-

Morning News: January 27, 2014

Posted by Eddy Elfenbein on January 27th, 2014 at 5:54 amGerman Business Confidence Rises as Growth Pickup Seen

Euro Jobless Record Not Whole Story as Italians Give Up

Record Japan Trade Deficit Highlights Cheap Yen Woes

Yen and Swiss Franc in Vogue on Emerging Market Stress

India Lifts Ban on Airbus A380s, Foreign Carriers Interested

Justice Department Inquiry Takes Aim at Banks’ Business With Payday Lenders

Apple Manufacturing Partner Looks to Build Factory in the US

Liberty Global Increases Buyback Program by $1 Billion

LG Electronics’s Mobile Unit Suffers Hit

AT&T Gives Up Right to Offer to Buy Vodafone Within 6 Months

Google to Buy Artificial Intelligence Company DeepMind

Chipotle Blurs Lines With a Satirical Series About Industrial Farming

Tata Motors Chief Karl Slym Dies

Epicurean Dealmaker: Mirror, Mirror, on the Wall… and Mirror, Mirror Redux

Jeff Miller: Weighing the Week Ahead: What Is The Market Message?

Be sure to follow me on Twitter.

-

S&P 500 Falls 2.09%

Posted by Eddy Elfenbein on January 24th, 2014 at 5:49 pmToday was the worst day for the stock market is more than four months. The S&P 500 dropped 2.09% to 1,790.29. We lost two important marks — 16,000 on the Dow and 1,800 on the S&P. The S&P 500 closed below its 50-day moving average for the first time since October 9. The index is 5.2% above its 200-DMA, which we haven’t closed below in 14 months.

Nineteen of our 20 Buy List stocks closed down today. Microsoft ($MSFT), thanks to the good earnings report, was our only winner.

The big loser was Moog ($MOG-A) which lost 8.85% after their earnings report. Despite that big loss, our Buy List held up reasonably well compared with the rest of the market. For the day, we lost 2.20% which was 0.11% worse than the S&P 500. Moog, by itself, made up 0.45% of today’s loss.

For the quarter, Moog made 88 cents per share which was one penny below expectations. Their outlook, however, was rather weak:

Moog also warned that its profits for the entire fiscal year would fall about 10 percent short of what both the company and analysts were forecasting. Moog now said it expects its profits to rise to $169 million, or $3.65 per share. That’s less than the $3.95 to $4.10 per share that the company forecast last fall and below the $4.06 per share that analysts were forecasting, but still an improvement from the $3.50 it earned last year.

Moog said it now plans to spend an additional 15 cents per share on research and development expenses for its aircraft business, while its business system conversion also is forecast to cost about 10 cents per share more than expected. The company also trimmed its sales forecast for the year by nearly 2 percent, or $45 million, to $2.63 billion from the previous prediction of $2.67 billion. That’s still up from $2.61 billion last year. The expectation of lower sales growth led to a reduction of about 10 cents per share in the company’s earnings forecast.

-

Beating Lowered Expectations

Posted by Eddy Elfenbein on January 24th, 2014 at 1:49 pmIn today’s newsletter, I wrote:

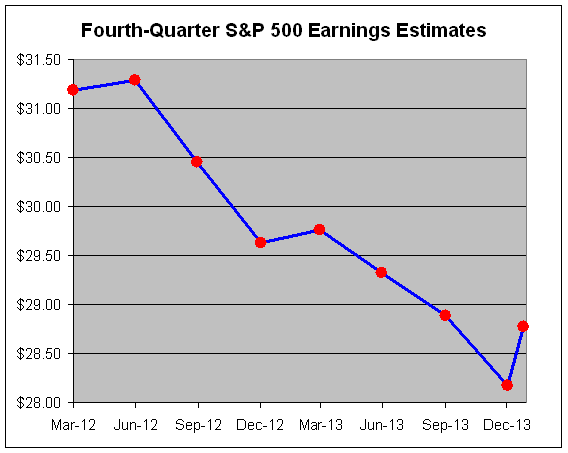

We’re still fairly early in the Q4 earnings season. Some 109 of the 500 stocks in the S&P 500 have reported so far. Of those, 74% have beaten their earnings estimates, while 67% have beaten their sales estimates. Unfortunately, those numbers sound better than they are when we consider that going into earnings, many companies had rolled back expectations. Essentially, they lowered the bar to the ground and now expect applause from investors for stepping over it. Well, that hasn’t been happening.

