stocks that investors should sell as soon as possible. I’ve included yesterday’s closing price for future reference.

Company Symbol Close 2/12/2013 TiVo TIVO $13.15 Forest Labs FRX $35.74 salesforce.com CRM $172.36 Netflix NFLX $177.95 Amazon.com AMZN $258.70 Zillow Z $36.15 Red Hat RHT $55.33 Weyerhaeuser WY $30.31 Iron Mountain IRM $34.47 iRobot IRBT $21.41 HomeAway AWAY $24.83 January Retail Sales +0.1%

Eddy Elfenbein, February 13th, 2013 at 10:05 amThe Commerce Department reported that retail sales rose by just 0.1% last month. That’s not very strong, but part of the problem was that higher taxes took a bite out of consumers. Still, the report was inline with what economists were expecting.

Economists also like to look at “core sales,” which is retail sales excluding cars, gas and building materials. In others words, they want to focus on basic consumer spending habits. For January, core sales also rose by 0.1%.

Even though the Q4 GDP report was rather poor, economists were impressed by the strength of consumer spending. That’s why people are interested to see if that trend is holding up into Q1. This is especially important for our retail stocks like Bed, Bath & Beyond ($BBBY) and Ross Stores ($ROST). If you recall, Ross recently said they had pretty good sales for January.

I should add that the Q4 GDP report will probably be revised higher thanks to the recent trade report. In fact, it will most likely go from being a negative number to a positive one.

The outlook in Europe got a boost this morning when the industrial production number came in at 0.7% growth which was better than the 0.2% that was expected.

In the U.S. market, the Volatility Index ($VIX) is close to hitting a six-year low today. If this keeps up, we might have to change the name from the VIX to the NIX. The VIX closed yesterday at 12.64 while the low is 12.29 from January 18th. The last time we were that low was February 27, 2007 which was the start of the financial crisis.

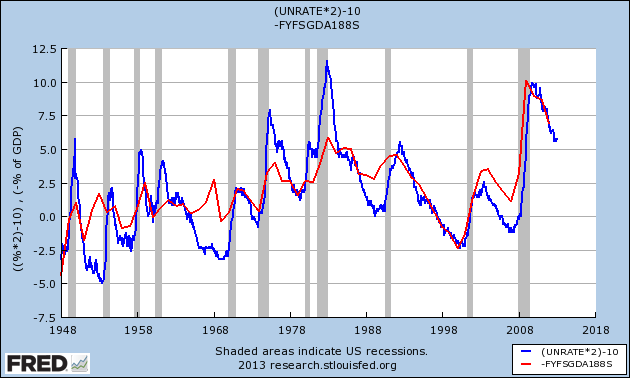

My Simple Rule for Government Financing

Eddy Elfenbein, February 13th, 2013 at 9:43 amAs part of my continuing effort to solve all of the world’s problems, I’ve devised a simple rule for the U.S. budget deficit. Here it is:

(Unemployment Rate x 2) – 10 = Budget Deficit / GDP

Here’s how my rule has held up (in blue) against the real budget deficit (in red).

Morning News: February 13, 2013

Eddy Elfenbein, February 13th, 2013 at 7:20 amBoE Will Tolerate Inflation To Aid Growth

G-7 Roils Currency Markets With Split on Yen Views

Wheat Falls to Seven-Month Low as Rain in Plains May Boost Crop

Obama Paints Wider Role for Government in Middle Class Revival

Raising Minimum Wage Would Ease Income Gap but Carries Political Risks

Silicon Valley and Immigrant Groups Find Common Cause

Small-Business Optimism in U.S. Improves for Second Month

Comcast Buys Rest of NBC’s Parent

ING Cutting 2,400 Jobs as Quarterly Profit Misses Estimates

Peugeot Citroën Reports Record Loss

Big Investors Stiffen Their Resistance to Dell’s Offer

Apple Said to Have Team Developing Wristwatch Computer

Pragmatic Capitalism: Market Volatility and Returns

Joshua Brown: begging your pardon…

Be sure to follow me on Twitter.

The Yen Drag

Eddy Elfenbein, February 12th, 2013 at 7:07 pmI thought this chart was interesting. It shows how much better the Nikkei Index has done than the iShares MSCI Japan Index ($EWJ) which is, of course, denominated in dollars. Japanese stocks are indeed doing well but devaluation explains some of it, though not all of it.

