-

Today’s Fed Statement: More Tapering

Posted by Eddy Elfenbein on January 29th, 2014 at 2:02 pmInformation received since the Federal Open Market Committee met in December indicates that growth in economic activity picked up in recent quarters. Labor market indicators were mixed but on balance showed further improvement. The unemployment rate declined but remains elevated. Household spending and business fixed investment advanced more quickly in recent months, while the recovery in the housing sector slowed somewhat. Fiscal policy is restraining economic growth, although the extent of restraint is diminishing. Inflation has been running below the Committee’s longer-run objective, but longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace and the unemployment rate will gradually decline toward levels the Committee judges consistent with its dual mandate. The Committee sees the risks to the outlook for the economy and the labor market as having become more nearly balanced. The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, and it is monitoring inflation developments carefully for evidence that inflation will move back toward its objective over the medium term.

Taking into account the extent of federal fiscal retrenchment since the inception of its current asset purchase program, the Committee continues to see the improvement in economic activity and labor market conditions over that period as consistent with growing underlying strength in the broader economy. In light of the cumulative progress toward maximum employment and the improvement in the outlook for labor market conditions, the Committee decided to make a further measured reduction in the pace of its asset purchases. Beginning in February, the Committee will add to its holdings of agency mortgage-backed securities at a pace of $30 billion per month rather than $35 billion per month, and will add to its holdings of longer-term Treasury securities at a pace of $35 billion per month rather than $40 billion per month. The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. The Committee’s sizable and still-increasing holdings of longer-term securities should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative, which in turn should promote a stronger economic recovery and help to ensure that inflation, over time, is at the rate most consistent with the Committee’s dual mandate.

The Committee will closely monitor incoming information on economic and financial developments in coming months and will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability. If incoming information broadly supports the Committee’s expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective, the Committee will likely reduce the pace of asset purchases in further measured steps at future meetings. However, asset purchases are not on a preset course, and the Committee’s decisions about their pace will remain contingent on the Committee’s outlook for the labor market and inflation as well as its assessment of the likely efficacy and costs of such purchases.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens. The Committee also reaffirmed its expectation that the current exceptionally low target range for the federal funds rate of 0 to 1/4 percent will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. In determining how long to maintain a highly accommodative stance of monetary policy, the Committee will also consider other information, including additional measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. The Committee continues to anticipate, based on its assessment of these factors, that it likely will be appropriate to maintain the current target range for the federal funds rate well past the time that the unemployment rate declines below 6-1/2 percent, especially if projected inflation continues to run below the Committee’s 2 percent longer-run goal. When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; Richard W. Fisher; Narayana Kocherlakota; Sandra Pianalto; Charles I. Plosser; Jerome H. Powell; Jeremy C. Stein; Daniel K. Tarullo; and Janet L. Yellen

This is pretty much what I expected. The only minor surprise was that Narayana Kocherlakota didn’t dissent. Binyamin Appelbaum of the NYT tweeted: “Kocherlakota told me he would only dissent if he thought doing so would influence his colleagues. Apparently he decided it wouldn’t.”

-

Triumph Group Bombs

Posted by Eddy Elfenbein on January 29th, 2014 at 12:21 pmIn the CWS Market Review from December 27, I listed some of the finalists for this year’s Buy List. One of them was Triumph Group ($TGI), which is a maker of aerospace parts.

I’m glad we didn’t choose Triumph Group because it just bombed earnings. Earnings for Q4 came in 24 cents below expectations ($0.99 versus $1.23). Triumph also lowered this year’s guidance from $5.25 per share to $4.75 per share. The stock has been down as much as 19% today.

Triumph Group is a well-run company and I suspect they’ll come back. This is one to keep an eye on.