Now I have a graph to back up that point. This is the estimate over time of earnings for Q4 2013 (courtesy of S&P).

So yes, we’re beating expectations.

-

The S&P 500 Breaks Its 50-DMA

Posted by Eddy Elfenbein on January 24th, 2014 at 10:52 amFor the first time in three months, the S&P 500 has dropped below its 50-day moving average.

-

CWS Market Review – January 24, 2014

Posted by Eddy Elfenbein on January 24th, 2014 at 9:21 am“Successful investing is anticipating the anticipations of others.” – JM Keynes

The stock market has been getting bumped around lately, and it hasn’t had much direction at all. Since December 23rd, the S&P 500 has closed every day but one between 1,826 and 1,849. That’s a fairly narrow range, although we are starting to see some behind-the-scenes rotations. For example, healthcare stocks are outperforming as consumer discretionary issues are lagging. The bond market has quietly improved, and the 10-year yield just hit a six-week low.

Of course, the major focus this week has been earnings, earnings and more earnings. The theme so far is that not even good earnings are enough. Investors want to see big earnings beats plus higher guidance. If you don’t have both, you’re in trouble.

We’re still fairly early in the Q4 earnings season. Some 109 of the 500 stocks in the S&P 500 have reported so far. Of those, 74% have beaten their earnings estimates, while 67% have beaten their sales estimates. Unfortunately, those numbers sound better than they are when we consider that going into earnings, many companies had rolled back expectations. Essentially, they lowered the bar to the ground and now expect applause from investors for stepping over it. Well, that hasn’t been happening.

Fortunately, our Buy List stocks have reported very good earnings results so far. Again, it’s early, but all six stocks have beaten expectations. A few beat them by a lot. However, the stocks haven’t been richly rewarded by the market. It’s not just our stocks; no one’s getting any earnings love, and this really shows the market’s ornery temperament.

Make no mistake: I still like the environment for stocks, but we have to come to terms with the reality that the market’s easy gains have already been made. This year won’t be as easy and stress-free as last year was. We’ll still see gains, but we need to be patient and have some humility.

In this week’s CWS Market Review, I’ll run through our Buy List earnings reports. We had especially strong results from CA Technologies and Microsoft. The report from IBM, however, was rather weak, though I wasn’t expecting much.

Later on, I’ll highlight our earnings reports for the coming week. Also, our friends at the Federal Reserve meet on Tuesday and Wednesday. It will be Mr. Bernanke’s swan song, and I expect to see another taper announcement. But first, let’s look at why everyone hates IBM (but me).

IBM Beats Earnings but Falls

On Tuesday, International Business Machines ($IBM) reported Q4 earnings of $6.13 per share. That was 14 cents more than Wall Street’s consensus. That’s the good news. The bad news is that much of that earnings beat was driven by cost-cutting. IBM’s top line numbers were pretty weak. Quarterly revenues fell 5.5% to $27.7 billion. That was $600 million below forecast, and it was the seventh-straight quarter of falling sales.

We know that much of the tech world is shifting to cloud-based networks, but Big Blue isn’t exactly sitting still. The company is aggressively moving toward cloud services, and they’re ditching their lower-margin businesses. They just sold their server business to Lenovo for $2.3 billion. The company also realizes the situation it’s in; the entire senior team has foregone bonuses. On the positive end, I was impressed to hear IBM say that it sees earnings for 2014 of at least $18 per share. They also reiterated their earnings target of $20 per share for 2015.

Simply put, IBM isn’t popular on Wall Street at the moment. The stock got clipped by more than 3% on Wednesday, the day after the earnings report came out. I’m not saying that IBM doesn’t face a difficult environment. It does. Its systems and tech revenue fell 26% last quarter. But IBM has transformed itself many times in its history. Remember that their cloud revenue rose by 69% in Q4 to $4.4 billion.

I think IBM is in a position similar to where Microsoft was one year ago. Bears have been having a field day beating them up, but the stock is cheap now. It’s going for about 10 times earnings, which is far less than the rest of the market. My take: IBM will require some patience, but it’s a solid stock. I rate IBM a buy up to $195 per share.

CA Technologies Is a Buy up to $36 per Share

Also on Tuesday, CA Technologies ($CA) reported earnings of 84 cents per share, which easily beat Wall Street’s forecast of 71 cents per share. Last week, I said the Street’s consensus was “a wee bit too low.” Shows you what I know! Interestingly, this was the third time in the last four quarters that CA has beaten earnings by 13 cents per share.