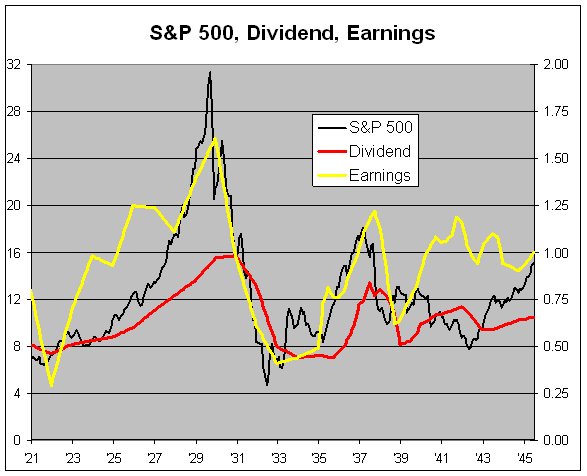

How Overpriced Were Stocks in 1929?

Eddy Elfenbein, February 12th, 2013 at 10:46 amScott Sumner recently wrote, “studies have shown that stocks were not overpriced in 1929.” This observation surprises many people. They’ve been led to assume to stocks were wildly overvalued in 1929, but carefully looking at the evidence shows that that really isn’t the case.

While stocks did soar during the 1920s, so did earnings and dividends. Stocks exploded higher in 1929, especially after April. The Federal Reserve also stepped in by raising rates a few times.

The chart above is from data from Robert Shiller’s website. The S&P 500 is the black line and it follows the left scale. The one-year trailing earnings and dividends follow the right scale. The lines are scaled at a ratio of 16-to-1, so whenever the lines cross, the earnings multiple is exactly 16 or the dividend yield is 6.25%.

I think a good way to view bear markets is to divide them into two categories. One is when prices far overshoot fundamentals. The other is when fundamentals crumble beneath prices; 1987 and 2000 are examples of the former, 1990 and 2007 are examples of the latter. I would say that 1929 is another good example of fundamentals falling apart beneath prices. So were stock prices overvalued in 1929? I think it’s fair to say that stock prices became “elevated,” but I don’t believe it was anything truly excessive.

According to the monthly Shiller data, the peak P/E Ratio, based on one-year trailing earnings, was 20.2 in September 1929. That’s high but hardly out of orbit. The dividend yield for September was 3%.

Bear in mind that I’m speaking from the standpoint of an investor at the time. Of course, investors then wouldn’t have known that the Federal Reserve engaged in an historic blunder by tightening as things got worse which, in turn, made things even worse. But for a person in 1929, there was little reason to believe that stock prices had reached the moon. In early 2000, by contrast, it was quite obvious that tech stocks bore little relation to their long-term value. They were going up simply because they were going up. As Herb Stein said about unsustainable trends, they eventually come to an end.

Let me add that any look at the market’s value is inherently subjective. There’s no one perfect measure of something’s worth. After all, if there were one, we wouldn’t need markets. In the end, something is worth how much someone else is willing to pay for it. So I’m not saying stocks were perfectly valued or undervalued in late 1929. I’m saying that there was no obvious signal at the time that stocks were overvalued.

That brings me to Robert Shiller’s CAPE, which is the Cyclically Adjusted Price/Earnings Ratio. That’s the P/E Ratio but based on the average of the last 10 years’ worth of earnings. As I’ve written before, I’m not a fan of CAPE. The issue for me is that stock valuations are inherently cyclical so there’s no need to adjust them for a cycle. With the 1929 example, we can really see the weakness of CAPE.

The problem is that 10 years prior to 1929, the earnings denominator included the earnings plunge of the early 1920s. That really weighs down the data and thereby elevates CAPE. On the chart, notice how earnings dropped below dividends which is a good sign that the data is a bit messy. If the CAPE were five years instead of 10, the picture would look much different. I used one-year data in my chart which I think gives us a better picture of what was truly happening.

Historically, CAPE doesn’t have a great track record. It showed that stocks were rather high in 1995 at the start of the bull market, and it showed that prices were fairly valued only weeks after the March 2009 low.

Recently I wrote about the little-appreciated bull market of 1949-55. I think it’s ignored because it didn’t come to a crashing end. The 1929 market gets the opposite effect. Because it came to a crashing end, people assume stocks were outrageously priced. The ultimate judge of a market shouldn’t be what comes after.