-

Morning News: January 29, 2014

Posted by Eddy Elfenbein on January 29th, 2014 at 6:40 amImpact of Turkey Rate Decision Fades Fast

EU Unveils Plan to Ban Banks’ Proprietary Trading

‘Fragile Five’ Is the Latest Club of Emerging Nations in Turmoil

Obama Seeks Trade Deals Sought by Biggest U.S. Companies

New York State Regulator Promises Tough Bitcoin Rules

LG Beats Its Rivals in Q4 Smartphone Sales

Pressure Builds for Apple to Overhaul or Expand Product Portfolio

Sony Credit Cut To Junk Status As Smartphones ‘Cannibalize’ Its TV And PC Businesses

American Airlines, US Airways Report Combined $1.95 Billion earnings for 2013

Fiat Scraps Dividend After Chrysler Buy

McDonald’s Seeks to Out-Latte Starbucks Amid Coffee Wars

Ford Posts Higher Profit But Faces Pressure in U.S.

Another Score for Crowdfunding: Indiegogo Raises $40 Million

Russia Bucks the Trend – Talks the Ruble Lower

Credit Writedowns: Turkey Moves, Focus Shifts to Fed

Be sure to follow me on Twitter.

-

MyRA

Posted by Eddy Elfenbein on January 28th, 2014 at 10:16 pmFrom President Obama’s State of the Union address:

Let’s do more to help Americans save for retirement. Today, most workers don’t have a pension. A Social Security check often isn’t enough on its own. And while the stock market has doubled over the last five years, that doesn’t help folks who don’t have 401ks. That’s why, tomorrow, I will direct the Treasury to create a new way for working Americans to start their own retirement savings: MyRA. It’s a new savings bond that encourages folks to build a nest egg. MyRA guarantees a decent return with no risk of losing what you put in. And if this Congress wants to help, work with me to fix an upside-down tax code that gives big tax breaks to help the wealthy save, but does little to nothing for middle-class Americans. Offer every American access to an automatic IRA on the job, so they can save at work just like everyone in this chamber can. And since the most important investment many families make is their home, send me legislation that protects taxpayers from footing the bill for a housing crisis ever again, and keeps the dream of homeownership alive for future generations of Americans.

I don’t know the details yet, but I’m having a hard time imagining what the benefits could be.

-

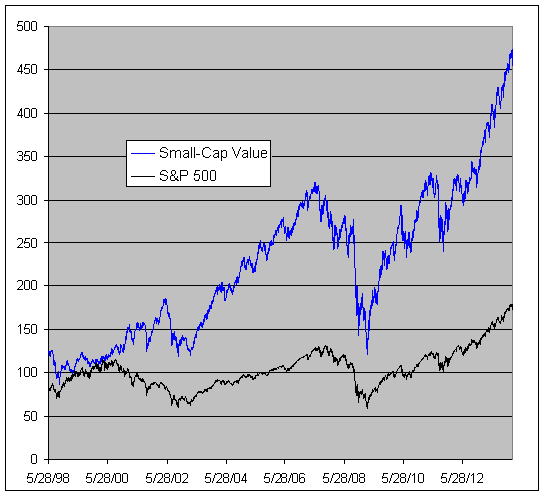

The Small-Cap Value Rally

Posted by Eddy Elfenbein on January 28th, 2014 at 4:05 pmIn reference to yesterday’s post on the small-cap premium, I want to look at the performance of small-cap value stocks compared with the rest of the market.

The difference is quite startling. This chart below has the Vanguard 500 Index Fund (VFINX) in black along with the Vanguard Small-Cap Value Index Fund ($VISVX) in blue. Both include dividends. I also set both funds to 100 on April 8, 1999, which was the start of small-cap outperformance.

-

Ford Beat by Three Cents per Share

Posted by Eddy Elfenbein on January 28th, 2014 at 10:52 amWe had more good earnings news today. Ford ($F) reported fourth-quarter earnings of 31 cents per share which was three cents better than estimates. In terms of net income, that’s a cool $3.04 billion. As usual, the company is doing well in North America. The F-Series trucks are very popular. For the 32nd year in a row, they were the top-selling vehicle in the U.S.