CA also guided Wall Street higher for the rest of the year. The December quarter is the third quarter of its fiscal year. So for 2014, CA now sees earnings ranging between $3.05 and $3.12 per share, compared with Wall Street’s estimate of $3.02 per share. The company also sees full-year revenues ranging between $4.52 and $4.57 billion, versus the consensus of $4.50 billion. This is what we like to see: beat and raise.

CEO Mike Gregoire said, “Based on our results so far this year, we expect our fiscal year 2015 revenue growth rate and non-GAAP operating margin to be similar to fiscal year 2014.” That sounds good to me. So what did the market do with this good news? On Wednesday, shares of CA rallied by…four cents! Then on Thursday, they dropped by 65 cents. No, it doesn’t make any sense, but you can never argue with traders. Instead, we look at the facts. Going by Thursday’s closing price, CA’s dividend yields 3%. This week, I’m raising our Buy Below on CA to $36 per share. This is one of the good ones.

Both Stryker and eBay Beat by a Penny per Share

On Wednesday, both Stryker and eBay reported earnings that beat expectations by one penny per share. Let’s break down the results.

For Q4, Stryker ($SYK) earned $1.23 per share, compared with Wall Street’s consensus of $1.22 per share. Honestly, I wasn’t too concerned with Stryker’s earnings report. They usually come very close to expectations. But I wanted to hear what the orthopedic outfit had to say about 2014.

For this year, Stryker said they see organic revenue growth of 4.5% to 6%, and earnings ranging between $4.75 and $4.90 per share. That’s a very good number, and it’s well above where the Street was at $4.63 per share. For all of 2013, Stryker earned $4.23 per share.

So with all this good news, what did the stock do on Thursday? It dropped 1%. I don’t get this one either. Stryker remains an excellent buy. I’m raising our Buy Below on Stryker to $81 per share.

eBay ($EBAY), one of our new stocks this year, turned out to be the most newsworthy company this week. For Q4, the online-auction house reported earnings of 81 cents per share, one penny more than consensus. The company also authorized another $5 billion for its share-buyback program.

But the big news came when multi-gazillionaire Carl Ichan said that he wanted to see eBay spin off its PayPal business. Icahn said that he’s going to nominate two of his people for the eBay board. Spinning off PayPal isn’t a new idea, but this is the first time someone so prominent has endorsed it. The board doesn’t like the idea, and they told Icahn so. But the market seems favorable for a spin off. On Wednesday afternoon, shares of eBay were trading up 8% in the after-hours market. On Thursday, however, eBay rallied for a 1% gain.

Frankly, I doubt we’ll see a PayPal spin-off. It’s too integrated into eBay’s business. But I like seeing Carl Icahn advocate on behalf of shareholders. He didn’t get to where he is by being a shrinking violet. eBay had a solid quarter, and it continues to be a very good buy up to $58 per share.

A Tough Quarter at McDonald’s, but Give Them Time

On Thursday morning, McDonald’s ($MCD) reported Q4 earnings of $1.40 per share. That made the company our third earnings report in a row that beat estimates by one penny per share. Sales at the hamburger giant rose by 2% to $7.09 billion. But the details were pretty ugly. Comparable-store sales dropped by 0.1%, and in the U.S., comparable-store sales fell by 1.4%. Ouch.

McDonald’s faces a number of challenges. The new CEO, Donald Thompson, hasn’t been as effective as I would have hoped. They’ve played around with the menu, but nothing has really taken off. The menu has probably grown too complicated and could use some paring down.

The situation at McDonald’s is somewhat similar to that at IBM. The current environment is rough, but the stock is going for a good value. Ultimately, I think the problems are very fixable, but it will take a little time and effort. McDonald’s made about the same profit as one year ago, but thanks to share buybacks, there are fewer shares outstanding, so EPS rose by two cents. The dividend currently yields us 3.4%, which is a nice buffer for us. MCD is a buy up to $102 per share.

Impressive Earnings Beat from Microsoft

After the bell on Thursday, Microsoft ($MSFT) had a very strong earnings report. It turns out that Xbox had a great holiday season. The software giant had a net income of $6.56 billion, or 78 cents per share. That was a full dime more than Wall Street’s forecast. At the top line, revenue rose 14% to $24.52 billion. The Street had been expecting sales of $23.68 billion. The best news is that Surface revenue more than doubled to $893 million.