Morning News: February 12, 2013

Eddy Elfenbein, February 12th, 2013 at 7:00 amWorld Bank Chief Economist Calls On G20 To Coordinate Policies

G-7 Won’t Target Exchange Rates Amid Currency War Concern

ECB Ready to Offset Banks’ Accelerated LTRO Payback

U.K. Inflation Stays at 2.7% as Price Pressures Mount

Buyout-Boom Shakeout Seen Leaving One in Four to Starve

Corn Heads for Longest Losing Run Since 2010 as Output May Climb

Yellen Says Higher Rates Not Assured After Thresholds Hit

Karen Mills to step down as head of Small Business Administration

Barclays Posts $1.3 Billion Loss and Plans to Cut 3,700 Jobs

Shell Vessels Sidelined, Imperiling Arctic Plans

Hostess Gets Approval to Auction Twinkies, Drake’s Brands

UK Fines UBS $15 Million For Failings In AIG Fund Sale

Samsung Girds for Life After Apple in Disruption Devotion

Howard Lindzon: Momentum Monday…The Magic Behind LinkedIn and Tesla Motors

John Hempton: Another Day – Another Strange Gulfport Energy Related Party Transaction

Be sure to follow me on Twitter.

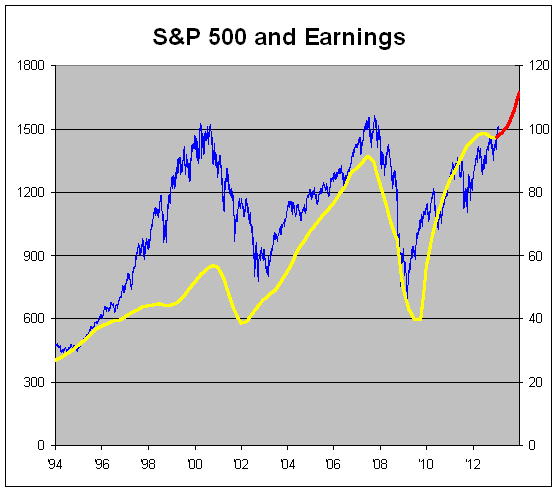

About That Earnings Acceleration….

Eddy Elfenbein, February 11th, 2013 at 2:28 pmOne aspect of this market that I’m starting to strongly doubt is the belief that earnings growth is about to ramp up. In other words, the rate of growth will itself increase.

The chart below shows the S&P 500 (blue line, left scale) along with its earnings (yellow line, right scale). The red line is Wall Street’s forecast (please note: it’s not my forecast, it’s Wall Street’s consensus). The lines are scaled at a ratio of 15-to-1 so whenever the lines cross, the P/E Ratio is exactly 15.

It’s that red line that has me concerned. Wall Street seems to believe it’s about to hook upward. Me? I’m not so sure. For one, profit margins have been pushed about as far as they can go. I can believe that nominal GDP growth will pick up, but nothing close to what would sustain a major bounce in corporate earnings.

The Street currently sees full-year earnings for the S&P 500 coming in at $111. That’s down from $117 ten months ago. Earnings growth was actually negative for Q3 and Q4 of 2012. Unless we see evidence of an earnings pickup for Q1 2013, I’m inclined to believe the market will earn $100 for all of 2013.

Is the yellow line going through a minor bump like it did in 1998, or is it hitting a major peak like 2000 and 2007? I should add that if the earnings projections are correct, the S&P 500 is very undervalued here.

Stocks Go for Seven Straight Up Weeks

Eddy Elfenbein, February 11th, 2013 at 1:04 pmThe stock market has now risen for six weeks in a row, and today we’re trying to make it seven. Right now, stocks are mostly unchanged. The S&P 500 is down a bit, but it’s nothing too serious. Just listening to the chatter, it seems like everyone is expecting a pullback to happen at some point. Just when and how much are the only missing pieces.

There’s a big euro meeting today to discuss what to do over Cyprus and Greece. Then on Friday, the G-20 finance chiefs gather for a meeting in Moscow. The big political item this week will be tomorrow’s State of the Union by address by President Obama. It’s expected that he’ll offer specific proposals about gun control and immigration.

The next earnings report from one of the stocks on the Buy List will be DirecTV ($DTV) which is due to report on Thursday. Wall Street expects earnings of $1.13 per share. Also on our Buy List, Medtronic ($MDT) made a fresh 52-week high.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His