The weak spot continues to be Europe. True, the economy there is a bit of a wreck, but Ford needs to be stronger in that market. For the year, Ford lost $1.61 billion in Europe. They expect more losses this year, but a profit by 2015. Things are improving. Ford lost $571 million in Europe last quarter which is bad, but it’s better than the $732 million they lost in Q4 2012. Also, Ford had a small loss from Latin America and a small profit from Asia, but those are still pretty minor parts of their overall business.

Ford reiterated that profits will fall a bit this year ($8 billion to $7 billion pre-tax), but that’s because the company has very ambitious plans to roll out new models. Ford is introducing 23 new vehicles of which 16 are in North America. Overall, these were good results from Ford.

-

Morning News: January 28, 2014

Posted by Eddy Elfenbein on January 28th, 2014 at 6:47 amAsian Stocks Fall a Fourth Day Amid China, Fed Stimulus Concerns

Worried by EM Sell Off, Investors Seek Foothold in South Korea and Mexico

Calm Returns to Emerging Markets

RBI’s Dovish Outlook Soothes Bond Investors

U.K. 4Q GDP Grows 0.7%, Ending Best Year Since 2007

Bank of Montreal Parent Acquires British Asset Manager for $1.2 Billion

Why Nothing Apple Does Is Ever Good Enough

Ford Sets Profit Records in Key Markets Before Busy Year

DuPont 4th-Quarter Profit Doubles

Philips Q4 EBITA Beats Forecasts, Sees Tough 2014

Comcast Profit Rises 26% on Broad Sales Growth

Siemens Profit Rises as CEO Presses On With Cost Cuts

Bitcoin Executive Charlie Shrem is Accuse of Money Laundering

Markets, Herding and Avalanche Dynamics

John Hempton: When the Hedge Doesn’t Work

Be sure to follow me on Twitter.

-

Is There a Small-Cap Premium?

Posted by Eddy Elfenbein on January 27th, 2014 at 3:25 pmJosh Brown highlighted an interesting post by Alex Bryan at Morningstar, “Does the Small-Cap Premium Exist?”

Bryan touches on a few important points which I’ve long suspected. The long-term data suggests that small-cap stocks outperform their larger-cap bretheren.

This is a good example of the fact being true, but it needs more context. The outperformance of small-caps has historically been very erratic. We’ve gone for many years, decades in fact, with small-cap stocks underperforming.

The data also shows that most of the outperformance comes during the month of January. This is suspicious and it tells me that something else is going on. Perhaps beaten down small-caps are subjected to tax-loss selling.

Bryan notes that there hasn’t been a small-cap premium over the last 30 years, nor does it appear in other countries. He thinks that liquidity may have played a role in shaping the historical data, and that may not play such a large factor in the future.

I suspect that there is a small-cap premium but it’s very small and not very stable. I also think it’s more visible among small-cap value stocks than small-cap growth issues. There are lots of values to be found among small-caps but I would never buy a stock because it’s small.

We often talk about the stock market as if it’s one entity, but that’s very misleading. The bull market of the late-1990s was heavily skewed to large-cap stocks. Morgan Housel writes, “In 1999, one of the best years for the market ever, more than half of stocks in the S&P 500 declined. Two companies, Microsoft and Cisco, accounted for one-fifth of the index’s return.” People speak of the terrible stock market from 2000 to 2009, but small-cap value stocks didn’t do so poorly, because they had been so badly left behind.

-

Scary Looking Chart

Posted by Eddy Elfenbein on January 27th, 2014 at 3:09 pmThis is hardly sophisticated analysis, but I’m struck by how scary this long-term chart of the Consumer Discretionaries ETF ($XLY) looks. I’ve compared it to the SPY.

The largest holding in the XLY is Amazon which is always dangerous to bet against. But it also has solid Buy List stocks such as Ford ($F) and McDonald’s ($MCD).