While Xbox continues to be a great profit center for Microsoft, the Surface is still small potatoes. One big piece of missing news is that Microsoft still hasn’t yet announced who its next CEO will be. Ballmer is out soon. If you recall, there was some speculation that Ford’s Alan Mulally would jump ship and take over at Microsoft. Fortunately, that won’t happen.

Microsoft jumped up more than 3% in Thursday’s after-hours market, but we’ll have to see how it trades from here. Microsoft was a great buy for us last year when it was under $27 per share. MSFT isn’t a screaming buy like it was a few months ago, but it’s still a good value. We also had a very nice dividend increase recently. Microsoft is a good buy up to $40 per share.

Upcoming Buy List Earnings

Still more earnings come in next week. Ford is due to report on Tuesday, January 28. Qualcomm follows on Wednesday, January 29, and CR Bard on Thursday, January 30. These dates may change, so please check our website for the latest. Also, Moog ($MOG-A) is due to report later today.

I’m most looking forward to Ford’s ($F) earnings report. The automaker recently threw a damper on expectations for 2014. The short version of the story is that North America is doing well, but Europe is not. Ford has made it clear they’re playing the long game, so we probably won’t see a turnaround in Europe until 2015 or 2016. Wall Street currently expects Q4 earnings of 29 cents per share, which is down two cents from a year ago. That would be disappointing, but Ford is clearly moving in the right direction. The 25% dividend boost was a great vote of confidence.

Qualcomm ($QCOM), another new stock on our Buy List, will be an interesting earnings report to see. The last report was a dud, and the stock’s subdued performance last year led me to add it to this year’s Buy List. The sentiment is beginning to shift here. If Qualcomm beats and offers impressive guidance, the shares could break out.

Three months ago, CR Bard ($BCR) told us to expect Q4 earnings to range between $1.34 and $1.39 per share. That would put full-year 2013 earnings between $5.70 and $5.75 per share. They should hit that range without much difficulty. Bard is a buy up to $142 per share.

That’s all for now. Next week will be the final trading week for January. The Federal Reserve meets on Tuesday and Wednesday. This will be Ben Bernanke’s final meeting as Fed chair. I expect to see another round of tapering. We have a few more Buy List earnings reports coming our way. On Thursday, we’ll also get our first look at Q4 GDP. The last three GDP reports have all seen increased growth rates, meaning economic acceleration. Let’s see if that continues. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: January 24, 2014

Posted by Eddy Elfenbein on January 24th, 2014 at 7:13 amEM Currency Rout As Risk Appetite Wanes

ECB Says to Cease 3-Month Dollar Operations as of April 2014

Japan Government Forecasts Show Abe Missing Budget-Balance Promise

Sochi’s Hotel Scarcity Deters U.S. Fans Considering Late Trips

Billionaire Braves Bloated Self-Importance for Davos Chat

Microsoft Posts Record Sales as Ballmer Prepares to Exit

Icahn Says He Is Prepared for eBay Proxy Fight

Samsung Electronics Pledges Higher Dividend After Record Payout

VW Labor Rep Blasts Car Maker’s U.S. Strategy

Can Jamie Dimon’s Pay Spark Political Populism?

Senator Is Lobbying for Inquiry on Herbalife

Key Witness Says Cohen of SAC Was F.B.I. Target

Credit Writedowns: Argentina – From Bad to Worse

Jeff Carter: Does the Economy Need Risk?

Be sure to follow me on Twitter.

-

25 Years of Stocks Vs. Bonds

Posted by Eddy Elfenbein on January 23rd, 2014 at 3:45 pmWhen we ask the question, “Are stocks cheap?,” we have to consider the important qualifier: compared with what?

Understand that every asset is in competition with every other asset for investors’ money. It’s like one giant cage match of relative value. There’s no absolute standard of value for any asset class at any time. The question is always, “Compared with what?”

This is why the stock and bond markets have such a problematic relationship. Frenemies, if you will. Every so often I like to look at how the stock market is doing — not in terms of dollars, but in terms of the bond market.

Below is a chart of the total return of the Wilshire 5000 (including dividends) divided by an index of AAA bonds.

Over the long haul, I would expect stocks to out-perform bonds, but not by much. The chart above shows that it’s a very rocky and highly volatile relationship.

Stocks have done well recently, but that’s making up a lot of lost ground. over the last 15 years, stocks have done just about as well as bonds have.

I wouldn’t make any predictions off this chart, but I would draw your attention to an interesting aspect. Notice how the blue line climbs steadily but falls very quickly. Yes, the bond market doesn’t like being ignored.

-

McDonald’s Earns $1.40 Per Share

Posted by Eddy Elfenbein on January 23rd, 2014 at 11:30 amYesterday, eBay and Stryker beat by one penny per share. Today, it’s McDonald’s ($MCD) turn.

McDonald’s reported fourth-quarter sales growth that missed estimates, even though earnings per share beat forecasts by a penny a share.

The fast food giant said it earned $1.40 billion, or $1.40 a share, as sales climbed 2% to $7.09 billion. Global comparable-store sales dropped 0.1%, adjusting for the opening of new stores and closing of others.

U.S. comparable-store sales dropped 1.4%. The company said the average customer spent more, but there were fewer of them.

The profit was virtually unchanged from late 2012, though earnings per share rose two cents as the company’s share count decreased due to stock buybacks. Analysts had expected profit of $1.39 a share.

McDonald’s shares were up 0.5% to $95.35 in morning trading.

“As we begin 2014, global comparable sales for the month of January are expected to be relatively flat,” McDonalds CEO Don Thompson said. “While near-term challenges remain, we are intent on strengthening our brand to further differentiate McDonald’s and become an even bigger part of our customers’ lives.”

-

Morning News: January 23, 2014

Posted by Eddy Elfenbein on January 23rd, 2014 at 4:56 amDavos Bankers Struggle to Convince Elite That Markets Are Safer

China Stocks Fall With Yuan After Surprise Manufacturing Decline

Spain Says Jobless Rate Tops 26% at End of 2013

In Twitter Onslaught, Carl Icahn Nags Apple to Spend More Money

EBay Says Icahn Proposes PayPal Spinoff After Taking Stake

IBM’s Earnings Blues Are a Big Opportunity

Lenovo to Buy IBM Low-End Server Business for $2.3 Billion

Toyota Beats GM, VW in 2013 as 3% Growth Planned in 2014

LG Display Q4 Operating Profit More Than Halves, Beats Analyst Estimates

Why Advanced Micro Devices, Inc. Shares Plummeted

Netflix Soars on Possible Price Shift as Outlook Tops Estimates

Target Hack A Tipping Point In Moving Away From Magnetic Stripes

Coach Sales in North America Plummet as Market Share Erodes

Jeff Miller: Ignore the Fed Factoid

Joshua Brown: Active is the New Passive

Be sure to follow me on Twitter.

-

Good Earnings for Stryker and eBay

Posted by Eddy Elfenbein on January 22nd, 2014 at 4:53 pmAfter the closing bell, we got two more Buy List earnings reports.

Stryker ($SYK) beat by one penny per share.

U.S. orthopedic implant maker Stryker Corp on Wednesday said quarterly net profit rose 43 percent, driven by increased sales in its reconstructive and neurotechnology divisions as well as lower taxes.

The company reported fourth-quarter net earnings of $386 million, or $1.01 per share, compared with $270 million, or 71 cents a share a year earlier. Net sales for the quarter rose 5.6 percent to $2.47 billion.

Excluding items such as product recall and acquisition charges, Stryker earned $1.23 per share. Wall Street analysts, on average, expected $1.22 per share, according to Thomson Reuters I/B/E/S.

Stryker said its effective tax rate in the latest quarter was 10.3 percent, compared with 24.6 percent in fourth quarter 2012.

For full-year 2014, the company projected organic sales growth of between 4.5 percent and 6 percent.

For all of 2013, Stryker earned $4.23 per share. The company sees earnings between $4.75 to $4.90 per share for 2014. Wall Street had been expecting $4.63 per share.

ebay ($EBAY) also beat by one penny per share and it drew some interesting comments from Carl Icahn.

EBay Inc. on Wednesday reported a fourth-quarter profit of $850 million, or 65 cents a share, on revenue of $4.5 billion, compared with earnings of $751 million, or 57 cents a share, on $3.99 billion in sales in the year-ago period.

Excluding one-time items, eBay would have earned 81 cents a share. Analysts surveyed by FactSet had forecast eBay to earn 80 cents a share on $4.55 billion in sales.

Additionally, eBay said it authorized an additional $5 billion stock repurchase program.

EBay also said that it received a proposal from activist investor Carl Icahn seeking to spin off PayPal as a separate company, and that Icahn is nominating two of his employees for positions on eBay’s board of directors. EBay shares rose 8% in after-hours trading following the slate of announcements.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His