-

The Emerging-Markets Meltdown

Posted by Eddy Elfenbein on January 27th, 2014 at 7:55 amI wanted to talk a little about what’s been happening in the market recently. The Dow fell 176 points on Thursday and another 318 points on Friday. The real pain, however, has been in the emerging markets, and especially in their currency and bond divisions.

A lot of folks are blaming the Federal Reserve, and the winding down of QE (more on that in a bit). While our central bank is a convenient villain—and very often, the proper one—in this case, I don’t think they deserve the blame.

Let’s take a step back. When the financial crisis hit, the Fed and other central banks lowered interest rates to the floor. Econ 101: Money goes to where it’s treated best, so people started investing heavily in emerging markets where the yields (and risks) were higher. Investors particularly liked the so-called BRICs (Brazil, Russia, India and China). I’d throw South Africa into the mix as well.

The problem is that a lot of the emerging economies have some serious structural problems. The inflow of cash bought them time, but they haven’t done much to change their ways. Now that the Fed is talking about winding down its extraordinary measure, investors realize that near-0% interest won’t last much longer. Naturally, that will dry up the capital flow to the emerging markets. This problem is compounded by the fact that the governments in the emerging markets loaded up on dollar-dominated U.S. Treasury debt. As a perverse result, they’re doubly sensitive to moves in U.S. interest rates.

People knew this day would eventually come; they just didn’t know when. “When” is apparently now. The governments in the emerging markets are somewhat like a person who builds a balsa-wood house in a tornado zone. When the house goes to smash, they blame the poor foresight on the builder’s part, not the tornado.

The situation in Argentina is especially screwed up—although when I use the phrase “screwed up” in conjunction with our friends on the Rio Plata, it’s like saying there’s “trouble” in the Middle East. The president of Argentina didn’t make any public appearances for six weeks. Can you imagine if President Obama had done the same?

President Kirchner promised not to devalue the currency, but reality intervened. Of course this was after the government spent a pile of cash trying to defend the indefensible peso. In the last three years, Argentina’s currency reserves have been cut in half. No one really knows what the inflation rate or dollar-peso exchange rate truly is.

There are a lot of people in Argentina, in and out of government, whose job it is to see how well the economy is doing. They track all sorts of complicated econ data, but I have a simple rule I use: How loudly are the politicians yapping about the Falklands? If they’re loud, you can be sure that means the economy is a wreck.

I don’t want to pick on Argentina. Turkey is in bad shape as well. Brazil doesn’t look so hot, either. The one saving grace for a lot of EMs was their monster customer in China. But when we got sluggish economic reports from China, that really spooked EM investors. And oh yeah, there also appears to be a revolution going on in Ukraine. That, too, affects things.

It’s gotten so desperate that even the poor battered yen has done well. I’ll give you another easy rule: If your country exports a lot of commodities (especially to China), then your currency probably got whacked. Places like Turkey, Argentina and Venezuela are running very low on their forex reserves. Broadly speaking, I think currency devaluations can be the best of several bad options, but they don’t work all by themselves. You need reform, too, and that can be politically unpopular.

Quick tangent: One stock that I like to follow is Ingredion (INGR). They make high-fructose corn syrup. A lot of their operations are in Argentina, and last year, INGR cut its full-year forecast due to the government’s policies. The shares got hit hard on Thursday and Friday. By most superficial measures, the stock is cheap, but I’m not going near it. There are just too many unknowns.

Several years ago, Bill Gross of PIMCO made a daring investment when he loaded up on Brazilian bonds. That was a shrewd move, and it turned out to be a big winner. So it was a bit jarring when Gross recently said that Brazil is no longer attractive.

I don’t know where all these recent EM developments are headed, but we’re going to soon find out who’s been responsible and who hasn’t. Mexico, for example, will probably pull through just fine. Poland as well. But I’m not so sure about others. Until then, we can expect a little more volatility in our markets and a lot more in the emerging markets.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His